United States - Institutional

United States - Institutional

Long-term focus critical when investing amid increased risk

22 June 2015 - Coronation Insights

Global equity markets look set to face a strong headwind as the era of cheap money comes to an end, cautions Coronation Fund Managers.

Record-low bond yields and interest rates have fuelled a phenomenal rise in almost all asset prices over recent years. Corporate profitability has benefited from the low cost of borrowing, and companies have been doing record levels of share buybacks, raising money in the debt market at very low rates. Value accretive mergers and acquisitions have followed, specifically in the property sector.

However, this powerful propellant of asset prices will fall away when global monetary policy starts to normalise. While the timing of the first interest rate hike in the US may be uncertain, early inflation pressure is emerging as wages start to climb in a tightening labour market. Higher rates will have negative implications for all asset classes: equities, listed property, private equity, commodities and housing.

“Amid this looming volatility and the threat of probable rerating, we believe the central tenets of our investment philosophy - a long-term horizon and a valuation-driven investment process - have never been as relevant,” says Neville Chester, senior portfolio manager at Coronation.

As markets grow frothier, the noise and the pressure to focus on short-term positions are increasing. This pressure to perform in the short term may expose investors to significant long-term investment risk. A case in point: most European bonds, which offer absurdly low yields. If you capitulate and invest in them now, you are likely to lose out in the long term by locking in record low interest rates.

“At Coronation, our long time horizon (of more than five years) allows us to make the best investment decisions for our clients, and to ensure the preservation and growth of long-term capital,” says Chester.

Key to Coronation’s investment philosophy is a disciplined approached to determining the real value of a business, with the aim of identifying mispriced assets that are trading at a discount to their normalised long-term values. The two most important aspects in valuing a business is determining its future earnings streams and deciding on the correct discount rate. The discount rate determines the premium an investor should demand to compensate for the opportunity cost and risks associated with the investment.

A key input in deciding on the appropriate discount rate is the US 10-year bond yield, which serves as the global risk-free rate. For investors who use the current near record-low yield (of around 2.5%) as the building block for their valuations, virtually every investment out there looks like a ‘buy’. However, the historic average of the US 10-year bond is between 4% to 5% and this level is more appropriate.

“We believe using a normalised, higher rate is prudent and more appropriate, particularly ahead of an era of rising interest rates,” says Chester. As a result, Coronation is using a higher discount rate in their asset valuations – and expecting lower investment returns in the future. A large portion of the returns generated across asset classes the past few years has been driven by re-rating as opposed to fundamental earnings growth.

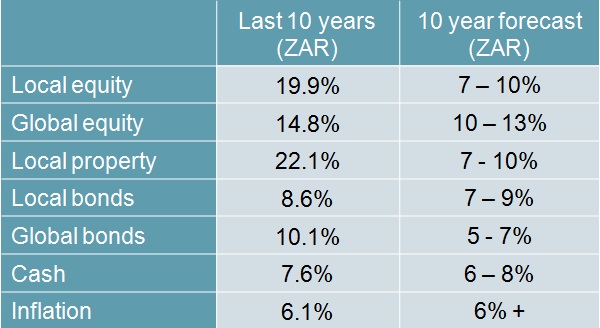

Table 1: Expected asset class returns (as at 30 April 2015)

Coronation Fund Managers forecasts. While these forecasts are not guaranteed to occur, they are based on our best estimates of possible future returns and represent a more prudent basis for informing planning assumptions than historical results achieved over the past decade.

As Coronation continues to caution about expecting much lower returns in the future, its exposure in multi-asset funds to domestic equities, in particular, has been sharply reduced. Global equities, specifically in emerging markets, continue to offer better value. “It is difficult to be optimistic about local prospects and the damage to our economy caused by Eskom’s failure to provide sufficient power cannot be underestimated,” warns Chester.

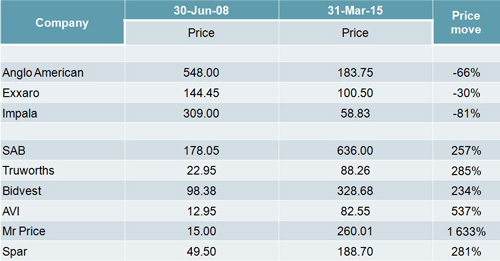

However, investors need to take note of a wide valuation gap that has opened up between domestic industrial shares and the commodity sector:

Table 2: Resources vs Industrials

Due in part to a glut of supply in recent years, commodity prices (and mining shares) have been under pressure and are currently trading below Coronation’s assessment of normalised levels. “As suppliers cut back their output, we expect commodity prices to revert to normal,” says Pallavi Ambekar, who co-manages the Coronation Top 20 and Market Plus funds with Chester. “While we don’t know how long and deep the current cycle will be, we believe three companies in particular offer investment value: Anglo American, Exxaro and Impala Platinum.”

Mondi remains a large holding in the Coronation Top 20 fund. In recent years, the company has invested extensively in its capacity in Russia and Eastern Europe, improving efficiencies and dramatically lowering its costs. Another substantial holding is Standard Bank, which should benefit from its exposure to faster-growing markets in Africa.

As asset prices tend to extreme levels, volatility and the scope for sharp losses will increase. “Patience and a focus on the long term are necessary to avoid getting caught up in the hype and making a mistake,” says Ambekar.

Disclaimer

Any information being provided herein (the “Information”) is not designed for use in any jurisdiction or location where the publication or availability of the Information would be contrary to local law or regulation. If you have access to the Information it is your responsibility to be aware of and to observe all applicable laws and regulations of any relevant jurisdiction and it is recommended an investor first obtain appropriate legal, tax, investment or other professional advice prior to acting upon the Information. Coronation Asset Management (Pty) Limited is an authorised Financial Services Provider regulated by the Financial Services Board of South Africa. Coronation Asset Management (Pty) Limited is a subsidiary company of Coronation Fund Managers Limited, a company incorporated in South Africa and listed on the JSE (ISIN: ZAE000047353). The Information is for information purposes only and does not constitute or form part of any offer to the public to issue or sell, or any solicitation of any offer to subscribe for or purchase an investment, nor shall it or the fact of its distribution form the basis of, or be relied upon in connection with, any contract for investment. Unit trusts should be considered a medium- to long-term investment. The value of units may go down as well as up, and is therefore not guaranteed. Past performance is not necessarily an indication of future performance. Note that individual investor performance may differ as a result of the actual investment date, the date of reinvestment of distributions and dividend withholding tax, where applicable. Where foreign securities are included in a fund it may be exposed to macroeconomic, settlement, political, tax, reporting or illiquidity risk factors that may be different to similar investments in the South African markets. Fluctuations or movements in exchange rates may cause the value of underlying investments to go up or down. Coronation Management Company (RF) (Pty) Ltd is a Collective Investment Schemes Manager approved by the Financial Services Board in terms of the Collective Investment Schemes Control Act. Unit trusts are traded at ruling prices set on every trading day. Unit trusts are allowed to engage in scrip lending and borrowing. Coronation is a Full member of the Association for Savings & Investment SA (ASISA).Opinions expressed in this document may be changed without notice at any time after publication. Nothing in this document shall constitute advice on the merits of buying and selling an investment.