United States - Institutional

United States - Institutional

Investment views

Demonetisation: India’s bolt from the blue

What did this programme really achieve?

- Demonetisation failed to punish beneficiaries of illicit activity/parallel market operators as intended

- Constraints on withdrawals relative to immediate high deposits led to excess liquidity in the banking sector

- Money market and similar instruments became attractive savings vehicles, with above-inflation interest rates

- The demonetisation process indirectly caused some of the issues that led to defaults by some non-banking finance companies

IT’S BEEN JUST over three years since 8 November 2016 when, without prior warning, the government of India announced a cabinet decision that all existing Rs500 and Rs1 000 notes (then worth $7.50 and $15.00, respectively) would cease to be legal tender from midnight. In light of the deceleration of India’s economic growth rate and liquidity issues in its banking sector, it is worth revisiting the impact of this ‘demonetisation’ programme on the intervening years.

At the time of the announcement, the government also laid out the path forward to manage this exercise. The following day, 9 November, would be a banking holiday when no deposits or withdrawals would be allowed. From 10 November, all holders of these notes would have to deposit them into a bank account or exchange them for either smaller denomination notes or a new series of high-denomination notes before the end of the calendar year. The old notes could be used for a short time for a narrow range of transactions, with certain public services such as healthcare and train fares listed as exemptions, but by and large, the soon-to-be defunct denominations were essentially useless to holders.

I’ve looked for data as to what proportion of the total value of outstanding notes these cancelled notes represented at the time, and there is a wide variety of estimates.

Evidence suggests that the cancelled notes represented about 25% of total notes in circulation by volume. However, since these were the two highest denomination notes in the country, they represented over 90% of cash currency in circulation by value. Reserve Bank of India (RBI) figures show that the total value of notes in circulation at the time of the decision amounted to $260 billion, so something in the region of $240 billion needed to be deposited or exchanged by the end of December 2016.

THE ELEMENT OF SURPRISE

A variety of reasons was given by the government for this drastic measure. Most apparent was the need to curb tax evasion by mainstreaming the shadow economy. In theory, this move would either spook tax evaders and other holders of illicit funds for fear of having to disclose their source of income, causing them to cut their losses, or the money would leave the shadow economy and enter the formal economy under the oversight of the banking system and tax authorities. Other reasons cited were along the same lines, such as halting counterfeiting activities and weeding out the proceeds of corruption.

Both individually and as a collective, the aims were laudable, but of course the true measures of success for any policy are, first, whether it achieves its targets, and secondly, the overall cost of implementation. Economists refer to the latter as a ‘cost-benefit analysis’, and it has been the subject of much debate in India as to whether this exercise was a success overall.

THERE IS (ALWAYS) A WAY

As mentioned, the government expected a material proportion of the cancelled bank notes to be of dubious origin and to leave the system permanently, as their holders would not be able to explain the source of funds. On this metric, the demonetisation drive failed completely.

The RBI estimates that 99.3% of total cancelled notes were either deposited or exchanged. This is an astonishingly high proportion, both in absolute terms and relative to government expectations of 80% to 85%. In discussions with bank executives with whom our investment team meets when in India, the common theme was that people found a way to deposit their illicit money.

The most frequent tactic was to divide large sums into smaller amounts that fell below the suspicious threshold, and then have several ‘friends’ deposit the money into their own accounts, to be subsequently withdrawn and returned to the originator for a fee or commission.

There were also reports of many businesses accepting the cancelled notes as payment for goods and services, since the businesses could then deposit the money under the pretext of having been in possession of them before they were cancelled.

UNINTENDED CONSEQUENCES

As could be expected in a society where more than 95% of transactions are cash, the demonetisation programme had quite an impact on ordinary citizens. Even with flawless implementation, it would have been difficult to avoid large-scale disruption – and the implementation was far from flawless.

In the days and weeks that followed, India’s national pastime became queuing at banks and ATMs to deposit money and withdraw new notes. The banking system was not prepared – there was an insufficiency of new notes and daily withdrawal limits meant that money deposited far exceeded the amount that could be withdrawn on a system-wide basis.

There was also a shortage of smaller-denomination notes, as most people did not want to withdraw Rs2 000 ($22.50) notes, which is a significant amount of money in a low-income country. Additionally, large notes are not readily accepted by merchants, many of whom found themselves struggling due to the lack of lower-denomination notes for their cash floats.

The temporary flood of liquidity into the banking system also had consequences. The shortage of notes and staggered withdrawal limits resulted in people ‘parking’ their money in fixed-term deposits or money market funds to get returns. Since one could earn interest rates higher than inflation in India (positive real rates), this made sense relative to withdrawing cash that earns nothing in the holder’s hands.

A FATAL FLAW

Much of this money found its way into the wholesale funding market, allowing India’s non-banking financial companies (NBFCs) to go on a lending spree just as the economy started to slow. One such NBFC, Infrastructure Leasing & Financial Services, defaulted on its debts in August 2018. The default was caused by poor lending practices and a mismatch between the long-term funding required for infrastructure and road projects, and the shorter-term nature of its borrowing book.

The default alarmed the market and led to a flight from the money- and wholesale-funding markets to regular savings accounts with banks, some of which was then withdrawn as cash. Other NBFCs have also since defaulted, most prominently Dewan Housing Finance Limited.

For now, the initial contagion seems to have been contained, but many of the weaker NBFCs have been forced to cut back on loan growth to preserve capital, as wholesale funding dried up for them, or at least was only possible at very high rates that squeezed their profit margins (net interest margins).

The recent slowdown in economic growth in the country is therefore partially attributable to the consequences of demonetisation.

THE OPPORTUNITY

A positive by-product of the programme was seen in some of the smaller private sector banks that our analysts assess. These banks had been investing in growing their branch infrastructure for several years in the hope of attracting a greater proportion of their revenue from current and savings accounts (CASA). A higher CASA ratio is desirable, since the average interest paid on these accounts is lower than other potential sources of funding.

Customers who deposit money in a bank are also more likely to make use of any retail banking offering available, take out loans or purchase other financial products.

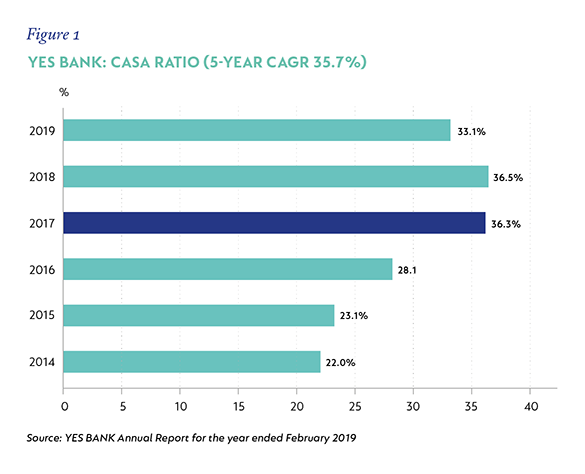

A good illustration is Yes Bank, which was India’s fourth largest private sector bank at the time of the demonetisation exercise. In February 2016 (the financial year-end for most Indian businesses as it coincides with the tax year-end), CASA deposits made up 28% (see Figure 1) of Yes Bank’s total deposits. By the time end-February 2017 came around, just four short months after the recall, CASA accounted for 36% of total deposits.

At the time, management attributed the spike to a rush of deposits by new customers who opened accounts at any bank they could to avoid dealing with the chaos at the bigger banks. Further, the lack of notes and the economic slowdown that followed demonetisation meant the average duration of deposits was longer than originally expected.

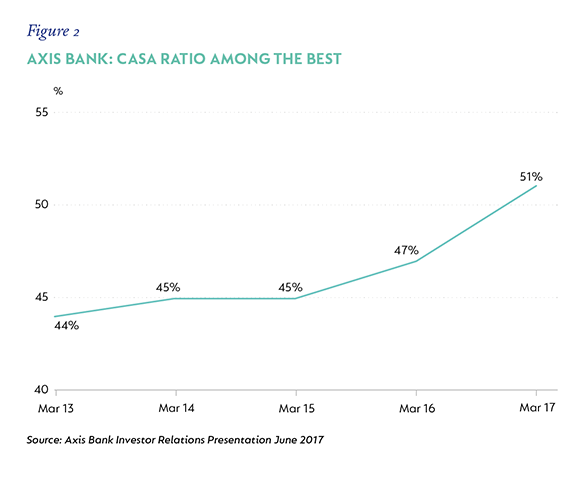

Another private sector bank we follow, with a more established retail franchise, also saw a significant jump in its CASA ratio. Axis Bank’s ratio exceeded 50% for the first time in 2017 (see Figure 2), jumping 4% as a result of demonetisation-related inflows.

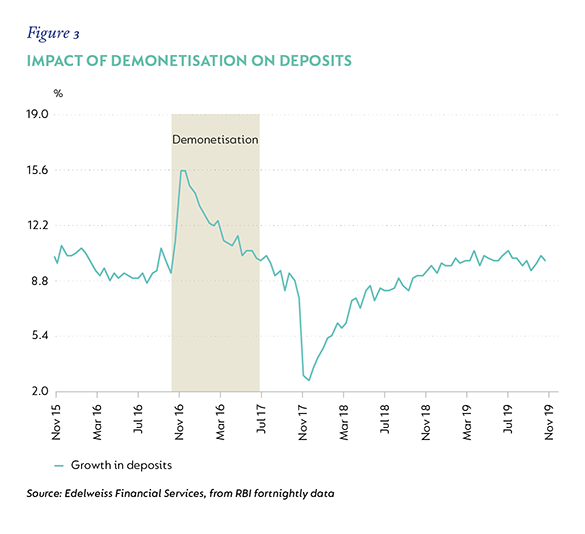

Figures 3 and 4 illustrate the impact demonetisation had on deposits and currency. Figure 3 tracks total deposits in the banking system and shows that there was a big spike in deposit growth when the programme started (it would have been even higher had no withdrawals been allowed), but collapsed completely thereafter as people were able to withdraw much of the money they had deposited.

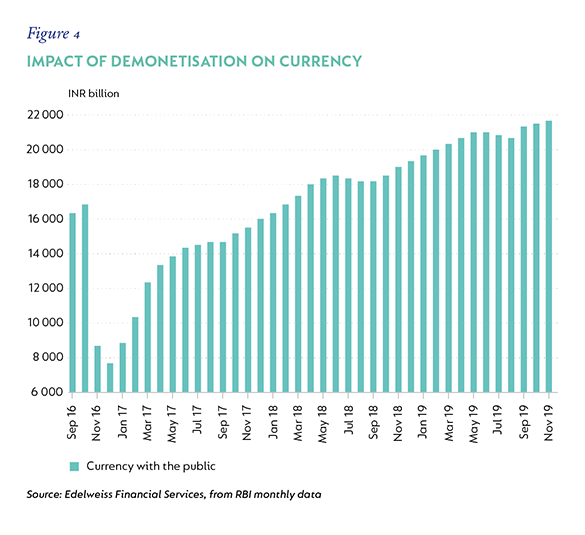

Figure 4 shows how total currency in circulation collapsed before resuming its upward trend. This counters the argument that the programme would help the transition to a ‘cashless’ society over time.

BUT WAS IT WORTH IT?

Based on the evidence presented, it is my conclusion that the demonetisation exercise did not achieve what it set out to do, or certainly not what the government argued would be achieved at the time. When one considers the short-term disruption it caused to Indian society and the medium-term impact it had on the NBFCs, it is probably fair to state that the net impact on India was negative.

This article is for informational purposes and should not be taken as a recommendation to purchase any individual securities. Some of the companies mentioned herein were held in Coronation managed strategies as at 31 December, however, Coronation closely monitors its positions and may make changes to investment strategies at any time. If a company’s underlying fundamentals or valuation measures change, Coronation will re-evaluate its position and may sell part or all of its position. There is no guarantee that, should market conditions repeat, the above-mentioned companies will perform in the same way in the future. There is no guarantee that the opinions expressed herein will be valid beyond the date of this presentation. There can be no assurance that a strategy will continue to hold the same position in companies described herein.

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter