South Africa - Institutional

South Africa - Institutional

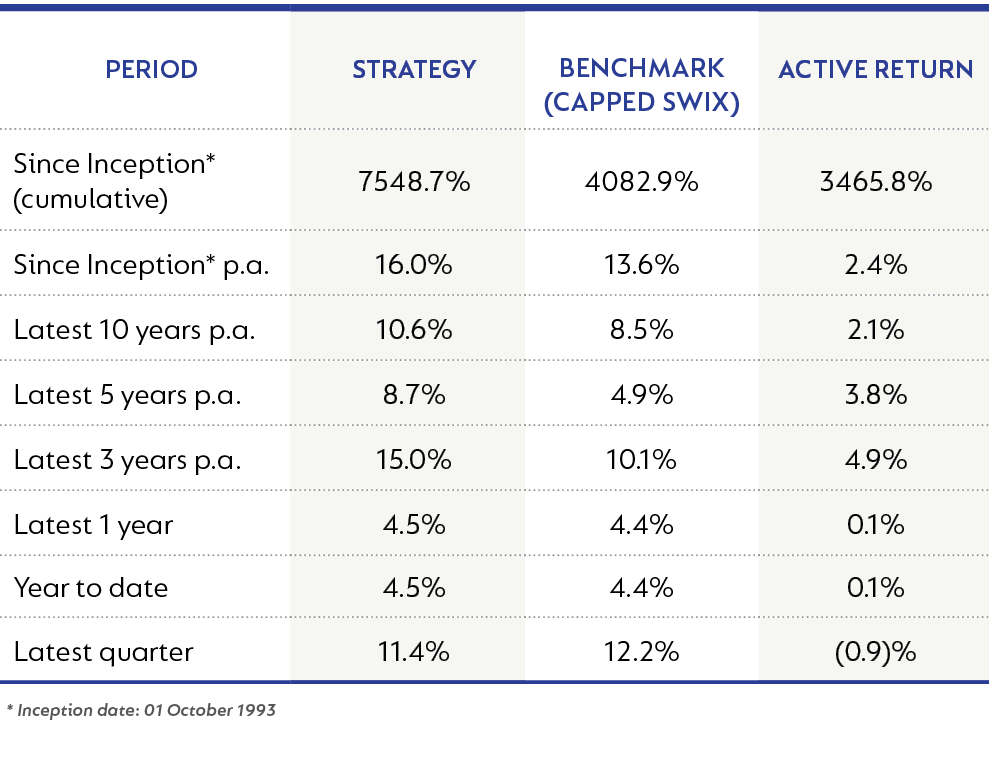

The Strategy returned 11.4% for the quarter (Q4-22), resulting in a return of 4.5% over the last year. The Strategy has performed well against its benchmark over all meaningful time periods.

2022 was a year of broad weakness across asset classes. Markets retreated off their January highs in the face of high inflation, rising interest rates and slowing growth. The MSCI All Country World Index (ACWI) ended the year -18% (after strengthening +10% in Q4-22). Europe has been particularly hard hit by rocketing energy prices. A recession is widely forecast across Europe and for the US in 2023.

The Strategy’s performance as at 31 December 2022 is shown below:

Geopolitical tensions remained high throughout 2022. Almost a year after Russia’s surprising invasion of Ukraine, the outcome remains uncertain. Escalation by a desperate Russia remains a risk. NATO and the European Union have emerged more united in the face of an increasingly polarised world order. China stuck doggedly to its zero-Covid policy for most of 2022, constraining mobility and economic growth. A sudden easing of Covid restrictions in the final weeks of 2022 should support economic growth in the year ahead, albeit raging infections in a population with limited immunity are a threat. The risks of investing in China remain heightened. President Xi Jinping tightened his control further in 2022: centralising power and decision making, enhancing state overview of everyday life, and increasing interference in the economy. Notwithstanding a Q4-22 rebound (MSCI China +14% in USD), assets remain cheap (FY decline -22%). Many good businesses with strong growth prospects and healthy balance sheets trade on low multiples. Strategy holdings names like Naspers/Prosus are expected to benefit from the country’s reopening.

