Quarterly Publication - October 2017

SA Portfolio Update - October 2017

Our portfolios performed very well over the quarter, supported by healthy returns from most major asset classes.

The JSE had a good quarter, with the FTSE/JSE Capped All Share Index returning +8.4% (9.4% over a rolling 12-month period).

Locally, the headlines continue to be dominated by the political backdrop, which remains volatile. The political and policy uncertainty has wreaked havoc on business and consumer sentiment, with SA business confidence slumping to a 32-year low. This has filtered through to a weak and deteriorating economic growth outlook.

While markets have been remarkably benign, we caution that global risks remain elevated, given the state of political disruption around the world. We remain overweight global equities, and emerging markets in particular, although we have been taking profits into strength.

Equity market returns were driven by a strong performance from the resources sector (+17.8%) and outsized returns from some of the large industrial sector constituents such as Naspers (+15%) and Richemont (+15%), which masked the poor performance of many SA-focused domestic shares. The financial sector lagged the overall market over the quarter.

Against this backdrop, our large holdings in Anglo American (+41%), Exxaro (+35%) and Glencore (+27%) continued to perform strongly and have been the major contributors to our portfolios’ outperformance this quarter. The original investment cases for these specific holdings are playing out. They all remain significant holdings as valuations are still supportive, but we have used share price strength to reduce the respective position sizes.

Our portfolios remain skewed towards stocks with large offshore earnings exposure (Naspers, British American Tobacco, MTN, UK-listed property holdings and Steinhoff). We believe the valuations of these businesses are extremely attractive.

We also continue to maintain reasonable exposure to resources based on our assessment of their long-term value.

We continue to find attractive investment opportunities in defensive, high-quality SA-focused businesses of which the share prices have de-rated significantly. We have bought broadly in names including Spar, Netcare and Curro. These businesses are well managed, cash generative and should be fairly resilient in tough economic conditions.

These purchases were funded predominantly by a reduction in our Naspers holding. This has certainly not been an easy call to make. The Naspers investment case remains compelling; Tencent is a phenomenal business and is at the core of a rapidly growing Chinese internet economy, with numerous opportunities to further monetise its massive user base. As an example, we believe that Tencent’s move into payments and financial services creates a market opportunity several times the size of its current gaming business. Naspers currently trades at an almost 30% discount to its Tencent stake alone – in our view, a complete pricing anomaly.

Furthermore, we have been very encouraged by the steps Naspers management has taken to streamline the rest of the business’s portfolio. Although Naspers remains the largest single position across our equity portfolios, we felt the holding’s absolute size had grown too large for our clean-slate portfolios and had created stock-specific risk for investors in absolute terms.

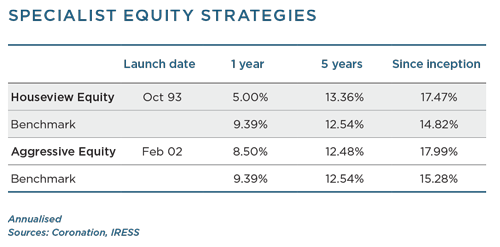

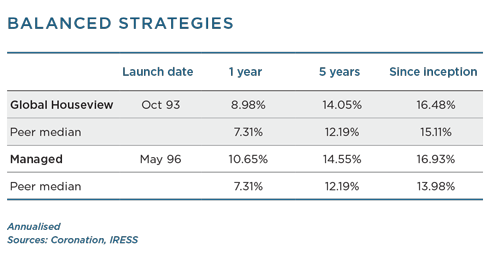

Our balanced strategies, Global Houseview and Managed, continued to deliver outperformance over meaningful periods.

Global equities delivered another strong performance over the quarter, with prospects for synchronised global economic growth more than offsetting a multitude of concerns (which we discuss in other parts of this publication). The MSCI All Country World Index returned 5.2% in US dollars for the quarter (+18.7% over a rolling 12 months), while emerging markets continued their strong rally, returning 8% for the quarter (+22.9% over a rolling 12 months).

Our large weighting in global and, in particular, emerging market equities, significantly added to the portfolios’ performance this quarter, with the Coronation Global Emerging Markets Equity strategy (a top five holding across our global balanced strategies) outperforming the index by 7.5% over the quarter and by 6.5% for the 12-month period.

From an asset allocation point of view, we remain overweight equities in our balanced portfolios. We have used the proceeds from our reduction in global equities (as mentioned earlier) to gradually increase our domestic equity exposure on further weakness in the rand and local equity markets.

We also maintained very low exposure to fixed rate bonds, which had a neutral impact on the portfolios’ return over the quarter. However, our credit portfolio delivered a strong performance over the period. After going through a period of remarkably low appetite for credit locally, we have seen a spike in demand for new credit, which has driven spreads lower.

Our property exposure did not contribute to performance over this period but remains a compelling opportunity. With very attractive distribution yields and potential for significant capital growth in the years ahead, we are very confident that these holdings will be an important part of the future growth of the portfolios. We have continued to add to our exposure to Intu, the UK retail property fund, where we can earn a dividend return in excess of 6%, with potential growth to come from rental growth driven by improved shopping centre performance.

The absolute return portfolios all have dual mandates of beating inflation by a certain target while also protecting capital. In light of the lower return world, we have made slight adjustments to the targets for the various funds, and we have extended the capital protection period from 12 months to 18 months (for more detail, please refer to page 35). While our absolute return strategies have delivered strong positive real returns over all longer-term periods, beating inflation plus the required target over the near term has proved challenging given the tough investment environment where real returns across asset classes have been far lower than the historical trend.

Where it used to be possible to generate reasonable real returns in the interest-bearing portion of a multi-asset class portfolio, it is simply no longer possible. Real returns of only 1% or 2% in cash and bonds have become the norm. Therefore, to meet our inflation targets and preserve capital over shorter time periods, we have reviewed the mandates of our absolute return strategies and will be discussing these amendments with clients directly. We have kept our exposure to risk assets in the respective strategies high as we feel these assets still offer good value. We are concerned that global interest rates will normalise at some point and will place upward pressure on yields in the emerging world too. The bond portion of the portfolios therefore has a very low duration, protecting the fund against capital losses that will be incurred in case interest rates do rise. We are also concerned by the state of government finances and prefer corporate to government bonds.

While the rand proved remarkably resilient for most of the quarter, it weakened materially in September on deteriorating SA sentiment. The rand ended the quarter down 3.6% against the US dollar and almost 7% against the euro. As such, we believe our offshore allocation of close to 25% (where applicable) remains appropriate given the benefits of diversification and the value in the underlying offshore assets. In this uncertain world, our objective remains to build diversified portfolios that can absorb unanticipated shocks. We will remain focused on valuation and will seek to take advantage of attractive opportunities that the market may present, and in so doing generate inflation-beating returns for our investors over the long term.