Quarterly Publication - April 2017

MTN - April 2017

“He who is not courageous enough to take risks will accomplish nothing in life.” Muhammad Ali

MTN came out of 2016 battered and bruised. The $5.2 billion fine on its Nigerian operations over unregistered SIM cards dealt a massive blow to its image as an African champion in mobile telephony. However, Nigeria was not MTN’s only hot spot last year. Many of its other operations also battled weakening economies and governments that were keen to bolster fiscal revenues by targeting cash-rich corporate entities. In addition to increasing regulatory demands for customer SIM card registration, MTN found itself subject to additional taxes and obligations in some markets to localise ownership of its subsidiaries. Internally, the company was attempting to stabilise its senior management team and to catch up on data network investment in key markets. Difficulties around the fine were compounded by constraints on extracting cash out of Nigeria, and there were concerns about the sustainability of the company’s dividend payment.

Recently released annual results for the year ended December 2016 saw continued pressure on MTN’s earnings, reflecting the tough environment and internal turmoil at the company. It did, however, manage to keep to its commitment to pay out a R7 dividend for the full year, and has committed to keep this flat for the 2017 financial year. With the fine settlement behind it and the rebasing of earnings, MTN now faces a critical turning point to prove whether it can capitalise on the still latent growth opportunity in its operations. It is certainly well equipped to do so. It commands strong, leading positions in most of its regions. It can also use tough times to entrench its moat by investing in infrastructure, while its competitors struggle with financing. With proper management execution, we think the next leg of growth for MTN will be delivered over the coming few years.

Historic growth witnessed in MTN’s early years was driven by entering virgin markets and building scale and coverage quickly. MTN enjoyed first-mover advantage, which resulted in it easily obtaining a large customer base that previously had very little access to communication. Once the business had built scale, however, it struggled with transitioning from an entrepreneurial operation to a professional organisation. Management’s focus on cost efficiencies and cash generation came at the expense of network investment in data capacity and providing customers with high-quality service. As a result, the company allowed competitors to take valuable market share.

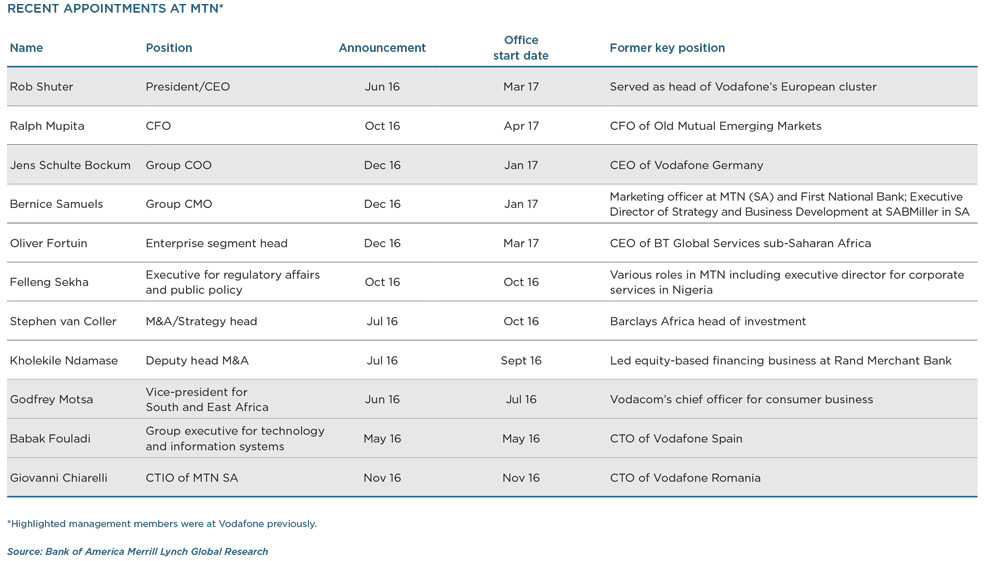

The Nigerian fine was a significant shock. While it was a major negative event, we think it forced the board into taking fundamental strategic steps to address complacency. The introduction of a new, experienced senior management team will enhance the ability of the company to deliver on its growth potential. These new appointments bring fresh energy to the company. They are also capable of addressing the underlying issues on a clean-slate basis, without any ties to legacy thinking.

Future growth in MTN will come from three areas:

- managing the existing base business better;

- accelerating the growth of new adjacent revenue streams; and

- good capital allocation.

While MTN has built a big business, it has not made the most of leveraging its scale. It has done some work to improve purchasing power in network equipment and handsets, but it has not been able to put in place a central steering function that is able to give coordinated direction to each of the operational companies. The new management team will implement this central model, which will enable regions to drive market strategies quickly and intelligently. Management is also focused on the very basics of network deployment, and is looking to improve network availability by using spectrum more efficiently and increasing 4G tower rollout (which will improve data capacity). These actions were first implemented in South Africa and Nigeria, and will be implemented in other operations during 2017. Network improvements will be coupled with the standardisation of business metrics and the upgrading of IT systems, which will allow for greater customer and business analytics. Combined, the increased quality of service and enhanced management information should enable MTN to grow market share and accelerate data revenue growth.

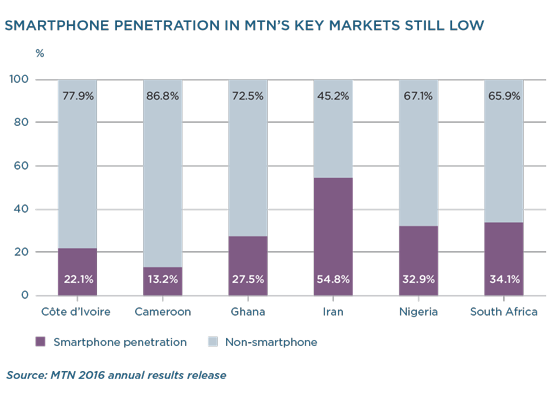

While business basics are being addressed, there is also a clear opportunity to grow revenue streams that are complementary to basic voice and data services. Smartphone penetration in MTN’s main markets is set to increase as handsets become more affordable. Customers are also using these handsets to perform more transactions and consume more content. MTN has already rolled out some of these services (music, gaming and mobile money) and they are growing strongly, with reported revenue growth of 44% (off a low base) in 2016.

This is not uncharted territory. Safaricom in Kenya is a good example of how a mobile telephony business can successfully leverage its scale to grow into a new category. M-Pesa (Safaricom’s mobile money product) has 16.6 million active subscribers, and mobile money now contributes 22% of Safaricom’s total revenues. MTN has 20 million mobile money subscribers, concentrated mostly in Ghana and Cameroon. We do not expect MTN to replicate the full success of Safaricom across all of its operations, but there is potential to grab more of the financial services income stream in Africa. This will come via the rollout of mobile money products into more countries (mobile money is only in five of MTN’s operating countries at the moment) and the launch of new financial products (such as remittances, microlending and savings products) in addition to basic payments and airtime purchases.

We expect these initiatives to support healthy organic earnings growth over the medium term. In addition, as the company comes out of a heavy capital expenditure cycle, it will convert a high percentage of earnings into cash flows. The business has a good track record of cash conversion – over the past 10 years it has converted about 85% of its earnings into cash. This will be supportive of growth in dividend payments to shareholders. There is also the opportunity to realise further value from the future sale of tower investment assets and digital investments. The current share price attributes little to no value to these investments, and presents another leg of optionality in the investment case.

Some market participants believe MTN is a broken business. We do not think this is the case. The company has weathered a particularly nasty period but has come out of it focused and better equipped to deal with a complex environment. The earnings base is low, and expectations are not high. We acknowledge that there are risks in how this investment case plays out, but feel that these risks are more than adequately discounted in the current share price. Our analysis of past case studies shows that investors tend to underestimate the upside case when new management teams come into undermanaged businesses with good fundamentals. In an uncertain investment environment, we think that MTN presents a powerful combination of attractive fundamentals and self-help initiatives, at an undemanding valuation.

This article is for informational purposes and should not be taken as a recommendation to purchase any individual securities. The companies mentioned herein are currently held in Coronation managed strategies, however, Coronation closely monitors its positions and may make changes to investment strategies at any time. If a company’s underlying fundamentals or valuation measures change, Coronation will re-evaluate its position and may sell part or all of its position. There is no guarantee that, should market conditions repeat, the abovementioned companies will perform in the same way in the future. There is no guarantee that the opinions expressed herein will be valid beyond the date of this presentation. There can be no assurance that a strategy will continue to hold the same position in companies described herein.