Having rebounded off its Covid lows, the South African (SA) economy continues to struggle with low growth. Ageing underinvested infrastructure and poorly run state entities hamstring the economy. High levels of power outages render Eskom unable to increase planned maintenance sufficiently to bring down the high levels of loadshedding experienced during the second half of 2022. The resignation of Eskom’s CEO and COO during Q4-22 add further uncertainty. The Phala Phala fiasco was a reminder of just how fragile the political situation is. The rand weakened on the back of this but then recovered on the more positive outcomes of December’s ANC elective conference to end the year -6% versus the USD. President Cyril Ramaphosa’s re-election alongside several of his allies should enable ongoing, albeit slow, reform.

In US dollar terms, the FTSE/JSE Capped SWIX Index outperformed the global benchmark to end the year -4% versus -18% for the MSCI ACWI. When measured in local currency terms, the Capped SWIX returns were positive for the year (+4%) and the quarter (+12%). We believe SA equities are cheap and continue to deserve a place in our portfolios alongside global equities. They offer broad value across resources, global stocks listed on the JSE, and domestics.

The resource sector rose 9% for the year, helped by a strong Q4-22 (+16%). Energy prices spiked earlier in the year in the face of Russia’s invasion of Ukraine with a broader surge in commodities in Q4-22 as markets anticipated strong demand into 2023 on the back of China’s reopening. We expect energy markets to be tight over the medium term as demand remains robust during the transition to lower carbon energy sources and due to the lack of investment in new capacity over the last few years constraining supply. We have diversified our energy holdings across a broader basket of local (Sasol and Exxaro) and global names to reduce company-specific risk. All are expected to benefit from elevated cash flows which will support high levels of dividends and buybacks.

Despite slowing global growth into 2023, we expect broader commodity prices to remain resilient as constrained capital expenditure from major diversified miners since 2015 keeps markets tight. We hold positions in diversified miners such as Glencore and Anglo American. Both offer attractive free cash flow streams, even at more normal commodity prices.

The Strategy started 2022 with a sizeable holding in gold equities which was sold down in Q1-22 as gold stocks outperformed. The Strategy is under-weight both gold and PGMs today, preferring diversified miners and the energy plays.

The Financials Index returned +7% for the year and +13% for the quarter. The banks (+18% for 2022, +15% for Q4-22) continued their strong earnings recovery and are all expected to have surpassed their pre-Covid earnings during 2022. While costs and credit losses are normalising off low bases, good revenue growth (advances and rising interest rates) enabled the banks to deliver healthy profit growth. Corporate and retail clients with sound balance sheets are expected to withstand interest rate hikes. The portfolio has reasonable exposure to the banks via FirstRand, Standard Bank, and more recently Absa. Absa has shown strong growth off its pre-Covid earnings base, driven by market share gains and good operating leverage. While the share price has risen, multiples remain low in absolute terms and versus the other banks. With board and management succession issues resolved, and the Barclays separation complete, we expect Absa to continue delivering against its long-term targets.

Life insurers underperformed their bank counterparts (-13% for 2022, +4% for Q4-22) as they faced Covid-inflated mortality claims, weak equity markets, low growth, and competitive pricing in risk insurance. The Strategy does not own the life insurers, preferring positions in the banks and other financials.

OUTsurance (+9%), Transaction Capital (TCP) (+9%) and PSG Konsult (+14%) are sizeable holdings in the portfolio. All are expected to continue growing robustly.

The Industrials Index returned -4% for the year but was up strongly in the fourth quarter (+16%) as major constituents Naspers and Prosus delivered a whopping +25% and +24% respectively in the final quarter of 2022.

In line with the volatility experienced by China stocks over 2022 (declining on the perception of increasing political risk and then rebounding in response to an improved economic outlook thanks to easing Covid restrictions), the large Tencent holding in Naspers/Prosus was similarly impacted. In addition, Naspers/Prosus have created value at the holding company level through an accretive buyback programme. The discount narrowed by a third in recognition of both the value this transaction creates and the positive message it sends about management’s commitment to narrow the discount through optimal capital allocation.

Domestic stocks continue to offer attractive stock picking opportunities. Many are trading on high dividend yields too. The JSE has seen several buyouts by international bidders in the last few years, underpinning the value on offer. 2022 was no exception with Mediclinic and Massmart receiving buy-out offers. Our emphasis within the portfolio has been on finding businesses that can prosper even in a low-growth economy. Managers in these businesses are investing behind their expanding franchises, taking market share, and strengthening their moats. Examples include ADvTECH, Dis-Chem and Motus.

The Strategy continues to hold several global businesses listed in SA, all of which are attractive versus global peers. Examples include Richemont, British American Tobacco, Bidcorp, and an increased holding in Anheuser-Busch InBev (ANH) built up in Q4-22. Near-term inflationary pressures have weighed on ANH’s share price, but its long-term prospects remain solid. ANH has leading market positions, strong brands, scale benefits, healthy margins, and strong free cash flow conversion.

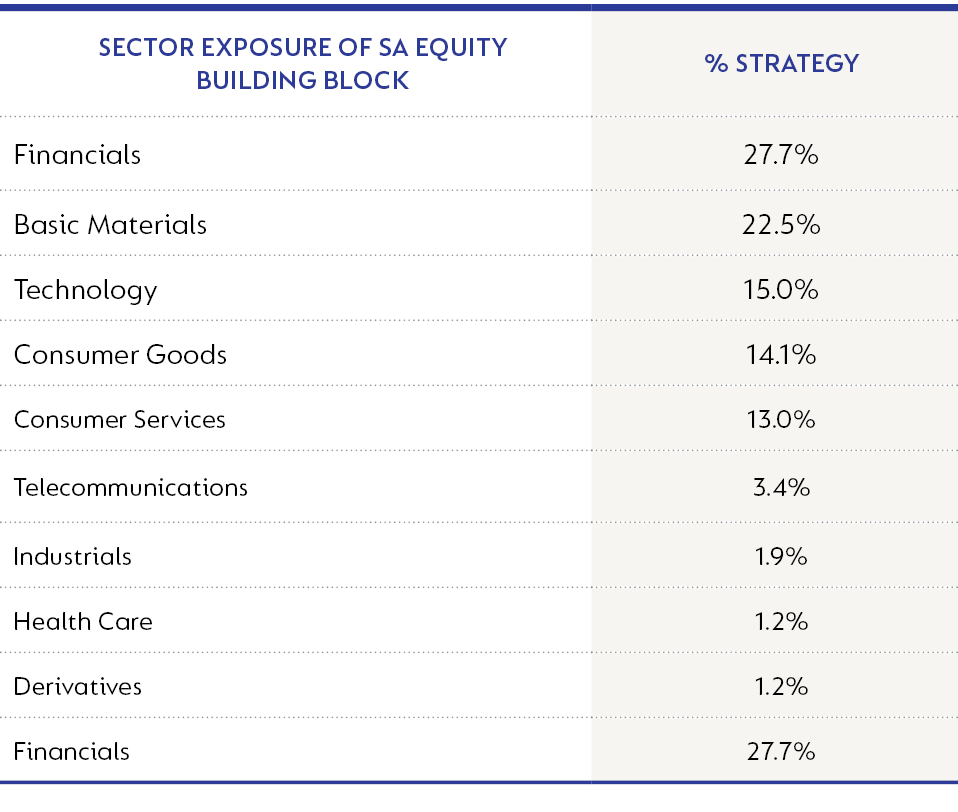

Our top 10 equity holdings and sector exposure as at 31 December 2022 are shown below:

While headwinds exist in both global and domestic markets, we believe equities are well priced for the risks and offer attractive returns to stock pickers.

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter