South Africa - Personal

South Africa - Personal

In last quarter’s commentary we wrote, ‘2019 was a year to make money’. However, we also cautioned that, ‘after a sustained period of strong equity returns, declining interest rates, reduced tax rates, expanding profit margins, and rising valuation multiples, investors should recalibrate return expectations lower. The conditions in place today are quite different to those in place a decade ago. We have no insight into short-term market moves but feel that absolute returns could very well be lower over the next 10 years compared to the last 10.’

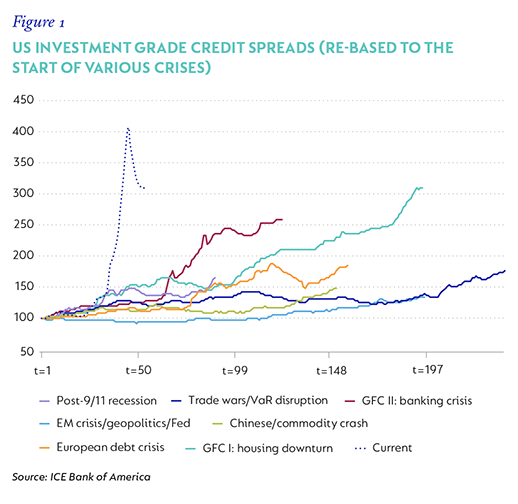

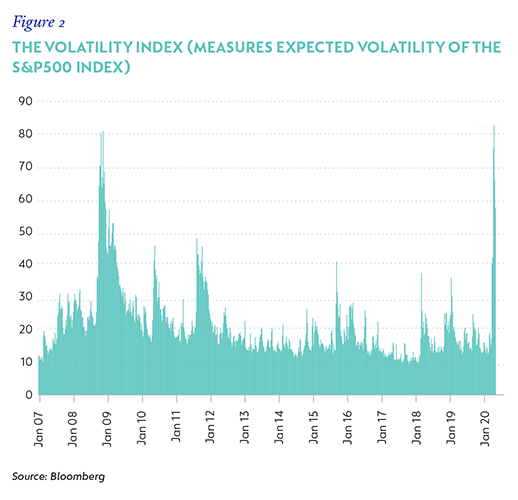

Well, we didn’t have to wait long. Risk assets plunged over the quarter as the economic consequences of the Covid-19 pandemic started to become apparent (for a full discussion, please see Coronation’s commentary on page XX). Economic activity in many countries and sectors around the world has come to a halt. This unprecedented ‘full stop’ caused stress and market dislocations across the spectrum. Volatility was back with a vengeance, and, in both credit and equity markets, indicators spiked to levels above those seen in the Global Financial Crisis (refer to figures 1 and 2).

With this as a backdrop, Global Equity Select declined -22.6% in US dollars for the quarter, slightly behind the benchmark’s -21.4%. Given the weak rand, this translated into a rand decline of -1.9% for the Global Equity Select Feeder Fund. Quarterly returns will inevitably be noisy, but we were cognisant of the high relative base of performance coming into the year following a strong 2019, which delivered 11% outperformance, and are reasonably satisfied to have at least protected these relative gains.

Global Managed declined -16.4% for the quarter compared to -13.3% for the benchmark, while the Global Managed Feeder Fund returned 6.5% in rand. The fund’s equity holdings were marginally behind the benchmark over the quarter. Global Capital Plus declined -9.7% for the quarter compared to 0.8% for the benchmark, while the Global Capital Plus Feeder Fund returned 14.8% in rands. This fund’s equity portfolio was appropriately sized, selected and hedged. The negative contribution from equities was just over 5%. The stocks themselves performed in line with the overall market, and index-level hedges reduced losses by a quarter.

The underperformance in both funds was primarily due to the non-equity securities in their portfolios. The lack of developed market government bond exposure was the primary culprit, as we have chosen instead to take some credit risk which sold off as credit spreads increased. Importantly, these are mark-to-market losses, not permanent impairments, as we either still hold those securities or have rotated into issues with a more favourable risk-reward profile.

While the quarterly declines are disappointing, it follows on a strong 2019, with alpha of 5% and 10% for Global Managed and Global Capital Plus, respectively. Although we are never satisfied with underperformance, we are excited by a much-improved opportunity set, which is most important for potential future returns.

Following such a dramatic quarter, it is also worth reflecting on some of the additional aims for managing Global Capital Plus and Global Managed as outlined in last quarter’s commentary. In particular the third point:

‘Do not expose the funds to excessive risk, even if such exposures represent large asset classes which, in a normal environment, would be well-suited to their strategies (such as developed market government bonds today).’

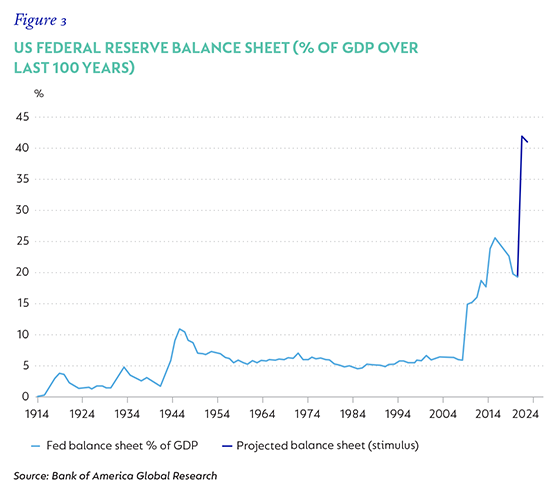

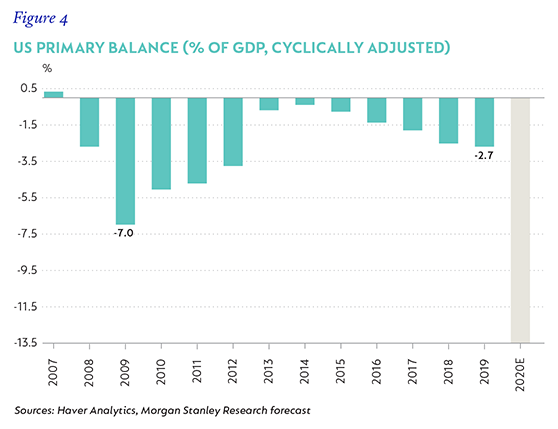

The fiscal and monetary response to the Covid-19 pandemic is unprecedented. Aggressive monetary measures are pumping vast amounts of liquidity into the system causing central bank balance sheets to surge, while fiscal deficits are also set to explode once economic support is factored into government finances.

Data for the US is shown in figures 3 and 4, but it is mirrored (to varying degrees) in Europe, Japan, China and the UK.

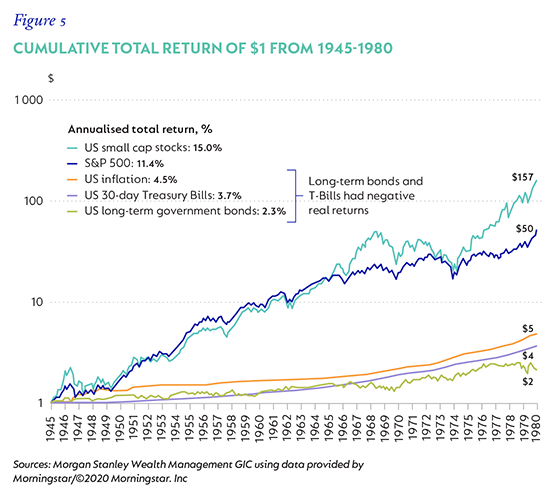

Notwithstanding the current recessionary conditions, which Morgan Stanley believes could be the fastest and steepest recession in history, resulting in spare capacity and economic slack, the world will eventually get back to work. From this low base of activity, pent-up demand (combined with huge stimulus) could be highly inflationary. In this scenario, the US experience after World War 2 is instructive and highlights the material underperformance, and declining purchasing power, of cash and government bonds (see Figure 5). This is in stark contrast to the last few decades during which bonds have been the ultimate low volatility, low risk, uncorrelated, and real return-generating asset:

- Since 1990 (30 years), the global bond index returned 5.7% p.a., less than 1% behind global equities, with a fraction of the volatility and drawdown risk.

- Since 2000 (20 years), the global bond index has beaten equities by c.0.5% p.a.

As bonds approach the zero bound, the asymmetry of returns skews increasingly one way. Yields cannot be forever compressed, so the upside potential is limited (bond prices go up when yields go down). However, poor prospective returns from rates simply staying where they are, negative real returns from monetary debasement and negative absolute returns from a rise in interest rates are all possibilities.

While the inflationary scenario outlined above is only one potential outcome, it does inform our positioning and we continue to hold no developed market government bonds in Global Managed and Global Capital Plus. In turn, we have built positions in assets that should perform well in an inflationary environment. Aside from the allocation to risk assets (equity, property and infrastructure), which comprised 64% in the case of Global Managed and 37% in the case of Global Capital Plus at quarter-end, we also have 10% to 11% of the funds’ portfolios in gold and inflation-protected securities.

KEY PORTFOLIO ACTIONS

- Active management of equity exposure

Walking through the changes in a volatile quarter such as this will help to illustrate the process. Global Managed started the quarter with 60% effective exposure to equities. On 27 February, with markets not far off their highs (the MSCI All Country World Index was 522), exposure troughed below 55%, as we grew concerned about the potential fall-out from the virus amidst fairly widespread complacency in the market. Equity exposure peaked at 64% on 25 March (index level 428, c. 20% lower). Global Capital Plus started the quarter with 30% effective exposure to equities. On 27 February, exposure troughed at 25% and peaked at 32.7% on 31 March (index level 442, c. 15% lower). Considering the decline in the markets and the increase in exposure, one can see the funds were meaningful net buyers into the decline. While we will never time these actions perfectly, with a disciplined, rational process and a valuation philosophy that is rooted in the long term, we aim to have lower equity exposure when risks and valuations are high, and higher exposure when prospective returns are higher. Simple, but not easy. - Changes in equity holdings

Most of our large holdings going into the quarter were well positioned for the coming economic stress. In the top 10, Chinese internet businesses Tencent (via Naspers) and Alibaba are arguably net beneficiaries, being leaders in gaming and ecommerce. Charter Communications, a broadband provider in the US, is seeing much higher demand for their essential internet service, although the business is not immune, and cord-cutting will accelerate and subscriber growth will slow as the unemployment wave hits. Tobacco businesses Philip Morris and British American Tobacco have seen stable demand. Airbus is an obvious exception. With entire countries in lockdown and many airlines around the world facing bankruptcy, orders of new aeroplanes are being delayed and cancelled. The stock ended down more than 50%. Airbus has a net cash balance sheet, which should see it through this crisis. Deliveries will be cut substantially over the next couple of years, but, looking through this extended period of disruption, our estimate of normalised earnings power justifies a significantly higher share price.

The funds took advantage of a few anomalies – good businesses that initially sold off in line with the market, but whose prospects had only changed marginally. Unilever is a case in point. The stock traded close to 14 times earnings, and with a dividend yield of nearly 4.5% at the lows, which we thought provided good value – in particular when the potential range of outcomes for the average business had widened so considerably. We also re-entered Diageo and bought stocks such as Intercontinental Exchange and Thermo Fisher.

Earlier in the quarter we exited or reduced holdings that had performed strongly and approached our estimates of fair value. Adidas, Blackstone and Apollo were all sold. - Other changes

Within credit, the most meaningful portfolio actions centred on investment-grade credits to take advantage of dislocated credit spreads (as shown in Figure 1). While these actions don’t dramatically change the return profile of the portfolio, they help at the margin. Examples of near-dated issues that were purchased include:

- Berkshire Hathaway (AA-rated) August 2021s were bought at a credit spread of 250 basis points (bps) over Treasuries.

- GlaxoSmithKline (A-rated) May 2022s were bought at a credit spread of 290bps.

OUTLOOK

Markets could very well remain volatile as the nature of the pandemic evolves and progresses. As a team, we are focused (as always) on researching individual businesses, assessing their long-term earnings power, understanding the potential impact this black swan event may have on the investment case, managing risk and adjusting the portfolio accordingly. While the backdrop has changed dramatically, our process hasn’t.

Thank you for your continued support and interest in the funds.

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter