United States - Institutional

United States - Institutional

If you want to see the sunshine, you have to weather the storm, but in order to weather and navigate the storm, you have to adjust your sails. At Coronation, we are constantly questioning the assumptions that underlie our valuation-driven approach to investing so as to provide our clients with portfolios that are anti-fragile and best positioned to withstand the shorter effects of adverse volatility.

2018 was a difficult year for emerging markets and more especially for emerging market fixed-income investors. The year started with tremendous promise as emerging market bond yields and currencies appreciated markedly. Then the tide turned. The US/China trade war escalated, raising concerns about global growth expectations, which we now know to be too high. Around about the same time, the US Federal Reserve (Fed) started to lift its expectations for the US economy and consequently, its expectations around US interest rates. This combination of higher-than-expected US rates, lower global investor confidence and slower global growth, painted a very poor picture for emerging markets. This change occurred so suddenly that many authorities in these markets were left with very little time to react, so valuations of emerging market currencies and bonds had to adjust and act as the pressure valve. Emerging markets with large external deficits were the first to suffer, as was evidenced by Turkey and Argentina, which were both down between 30% to 50%. Emerging market bonds were down 7.9% in US dollars for 2018, while emerging market bonds in their local currencies only returned a paltry 2.9%.

South Africa didn’t fare much better, as concerns on the key policies (land, mining charter and state-owned enterprise (SOE) reform) and much slower growth weighed heavily on local asset price performance. The All Bond Index (ALBI) was up 7.7% for 2018, however the rand was down 13.8% to the US dollar, bringing South African government bond returns in US dollars to -7%. Performance across the various parts of the yield curve was pretty balanced, with the very front end of the curve outperforming. We see the performance at the front end of the yield curve (one to three year) as unsustainable given that this performance was in large part driven by the buyback of bonds in that area of the curve as part of National Treasury’s switch auction programme. South African government bonds had a rollercoaster of a year, with the benchmark bond starting the year at 8.6%, hitting a high of 7.9%, then a low of 9.4% and ending the year at 8.87%. Inflation-linked bonds (ILBs) continued to suffer as real yields moved almost as much as nominal bonds (I2025 – low: 3.15%, high: 2.08%) primarily due to the adjustment lower in both medium- and longer-dated inflation assumptions. Due to the higher duration that these bonds carry, ILBs only managed to eke out a return of 0.3% for the year.

Are there rays of sunshine on the horizon for South African government bonds and emerging markets? Or are there more adjustments needed from a valuation and portfolio perspective in order for us to weather this storm?

Over the next two years, global growth is expected to decelerate from 3.2% to 3.0%, driven primarily by a deceleration in growth coming out of developed markets (2.3% to 1.7%) and China (6.6% to 6%). Emerging market growth is expected to remain relatively stable around 4.6% but with quite a bit of disparity. The only emerging market countries that are expected to see an increase in growth over the next two years are Brazil, Russia, India and South Africa. Russia remains at risk of further US sanctions, Brazil’s outlook remains clouded by high debt levels and a new political regime, while India enters an election year in which the ruling party is at risk of losing its majority. This only leaves South Africa as a somewhat more “stable” emerging market where growth is expected to pick up and inflation remaining relatively stable, closer to the midpoint (4.5%) of its target band.

South Africa itself still faces risks. The largest of which remains Eskom, which has been a concern for the fiscus and a headwind to sustainable growth. More recently, Eskom has suggested that government would need to take on close to R100 billion (2%-3% of GDP) worth of debt onto its balance sheet in order to render the beleaguered SOE’s debt servicing costs more practical. Although this is not enough to blow up South Africa’s fiscal metrics, the precedent it sets for other SOE bailouts will not be looked at favourably. Discussions around Eskom in the last few months have intensified, with intentions to now reduce headcount in areas that have been bloated (mid- to high-level management). If the debt transfer is to happen, it has to be:

- temporary in nature (e.g. government agreeing to meet debt servicing costs over the next three years only);

- accompanied by a plan to reduce costs in overextended areas and;

- a plan to restructure the SOE into a financially viable vehicle (selling off assets or parts of the company to inject much needed capital).

As has been the case in South Africa over the last year, revelations over how badly state capture has ruined SOEs has brought the stark realisation that many of them are in a much worse position than was initially suggested. Drastic action needs to be taken in order to turn these SOEs around and reignite the country’s growth engine. The process has already started, but now needs to be accelerated in order to alleviate ratings agency concerns and prevent a full downgrade to sub-investment grade (Moody’s is the only agency that still has South Africa on an investment-grade rating).

Thankfully, the economy has been relatively resilient and has the potential to grow quite quickly from here if key issues are addressed. Investment has been very low and capital stock replacement has not occurred for quite some time. If concerns around Eskom are alleviated and we have a market-friendly resolution to the land expropriation without compensation debate (as has been suggested by Government), then we could see a meaningful pickup in growth, even well above the 1.8% consensus expectation over the next two years. In addition, with inflation remaining relatively well behaved and lower oil prices providing a boost to the consumers, we could see this accompanied by a further boost to consumer spending (60% of GDP), which could provide further upside. Overall, one can remain cautiously optimistic on the South African outlook for the next two years.

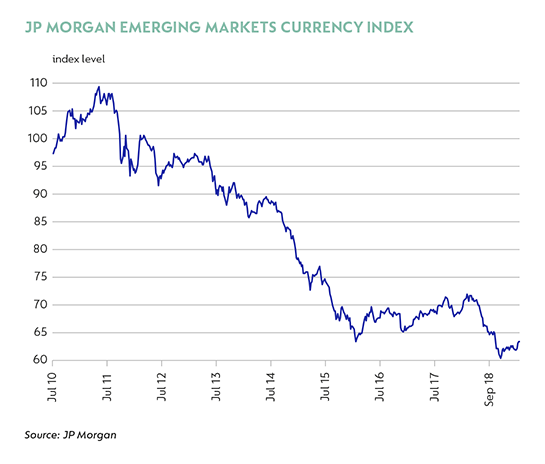

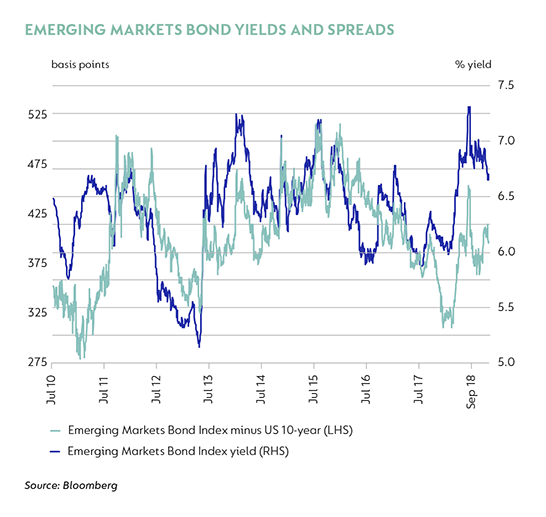

A change in the expectations for US interest rates and/or a resumption in the escalation of the US/China trade war could once again sour emerging market sentiment. However, valuations of emerging market bonds and currencies are now much more representative that when this occurred in mid-2017. Emerging market currencies are at the weakest point seen in the last 10 years, and emerging market bond spreads (relative to the US 10-year bond) and yields are now at their long-term average.

The graphs suggest that even if there is a resumption in the risk-off sentiment towards emerging markets, the valuation cushion that is now present is much healthier than in previously experienced episodes.

In the US, recent Fed rhetoric and revisions have all suggested more downside to growth over the coming year, which has lowered expectations for both interest rate hikes and the long-term level of interest rates in the US. The Fed has signaled two more hikes in 2019 (taking the policy rate to 2.9%) and a long-term neutral interest rate of 3%. Although the front end of the US curve currently fully prices this in, the US 10-year treasury bond (US 10y) remains well below this at 2.7%. This suggests that the level of US 10-year rates is once again too low. In our assessment, it should be closer to 3.3% (1.3% real policy rate + 2% inflation). Despite this, South African government bonds don’t look unattractive.

Our fair value analysis, using the US 10-year rate of 3.25%, South Africa’s expected inflation of 5.5% (which is above our expectations), US expected inflation of 2% and the 10-year average South African credit spread of 2.9% results in a fair value for South African government bonds of 9.7% (3.3% + 5.5% - 2% + 2.9%), which is close to current levels of the South African 10-year bond yield (9.6%), implying there is still some value in South African government bonds. However, with only a cautiously optimistic view on the local yield, how does one protect a bond portfolio?

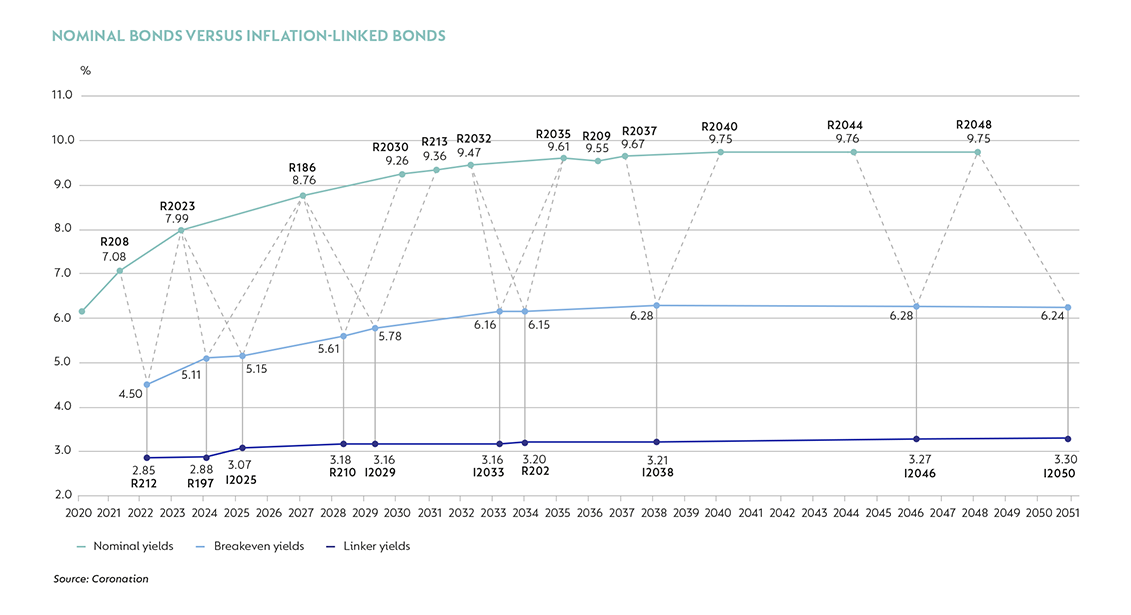

The natural answer to this would be ILBs, given that in the event of a risk-off sell-off, the rand would also sell off, pushing inflation higher and causing the central bank to readjust rates. However, given the very high duration that these instruments carry, one has to be very careful which part of the ILB curve one invests in. The red/middle line in the graph below shows where the market expects inflation to average over various maturities. Given that we only expect inflation to average 5.3% over the next two to three years, it is only the bonds that have an implied breakeven inflation of close to 5.3% that look interesting. This rules out any ILB with a maturity longer than the year 2025. In addition, ILBs carry a materially longer modified duration (capital at risk) than nominal bonds, e.g. I2046 has a modified duration of 18.7 years, while the R2048 (equivalent nominal bond) has a modified duration of 9.2 years - if both the ILB and nominal curve move 100 basis points (bps) higher, one would lose 9.5% more being invested in the I2046 than the R2048. This means that to be invested in longer end ILBs, the implied breakeven needs to be quite a bit lower than the current 6.5% (closer to 5.5% actually) for it to be an attractive investment. Shorter end ILBs, however, at current levels of a 3% real return and a more realistic break-even inflation do look much more attractive and do warrant positions in a bond portfolio (albeit not materially large).

South African government bonds mostly reflect realistic expectations for the local economy, although they have benefitted from a turn in global sentiment recently. South African bonds compare favourably to their emerging market peers, relative to their own history, and still offer a respectable cushion against further global policy normalisation. At current levels, the yields on offer in the local bond market are fairly valued relative to their underlying fundamentals and warrant a neutral to modestly positive allocation. The relative underperformance of ILBs.

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter