United States - Institutional

United States - Institutional

Quarterly Publication - July 2016

Mexico - July 2016

Coronation investment team members recently visited Mexico where we gained an on-the-ground view of the country’s prospects and a better understanding of what some of its most dynamic companies are planning. We met one-on-one with a number of key executives and visited operations in the consumer and financial sectors.

In the past, we have been fairly cautious on the Mexican market. Generally, it trades at higher-than-average multiples compared to the rest of the Global Emerging Market (GEM) universe. Also, while its economy is often touted as being close to an inflection point, Mexican growth has been a perennial disappointment. While valuations in Mexico remained stretched (its stock market is currently trading at around 18.4 times one-year forward earnings versus 12 times for the broader GEM universe), we believe that its economic fundamentals as well as various policy initiatives have at last created a more conducive environment for select medium- to long-term investment opportunities. Mexico has either already implemented, or is in the process of implementing, a series of reforms in education, energy, banking and the fiscus – arguably, the most ambitious policy reform programme in our GEM universe.

Still, we have found a clear disconnect between the respective outlooks of policymakers and company management teams. Policymakers are increasingly defensive in their policy mix. However, management teams appear optimistic about the demand outlook for their businesses, especially those facing the consumers. This is largely due to the boom that most Mexican consumers have been enjoying. Employment stands at its highest level in years (with an unemployment rate of 3.9%) and remittances (mostly from Mexicans living in the neighbouring US) have grown 28% in Mexican peso in the year to date. Although the sanguine mood of the policymakers has been tempering consumer sentiment, which remains at moderate levels, consumer spending and credit are nonetheless growing at a healthy pace. Accordingly, banks are seeing strong growth in the demand for consumer loans and the use of credit cards, and a number of retailers are enjoying robust same-store sales growth. This sector (in particular segments such as convenience stores, food retail and casual dining) is also benefiting from the shift from informal trading to formal, more sophisticated outlets. Mexico has a much larger informal sector than many other emerging countries, with strong scope for growing formalisation.

Mexico’s competitiveness has improved significantly in the years since the global financial crisis. As labour productivity in China has been declining, Mexico has benefited from the decision of large manufacturing companies to resettle their activities closer to the important end-user market of the US. It has also continued to see a flow of US manufacturing capacity moving across the border to take advantage of its stronger economic growth, lower cost of labour and convenient location. More recently though, as the strong dollar and low oil price weighed on US manufacturing orders, Mexico has also seen a slowdown in its own manufacturing sector (as much of it is intricately linked to US supply chains).

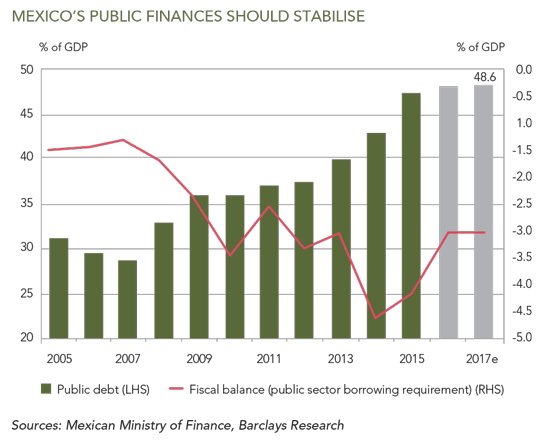

The challenges that Mexican policymakers face are not negligible. In the last six months, the Mexican central bank (Banxico) has had to raise its benchmark rates by a total of 125 basis points in order to shore up support for the peso, which has seen a steady decline since the end of 2014. The currency’s high liquidity and low yield make it an easy proxy for investors who want to take a short position in emerging market currencies, a popular trade the last couple of years. The authorities have adopted more stringent fiscal measures to bolster state revenues and to counter the effect of low oil prices on the external accounts. (While oil and gas are not as material for Mexico as they are for some of its Latin American peers, the country is a net exporter of oil.) The timing of liberalisation of the energy industry (previously monopolised by troubled state giant Pemex) has been unfortunate: it came amid collapsing commodity prices, resulting in lower-than-expected revenues from oil field auctions. The result has been a widening in the country’s twin deficits (fiscal and current account), an additional source of vulnerability for the peso. Although foreign direct investment has continued to increase, the economy has grown more vulnerable to external crises and the currency has played the role of the shock absorber.

Of course, it should be underlined that given the linkages of the Mexican economy to its wealthy northern neighbour, it is important for the country’s economic performance that US growth remains at least benign. Also, the possible election of Donald Trump (who has adopted a hostile stance towards Mexico) as US president is a risk. In addition, prospective investors need to take note of the early signs of a rise in domestic Mexican populism.

A number of Mexican companies, particularly in the consumer sector, are on our radar. These include Femsa, a Mexican-based multinational which (among other businesses) owns the country’s largest beverage bottling company, as well as the leading convenience store chain Oxxo and a 20% interest in the brewer Heineken NV. We also like Alsea, which operates fast-food and casual-dining brands in Mexico, broader Latin America and Spain. However, we believe their valuations are too demanding, and we are happy to remain patient and buy them only when the price is right. While the Coronation GEM Fund holds a small position in the US-listed railways operator Kansas City Southern for its Mexican exposure (Mexico represents more than half of the group’s profits), the fund currently only has one Mexican-listed holding: Grupo Financiero Banorte.

Banorte

We have been investors in Banorte since November 2014. Banking represents some 70% of its earnings, while long-term savings (insurance and asset management) make up 22%, followed by brokerage (5%) and its other activities (3%). Over recent years, the group’s profitability has been underwhelming due to a long period of record-low interest rates (which squeezed its net interest margins), the cost of integrating Ixe Banco (which focuses on the premium segment and had a high cost base) after its acquisition in late 2010 and low levels of leverage. A relatively new management team has embarked on initiatives to improve the utilisation of the bank’s balance sheet. The team wants to achieve a return on equity (ROE) target of 20% by the end of the decade – and, importantly in our view, management is aligned to this target. Some 40% of executives’ variable compensation will only be released as key ROE milestones are achieved.

We believe the ROE target will be achieved due to the following:

- The implementation of efficiency initiatives. These interventions are in the process of being adopted following an extensive consulting project, led by IBM. The initiatives include a new customer relationship management system, expanded use of online and mobile channels, and the optimisation of the bank’s fee and commission structure. In the next five years, the bank’s branch footprint will remain stable or grow smaller, while its assets are forecast to continue growing by double digits.

- A return of capital to shareholders. This could come in the form of larger ordinary dividends and, potentially, the payment of extraordinary dividends.

- Material improvements in the cross-selling of products to the bank’s existing customers. The bank has already seen some success on this front: the number of products sold per customer has increased from 1.7 to 1.83 products since the management team set on improving this metric. It believes this can grow to more than two products.

- A key shift in its client base. The breakdown of Banorte’s various customer segments is stunning: high-income customers represent 1% of its total number of customers, but provide 12% of profits, while middle-income customers are 4% of total and contribute 65% of profits! By comparison, 95% of its customers are low-income and generate 23% of profits. Management believes that 40% of the low-income customers are moving into the middle-income segment – this could present the bank with a big opportunity.

- Rising interest rates. Banorte is one of the most asset-sensitive banks in the country (meaning its assets re-price considerably faster than its liabilities) and will benefit from higher net interest income as the central bank of Mexico increases its policy rate.

- An increase in the contribution to earnings from the nonbanking subsidiaries of the group, especially insurance and pension management. Both stand to benefit from structural tailwinds and are high ROE businesses.

In terms of competition, Banorte (which has the fourth-largest share of the loan market), along with other players, are taking market share off the embattled Banamex (the number two player, owned by Citigroup). While competition is robust, generally product pricing remains rational, as we understand from our conversations with a number of management teams in the sector.

While we believe Banorte offers a strong investment case, governance risk has deterred investors over the past two years. Banorte’s chairman Carlos Hank González is the former CEO and majority shareholder of Grupo Financiero Interacciones. His family holds a stake of more than 70% in this Mexican financial institution, which is mostly focused on infrastructure loans. Investors were concerned that he might attempt to force a merger between the two companies, to the detriment of Banorte’s minority shareholders. However, Hank González has repeatedly denied this. Last month, he backed this up with more concrete action. He suggested a change in the company’s bylaws that will ensure that any acquisition proposal for a related party (e.g. Grupo Interacciones) has to be approved not only by Banorte’s audit and corporate practices committee and the board, but also be put to a shareholder vote. This should allay any lingering corporate governance concerns.

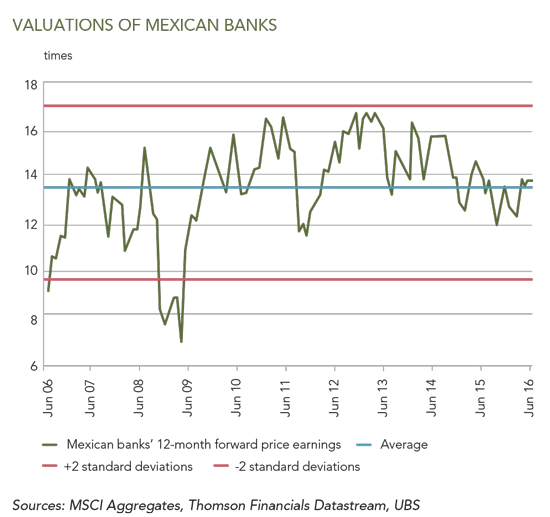

From a valuation point of view, Mexican banks in general look rather pricey compared to their emerging market peers. However, compared to their own history, valuations are in line with the average forward price earnings multiple over the past ten years. The banks are also trading below their average price-to-book levels over the same time period. Banorte has appreciated nicely since our initial purchase. It can currently be bought for approximately 14 times one-year forward earnings or 1.8 times book value – reasonable, given the robust earnings growth we expect in the coming years. Accordingly, Banorte remains a holding of the Coronation GEM Fund.

This article is for informational purposes and should not be taken as a recommendation to purchase any individual securities. The companies mentioned herein are currently held in Coronation managed strategies, however, Coronation closely monitors its positions and may make changes to investment strategies at any time. If a company’s underlying fundamentals or valuation measures change, Coronation will re-evaluate its position and may sell part or all of its position. There is no guarantee that, should market conditions repeat, the abovementioned companies will perform in the same way in the future. There is no guarantee that the opinions expressed herein will be valid beyond the date of this presentation. There can be no assurance that a strategy will continue to hold the same position in companies described herein.