South Africa - Institutional

South Africa - Institutional

4 MONTHS, 2 MILLION AND STILL RISING ...

“All we know is still infinitely less than all that remains unknown.” – William Harvey (16th century English physician)

What a long year these last three months have been. Few natural disasters threaten more loss of life, economic disruption and social disorder than large-scale disease outbreaks. It’s been four months since Covid-19 first emerged, with more than two million people infected at the time of writing; and the subsequent pandemic has changed all of our lives drastically in a short space of time – obsessive handwashing, Zoom calling and wearing a mask in public.

I am writing to you at an unprecedented time in our global history when billions of people around the world are sheltering at home. I am sure many of you, like me, have spent hours watching the news, which has been filled with eerie scenes from the now-quiet cosmopolitan cities of New York, Rome and London.

And with this new way of life we are facing a compound set of challenges that I, for one, couldn’t have imagined in my wildest dreams – the disease itself, quarantine and isolation, remote schooling, working from home and, of course, having to suit up like a stormtrooper before heading out to get bread and milk.

It has become increasingly clear that this is one of the greatest pandemics since the Spanish flu wreaked havoc on the global population 102 years ago, and it will leave lasting scars on the global economy. Experts predict that this year we will see the greatest economic contraction since the Great Depression ended 80 years ago.

March has been a historically bad month for the global economy. The market pandemonium has been surreal to witness. But we know that the true scale of the hit to the real economy is yet to become painfully clear.

There is no doubt that we are currently dealing with a public health-driven humanitarian crisis. The lockdowns have been an important short-term emergency lever to prevent a catastrophic death toll. We have thankfully bought some time in the global fight against this pandemic, but at a significant cost as we prepare ourselves to deal with an economically driven humanitarian crisis next.

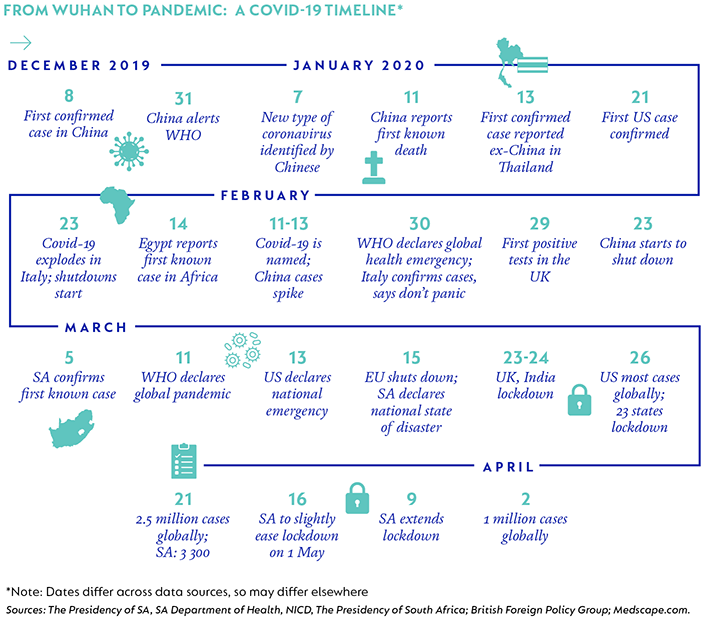

LOOKING BACK A FEW SHORT MONTHS AGO ...

The first case of (the as yet unknown) Covid-19 infection was reported in December 2019, and on 31 December, the Chinese government alerted the World Health Organisation (WHO) to a rise in cases of pneumonia (coronavirus) of an unknown origin in Hubei Province. On 7 January 2020, Covid-19 was identified, Wuhan was quarantined on 23 January, and on 11 March the WHO declared it to be a pandemic that was likely to become global in scale (at the time there were 118 000 cases reported across 114 countries).

Leadership responses have varied. One of the most exacerbating factors of this pandemic has been its exponential rate of growth. This means that if leaders miss two or three doubling infection cycles due to delayed responses, the problem will be eight to nine times worse by the time governments eventually tackle the spread of the disease.

When it comes to assessing and acting quickly and decisively in response to the looming public health crises, some leaders stood out. These include Tsai Ing-wen of Taiwan, Jacinda Ardern of New Zealand, Angela Merkel of Germany and our own President, Cyril Ramaphosa.

Not only were they quick and decisive in their reactions, but they were also truthful with their citizens about the risks faced and persuaded many people to act for the public good through their own example.

Unlike the other countries mentioned above, South Africa is a developing country, and like many other developing nations, we do not have the resources or money to assist in this fight. We are unsure as to how practical a lockdown is to enforce, and we know that financial instability and a looming depression will inflict huge harm on developing countries like ours.

Regardless of these tough choices and their worrying impacts on our society, I am proud of how our country has responded to the pandemic. South Africans have come together to implement a nationwide wall of defence. Much of it is not easy. We are a unique country and we need a unique approach. Unclear of the future, our initial actions have served to contain the spread of the virus and, in the process, bought us some valuable time to allow better preparation of the healthcare sector and better decisions about what comes next. Our economy cannot afford a long shutdown and hence our exit strategy from the current lockdown is complex and critical.

But this is not something that we are uniquely struggling with. All countries are dealing with how to phase a reopen of their economies, with the decision being informed by extensive testing and tracing (something that is easier said than done, given the global shortage of the equipment required). And above all, to ensure that a reopen is done in a manner that does not restart an aggressive rate of infection. As we are dealing with so many unknowns, there is simply no way of knowing exactly what a perfect response should be. But any responses in a swiftly evolving and complex crisis are likely to be imperfect at best. We need to learn to accept this.

Lessons learned along this journey will inform many of the decisions that governments make for society, and that we make as individuals, businesses and communities in the near term, medium term (until effective medical treatments become available) and the long term (until a vaccine becomes available).

When do we return to normal? Probably never to the way of life we knew before. I have no idea what the near-term future looks like, but I am very sure that some of our behaviours have been altered forever (and hopefully for the better); and that we will be called upon to reimagine our business and community interactions for, at the very least, the next 12 to 18 months. One thing is for sure, we won’t be shaking hands for some time to come.

THIS IS A UNIQUE EDITION ...

Our entire edition for this quarter has been adjusted to talk through the virus and its impact on our client portfolios. Our lead article, “A time of crisis”, written by CIO Karl Leinberger and John Parathyras, was published earlier this month. It summarises our team’s extensive research on the virus and the short- and medium-term economic impacts of the global response. We have updated it to reflect new information as the crisis has evolved over the past two weeks (a long time in the life of this pandemic).

In her very sobering article, economist Marie Antelme weighs the costs of the global economic shutdown, while head of fixed income, Nishan Maharaj, provides a deep dive into the arena of credit, income and debt.

In his article on Naspers, portfolio manager, Adrian Zetler, discusses why we continue to find that the position has an attractive investment case in this troubled time and demonstrates its resilience during this time of extreme disruption. For the rest of this edition, we have taken the opportunity to publish the full strategy comments for our main portfolio streams, in which our portfolio managers share their thoughts on the current crisis, its market impact and how they have positioned their portfolios for context.

MAINTAINING OUR SERVICE TO YOU ...

The Presidency identified financial services companies as providing essential services during the Covid-19 lockdown and we remain operational during this time.

You can trust that we have worked hard to ensure an uninterrupted and high-quality service to you. At the same time, as always, our first priority has been to ensure the well-being and safety of our clients and staff.

This means that we invoked our robust business continuity plans and extensive remote working capabilities. All of these have been in operation for more than a month, with about 85% of our employees working from home. We expect this to continue. However, there are understandably certain vital functions that need to be performed by certain team members in a highly controlled environment and our key staff performing these vital functions will be in the office daily.

IT’S ALL ABOUT SOLIDARITY

The nature and extent of Covid-19’s impact are pervasive and require strong cooperation between government and business. We continue to engage regularly as an industry participant and business to ensure that we collaborate with businesses, professional bodies and policymakers in South Africa to respond appropriately to the challenges we now all face.

At the very beginning, as a corporate and as individuals, we made financial contributions to the Solidarity Fund, as we believe that it is positioned to deliver maximum impact and relief to those most vulnerable to the harsh effects of this pandemic.

On Thursday 9 April, President Ramaphosa be-came the first world leader to announce that both he and his Cabinet were taking a one-third salary cut for the next three months, with the proceeds being contributed to the Solidarity Fund. He challenged all business executives in the country to heed his call and follow suit. Corporate South Africa has responded quickly, and I am very proud to announce that Coronation’s business leadership (consisting of 15 individuals), our non-executive directors and an additional 25% of our employee complement have voluntarily opted for a salary cut, with the proceeds being contributed to the Solidarity Fund.

Unlike the virus, humans make choices. Times are brutal – in our country and across the world. This pandemic, which took us all by surprise, is already taking a heavy toll – financial, social, emotional and mental. I give a special shout out to those parents, like me, feeling the strain of juggling working from home (and sometimes at the office), home-schooling kids, remote family care and home admin.

Coronation deeply values our continued partnership with our clients, which allows us to face this challenge together. We are indeed in unchartered waters. I believe that crises tell us a lot about the essence of people – their true nature. Some will disappoint. Others show immense courage, grit and compassion. The mark of the strength of any society is the ability to stay united in tumultuous times.

The one striking and exceptional thing that I have learned about South Africans is that our society and our people are remarkably resilient. We find ways to adapt, thrive and bounce back from adversity. This gives me great hope that by working together in a sensible and considered manner, we will navigate through this crisis.

I wish you, your family and your colleagues strength, fortitude and good health during these extraordinary times. Above all, make wise choices and I look forward to the time when we meet again in person.

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter