South Africa - Institutional

South Africa - Institutional

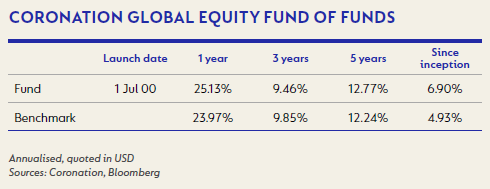

The fund advanced 5.1% against the benchmark return of 5.7%. This brings its one-year performance figure to 25.1%, compared to the MSCI All Country World Index (ACWI) return of 24.0%.

Japan was the best-performing region this quarter, rising 8.5% (in US dollar terms). The weakest return came from Europe, which rose 2.3% (in US dollar terms). The Pacific ex-Japan region returned 7.1% and North America rose 6.4%, while emerging markets advanced 7.1% (all in US dollar terms). The fund continues to be overweight North America, underweight Europe and Japan, and overweight emerging markets.

Amongst the global sectors, information technology (+8.1%), materials (+7.6%) and energy (+5.9%) generated the best returns. The worst-performing sectors were utilities (-1.0%), healthcare (+0.6%) and telecommunications (+0.9%). On a look-through basis, the fund benefited from its overweight positions in information technology and consumer discretionary and its underweight positions in utilities and telecommunications. Its underweight positions in energy and materials detracted from performance.

In general, the underlying managers had a weak quarter, although two of the fund's holdings (Lansdowne Developed Markets Strategy and Contrarius Global Equity) delivered very strong returns over the period.

Egerton Capital lagged the index over the quarter, but has otherwise had a very good year. Detractors from its performance include Ryanair (which declined 8% due to cancellations and pilot strikes) and Charter Communications (which also declined 8% after losing more customers than expected). The fund was further held back by its low exposure to resources.

Coronation Global Emerging Markets Equity had a difficult quarter, although its return for the one-year and longer-term periods remain very strong. Magnit, the Russian retailer, declined 33% after raising equity, while X5 Retail Group (a competitor to Magnit), declined 16%. Ctrip (Priceline, Expedia) fell 16%. The fund did have some good performers including Porsche, which rose 29% after the dismissal of long-outstanding lawsuits against the company, and Chinese insurers Ping An Insurance Group (+36%) and AIA Group (+16%), which benefited from a relaxation in regulations. However, these gains did not offset the detractors.

Maverick Capital and Tremblant Capital also closed the quarter behind the index. Maverick was again held back by its healthcare exposure after the industry recorded another poor earnings quarter. Tremblant, in turn, held UniCredit (-14%), The Tile Shop (-24%) and Telefónica Deutschland (-11%).

Contrarius and Lansdowne both generated strong alpha for the quarter. Contrarius benefited from its large weighting to energy and materials companies, while Lansdowne benefited from exposure to airlines and banking stocks.

Global growth is strong and a key consideration for 2018 is whether the pace of expansion would be curbed by inflationary pressures arising from such growth. A recent Bloomberg survey indicated that consensus was for little or no acceleration in global inflation. Monetary policy is expected to remain benign, with markets anticipating two to three rate hikes by the US Federal Reserve (Fed) in the medium term. The ECB has already guided that its quantitative easing programme will last until at least September 2018 and rates would be on hold until well past this date. The Bank of Japan, in turn, is not looking to change its relaxed monetary policy any time soon. It would be prudent to watch closely for any surprises on the upside that may modify these positions.

The last quarter of 2017 continued to bring good news and strong returns to equity investors worldwide. A combination of surprisingly strong economic data points (especially in regions such as Europe and China) and a relatively benign outlook on interest rate normalisation in the US fuelled equity markets to new highs. Investor euphoria grew even stronger when the US legislative forums agreed to a radical reform of the US tax system, one of the cornerstones of the Trump administration’s efforts to kick-start growth in the US economy. The headline corporate federal tax rate is proposed to drop from 35% to 21%, in return for the introduction of a territorial tax system. This will result in US-based multinational companies paying slightly more tax on their non-US earnings but seeing a drastic reduction in domestic tax rates. At the time of writing, much of the detail remains unclear, but it does not take away from the fact that this is a significant event that in the short term will lead to a jump in the earnings of the Standard & Poor’s (S&P) 500 Index of around 7% to 10%, and in the longer term could propel the US economy onto a higher growth path.

Global equity markets returned 5.7% over the past quarter, and a very strong 24.0% over 2017. The S&P 500 ended the year with a positive return in every month – a historic first. Inflationary pressures around the world continued to surprise on the downside and global central bank liquidity remained at close to peak levels throughout the year. This scenario culminated in very low volatility levels, with the cost of protection on equity markets continuing to reach new lows at the time of writing.

Emerging markets had a blowout year, producing 37.8%, with China registering the strongest performance among the grouping (+54.3%). Within developed markets, performances were closely aligned, with Europe and Japan marginally outperforming the US. This was primarily as a result of the weaker dollar, as the US performed better than most other markets in local currency terms. The dollar weakened by 14% against the euro over 2017. However, over the longer term, the US equity market has performed significantly better than any of the other developed equity markets.

While there was not much diversion among the performances of the various sectors, healthcare continued to lag, as did utilities and telecommunication services. Energy stocks benefited surprisingly little from a strong rebound in the oil price, resulting in energy (+6.9%) being the worst-performing subsector on the MSCI ACWI over 2017. Energy is probably the sector (outside of real estate) that stands to benefit the least from the tax reform. Information technology was the best-performing sector, with an annual return of 41.8%. Other notable laggards were telecommunications (+8.1%) and utilities (+14.1%).

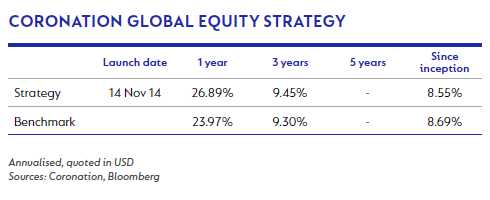

The strategy performed well against this backdrop. Its gross return of 26.9% for 2017 should be viewed against a very strong performance in 2016, which means that alpha for the two-year period now amounts to 4.3% per annum. Over three years and since inception, the strategy performed more or less in line with its benchmark, given the very challenging first year of the fund’s existence.

The biggest positive contributor this quarter was L Brands, a position that we have previously discussed in detail. It bounced back spectacularly from highly oversold levels, but subsequent to quarter-end sold-off in response to poorer than expected Christmas trading numbers. Other strong contributors over the quarter included Fox (on the back of a proposed takeover by Disney), Amazon, Spirit Airlines (a low-cost US airline introduced into the portfolio a few quarters ago), Naspers and Intu Properties (after announcing a merger with Hammerson).

By far the biggest detractor was Altice NV, a new position that was severely punished by the market for producing poor trading numbers (especially in its French operation), which led to concerns about Altice’s ability to service its reasonably high debt levels. Other disappointments included Allergan (loss of patents and an adverse court outcome), Newell Brands (poor trading update), and CVS Caremark and Walgreens (both punished due to fears that Amazon will enter the retail pharmacy market).

Over the last year, Fortress remained our biggest positive contributor, following its takeover by Softbank. Estácio and JD.com added significantly to performance, as did most of our other alternative asset managers (Apollo Global Management, KKR and the Carlyle Group). The strategy's internet positions (Amazon, Naspers and Facebook) benefited from the strong uplift in the sector. The biggest detractors over 2017 were Altice NV, Allergan and the retail pharmacy stocks Walgreens, CVS Caremark and Rite Aid. Put options to protect the fund from a significant drawdown cost the fund 28 basis points (bps) over the 12-month period.

The US tax reform signed into law is a game-changing event, and investors should expect the portfolio to change once the details of the programme have been fleshed out. During the last quarter our decision to increase the fund’s exposure to US cable stocks Comcast Cable Communications, Charter and even Altice NV was partly influenced by the fact that this sector will be a prime beneficiary of the proposed changes. The sector is almost exclusively focused on the US domestic market, provides for tax at the maximum rate, and is a significant investor in capital equipment, which will receive preferential tax deductions in terms of the current proposals. While the outcome of the tax reform initiative remained uncertain until just before Christmas, some of these stocks have reacted strongly before and after the bill has been passed. We will continue to assess investment opportunities with an open mind, but are also conscious of the fact that in a competitive environment like the US, there is a chance that at least some of the benefits of the tax reform will be competed away.

The strategy performed well over the quarter. For the year its gross return of 18.0% is very strong in absolute terms, and ahead of the benchmark return of 17.1%. The strategy has outperformed its quantitative benchmark over all meaningful periods, and since inception almost eight years ago, this outperformance amounts to an impressive 1.82% per annum.

It is gratifying to note that the strategy's equity carve-out beat the MSCI ACWI benchmark comfortably over one and three years, and marginally over five years. The property carve-out was particularly strong over one year, yielding a return of 24%. This subsector of the fund added significant value relative to the global bond index, which is being considered the alternative.

Our credit positions underperformed the global bond index over the last year, which was expected given our conservative positioning in this bucket. The merger arbitrage bucket detracted from performance after our Rite Aid position was negatively impacted by the renegotiated terms of the deal with Walgreens. The strategy's direct gold position contributed positively.

Probably the biggest detractor to performance was the decision just over a year ago to reduce the equity exposure in the fund to below the benchmark weight of 60%. We finished the year with an exposure of around 55%, and given how strong equity markets performed, the opportunity cost to the fund was material. We continue to manage the risk profile of potential returns, and therefore felt that it was the appropriate thing to do. We remain underweight equities in our positioning, as we believe that the current trading levels are discounting a lot of good news.

Please refer to the Global Equity Strategy commentary (above) the fund's equity performance.

With regard to the other asset classes, we remain concerned about the level of long-term interest rates, and as such remain negative about the outlook for global bonds. We also think credit markets are discounting a benign outcome in terms of corporate defaults, and have very low exposure to this asset class. Listed property still looks appealing to us in some of the geographies, and we will continue to selectively add to this sector over time.

The Coronation Global Emerging Markets Strategy returned 40.7% in 2017, which was 3.4% in excess of the benchmark’s return of 37.3%. In our view, longer time periods are a far more meaningful indicator of performance, and in this regard the strategy has outperformed the market by 4.8% per annum since inception nine-and-a-half years ago. Over seven years and five years, the strategy has outperformed the market by 4.0% per annum and by 2.6% per annum, respectively.

The largest positive contributors to alpha over 2017 were Naspers (+89.3%, a 2.6% contribution), 58.com (+155.2%, a 2.6% contribution), Estácio (+99.0%, a 1.6% contribution), JD.com (+63.2%, a 1.2% contribution) and Porsche (+55.8%, a 0.96% contribution). Other notable positive contributors (with a larger than 0.5% contribution) were Hering, Melco Resorts & Entertainment, Sberbank and Brilliance China. In terms of detractors, Magnit was the single largest detractor (with a -3.6% contribution), followed by Steinhoff (a -3.4% contribution) and not owning Tencent (a -2.7% contribution, although this was largely offset by Naspers's positive contribution). Smaller negative detractors included Samsung (a -1.3% impact from not owning the stock for most of the year), Tata Motors (a -1.2% contribution) and Alibaba (a -1.1% contribution, although this was partly offset by a 0.4% positive contribution from Altaba).

By country, the three largest positive contributors were China (with a +3.1% contribution which largely came from the Chinese internet stocks, but also from Brilliance China Automotive and Melco Resorts), Brazil (with a +3.0% contribution, mainly from the Brazilian education companies and the clothing retailer Hering) and Taiwan (a +1.4% contribution). The three largest negative contributors by country were Russia (with a -2.4% contribution, largely from Magnit), Korea (a -1.8% contribution) and India (a -1.5% contribution).

In terms of strategy activity over the past quarter, there were four new buys: Ping An (2.3% of strategy), Samsung Electronics preference shares (2.1% of strategy) and smaller new positions in Fomento Económico Mexicano (Femsa) (0.6%) and Reckitt Benckiser (0.5%). We also added to existing positions in Magnit, X5 Retail and Ctrip (all three of these as a result of weak share prices with little change in their long-term prospects, in our view, and the resultant increased upside to fair value), Yes Bank and Indiabulls Housing Finance (following a financials research trip to India in November).

In terms of positions sold, the strategy sold out of Melco Resorts, Norilsk Nickel and Discovery (all three had performed strongly and reached our estimation of their fair value), and also out of Anheuser Busch (better value was represented in other consumer staples like Heineken and British American Tobacco, which we added to, as well as the new Reckitt Benckiser buy). We also reduced the positions in Hering, Taiwan Semiconductor and YUM Brands (all three were getting closer to fair value due to share price appreciation) and also in Axis Bank (with better value represented in other selected Indian financials).

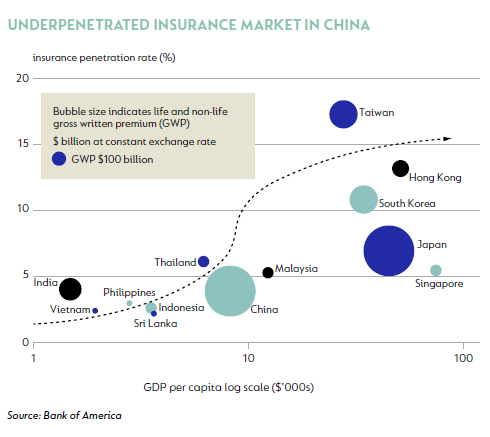

Ping An, the largest private insurance company in China, was the largest new purchase in the strategy over the quarter. The company has 153 million customers in China, and besides insurance products (life and non-life) it also offers asset management and banking services. The company is extremely entrepreneurial, with a founder chairman who is still very involved in the business and who owns a significant stake. Ping An’s value of new business has grown by 33.7% per annum over the past five years, net profit by 32.8% per annum and dividends per share by 35.1% per annum over the same period. China has one of the lowest penetrated insurance markets in the world, and Ping An has a number of competitive advantages – a high quality brand, a large and productive sales force (1.4 million agents with industry-leading productivity), and significant investment in technology and the resultant leadership in financial technology. It is also privately run compared to most competitors who are state owned. These advantages ensure that Ping An is well placed to take a high share of the growing Chinese insurance market over time.

While we have not owned Ping An before, we have followed it for many years and have owned AIA (the pan-Asian insurer and a key Ping An competitor in China) for the past few years, as well as Discovery (a joint venture partner to Ping An in China) until recently. Over time, these holdings have given us additional (positive) insight into the company. We have always held the view that the insurance assets of Ping An are very good and that the company is entrepreneurial and well run. In contrast, Ping An Bank (part of the Ping An Group) has historically been a concern to us, but over time, as the insurance business has grown at a high rate, the contribution from the bank has declined and is now only 17% of profits (from 35% of profits a few years ago) and a far smaller part of our fair value.

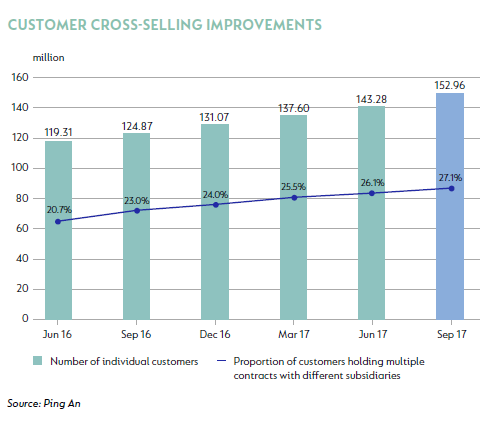

Besides an underpenetrated insurance market, in our view Ping An has the opportunity to continue to drive cross-selling through its large customer base. As can be seen from the graph below, over the past five years the cross-selling ratio (the percentage of customers who have more than one contract with the Ping An Group) has increased from 20.7% to 27.1%. The use of technology, together with a productive, well-paid and incentivised agency force should lead to further gains.

Ping An generates a return on embedded value north of 20% and today trades on around 14 times earnings (9 times embedded value earnings), with a 2% dividend yield. Given the long-term prospects for Ping An, we believe this is a very attractive valuation.

The strategy has not owned Samsung for a few years but in the last quarter bought a new 2% position in Samsung Electronics preference shares, which trade at a 20% discount to its ordinary shares. Over time we have become more positive about the long-term prospects for the semiconductor industry (which now makes up c. 65% of Samsung’s profits) as the industry has continued to consolidate and as additional revenue streams (such as ‘Big Data’ and artificial intelligence) have emerged. In recent months, two of the analysts in the Coronation Emerging Markets and Global Developed Markets teams have been researching two semiconductor companies (ASML in Europe and Applied Materials in the US), and this work has further contributed to a more positive long-term view of the industry. That said, the industry is cyclical and will continue to be so, and it is this cyclicality and concern over the industry’s profitability in 2018/2019 that have resulted in Samsung’s share price declining over recent months. In our view, semiconductor profitability is indeed above normal and this is very likely to result in earnings pressure in the year or two ahead.

However, the valuation of the Samsung preference shares in particular are very attractive (c. 5.5 times 2018 earnings with a 3.5% dividend yield), and given the more favourable long-term prospects for the industry we believe that this is an attractive entry point. Our two main concerns with Samsung over the past few years have been whether the high profitability of the semiconductor division could be sustained, and poor corporate governance, as indeed is the case with most South Korean companies. In this regard, besides the improvement in the long-term prospects for the semiconductor industry, there have in recent times also been corporate governance improvements at Samsung Electronics, including the effective separation of the chairman and CEO roles, and a change in the capital return policy, with a doubling of the dividend and a commitment to pay out 50% of free cash flow to shareholders between 2018 and 2020.

Femsa (0.6% of strategy) is a company that the strategy has owned in the past but has not owned for some time due to valuation. A recent decline in the share price, as well as the sharp depreciation of the Mexican peso, brought the share into buying range for a brief period. Femsa owns two great assets, which together make up over 70% of the value of the company – the Oxxo convenience stores and pharmacies in Mexico / the rest of Latin America (c. 50% of our valuation) and a stake in Heineken (c. 22% of our valuation). Its third major asset is a majority stake in Coca-Cola Femsa (c. 20% of our valuation) which is the largest Coke bottler in Latin American and the second largest Coke bottler in the world. In our view, this is a decent asset that generates significant cash but which faces some long-term challenges. Overall, given its mix of assets, Femsa is in our view a high-quality asset which owns very cash-generative assets and has shown strong capital allocation skills over long periods of time.

Reckitt Benckiser (0.5% of strategy) was the last small buy during the quarter. Reckitt is in our view one of the best-run global consumer companies and the owner of some of the best consumer health brands out there (including Durex, Nurofen, Strepsils, Clearasil and Gaviscon). Emerging markets contribute 41% of group earnings and are growing at a far higher rate than developed markets. In recent times, Reckitt has produced disappointing sales and earnings growth, which in turn resulted in a large decline in its share price. Whilst Reckitt undoubtedly faces some challenges, in our view the below average performance is temporary in nature and the share price decline enabled us to buy a stake in this high-quality business at an attractive price.

We continue to travel widely to meet with companies we own, or are interested in purchasing for the strategy, and trips to both Brazil and India are planned for the first few months of 2018. While emerging markets have appreciated strongly over the past year, we continue to find good selected value and the overall upside of the portfolio – our assessment of fair value versus current share prices – is around 40% on a weighted average basis.

The performance of markets across Africa continued to be strong over the past three months. The strategy’s gross return was 9.9% during the quarter, compared to its benchmark (3 Month USD Libor + 5%) which was up 1.6%, and the FTSE/JSE All Africa ex-SA 30 Index, which gained 3.3%. For the year, the fund delivered 36.9% compared to the All Africa ex-SA 30 Index, which returned 29.0%.

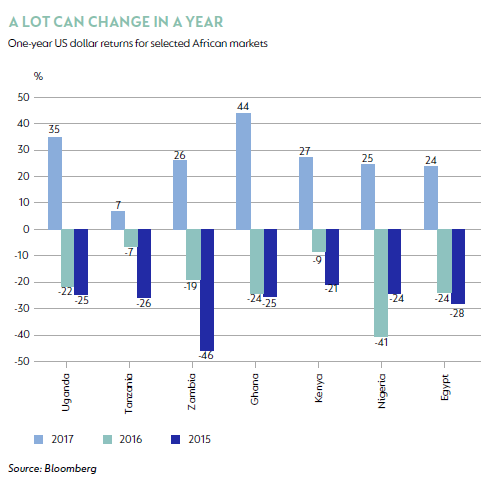

In 2017, many African markets rebounded strongly after two very painful years in 2015 and 2016 (see the graph below).

Nigeria gained 24.5% on the back of a number of positives which included the introduction of the Nigerian Autonomous Foreign Exchange (NAFEX) exchange rate window; the easing of forex liquidity pressure and normalisation of the parallel rate in response; and increased oil production and the opening of the Forcados terminal after its 16-month closure, combined with a more sustainable agreement with rebel forces. Similarly, Kenya (+27.5%), Egypt (+24.1%), Ghana (+44.0%) and Uganda (+35.0%) all gained.

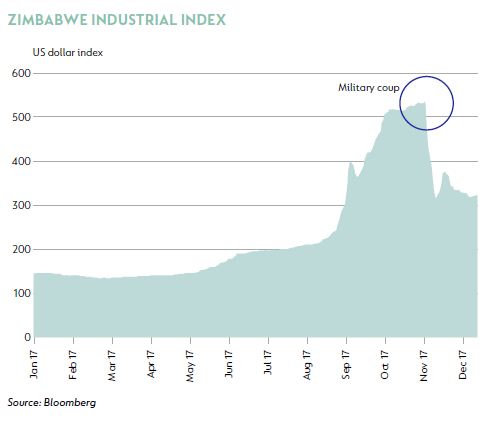

If there had to be a theme across African markets for 2017, it would probably be that ‘a lot can change in a year’. While Zimbabwe, Nigeria and to a lesser extent Kenya all bear testament to this, the real poster child must surely be Egypt. This time last year, Egypt was dealing with a year of foreign exchange shortages and economic pain that ultimately culminated in the November flotation of the Egyptian pound. The value of the pound plummeted, inflation skyrocketed and equity investors held their breaths.

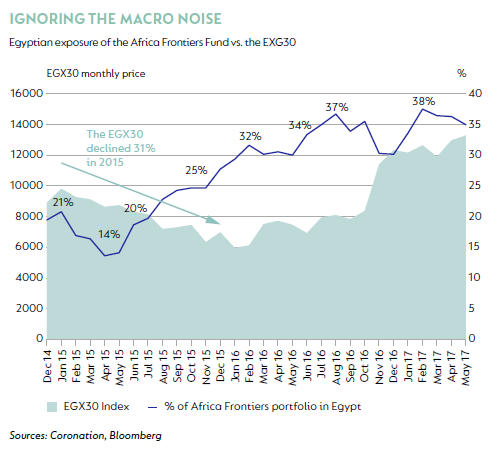

One year on, the country has seen $19 billion of inflows into government debt (as at October 2017) and c. $1 billion of net foreign purchases in the equity market. For the year, the dollar value of the equity market is up 24.1%, compared to a decline of 24.0% in 2016 (see the graph below). Local dollar migration into formal channels has been astounding, totalling an estimated $35 billion since the float, while another $15 billion was remitted from outside of Egypt in the first three quarters of 2017. In the corporate sector, Egyptian companies finally gained access to US dollars again – although at the cost of higher interest rates and inflation, which also resulted in consumers’ disposable income being squeezed. Encouragingly, businesses have adjusted well, with third-quarter results showing some green shoots as volumes recovered. While inflation (26% in November) and interest rates (c. 20% in December) remain elevated, we believe company earnings are on the path towards normalisation and valuations continue to look attractive.

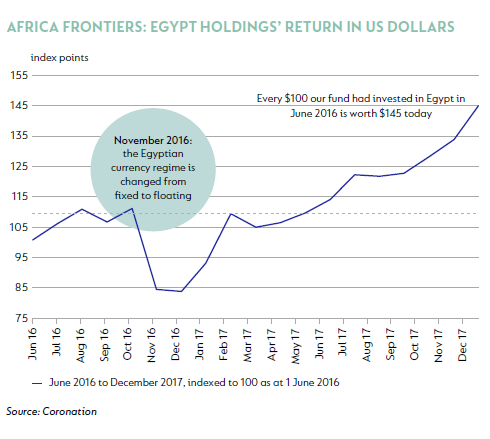

Our holdings in Egypt have performed very well for clients, in part due to the fact that we built large positions in high-conviction ideas that were trading at what we believed to be very attractive valuations and below-normal earnings when many other investors had written off the market. This required us to ignore the macroeconomic noise. In 2015, for example, the Egyptian market was down 30.9% while our fund’s exposure to Egyptian equities went from 20% to 28% and increased further to 34% by June 2016 (see the graph above). As at the end of December 2017, every $100 we had invested in Egypt in July 2016 was worth $145 (see the graph below).

Our holdings of Egyptian equities and bonds remain the largest geographic exposure in the fund as we continue to believe that companies are trading below their intrinsic value. In 2017, roughly half of the fund’s performance was contributed by our Egyptian holdings, which included Eastern Tobacco (Egypt’s monopoly tobacco manufacturer), EIPICO (an Egyptian pharmaceutical manufacturer that is a market leader in the export sector) and Commercial International Bank (Egypt’s largest private sector bank).

In light of our experience in Egypt and seeing first hand just how much can change in a year when the business environment improves for companies, we are particularly excited about our holdings in Zimbabwe. In the previous quarterly commentary, we wrote about the dire currency situation. Zimbabwe’s economic and political issues are well known. However, in the fourth quarter we saw the end of 37 years of dictatorial rule by Robert Mugabe. The rapid unwind of the stock market (see the graph below) since the military coup is proof of the return of confidence in some level of currency normalisation. Those who had been using equities as safe havens appear to be building up cash again in the hope of a return to currency liquidity.

We share our views on the Zimbabwean landscape elsewhere in this publication, but in short, we do not believe the economic damage done under Mugabe is irreversible. Zimbabwe is a deeply blessed country with unrivalled mineral and human resources. Allowing its people to get on with life unfettered and providing capital a degree of security will be transformational. Yes, forecasting the outcome and intention of the new roleplayers is tricky. We do know, however, that those vacating the throne had long outlived their usefulness. Being a long-serving dictator is increasingly a lonely and endangered pastime. This is a good thing for citizens and investors alike.

At Coronation, we have been patient investors in what we believe are very high-quality companies in Zimbabwe. We currently recognise our holdings in Zimbabwe at our internal fair value, but as share prices have given up some of the paper gains of recent months, if one were to look at current prices adjusted for the Old Mutual discount, our positions are worth quite a bit more.

A little over a year ago, our funds were heavily invested in three markets with delinquent currency exchanges: Egypt, Nigeria and Zimbabwe. The first two have since normalised and proved very profitable for our clients. For the patient investor, we believe that Zimbabwe will ultimately prove so too.

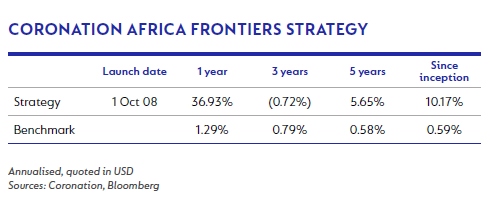

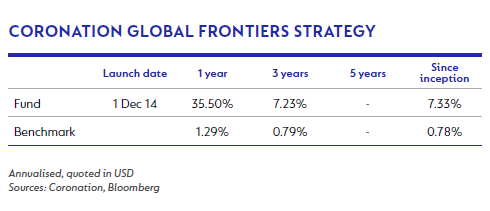

Over the past three months, the strategy delivered a gross return of 10.1% compared to the benchmark (3 Month USD Libor + 3.5%), which was up 1.3% and the MSCI Frontier Markets Index, up 5.6%. It was a strong quarter across the frontier universe, with Vietnam (+23.4%), Argentina (+15.3%), Egypt (+8.1%), Nigeria (+7.9%), Kenya (+5.5%), Bangladesh (+2.5%), Qatar (+2.5%) and Morocco (+2.1%) doing well. Kuwait (-4.1%), Pakistan (-2.0%) and Sri Lanka (-1.1%) lagged.

For 2017 as a whole, the frontier universe also saw some very strong market performance, with Vietnam (+59.5%), Argentina (+51.9%), Kenya (+27.5%), Egypt (+24.1%), Bangladesh (+18.4%), Morocco (+15.3%), and Kuwait (13.0%) all doing well. During the year, Pakistan was down 14.3% on the back of numerous factors, including the country’s upgrade into the MSCI Emerging Markets Index, the resignation of its prime minister following the ‘Panama Paper’ leaks, the removal of the central bank governor and chairman of the securities and exchange commission, the indictment of the finance minister and foreign investors becoming increasingly concerned about the possibility of a devaluation of the rupee. Qatar (-18.9%) and Oman (-11.7%) were down while Sri Lanka (-0.2%) and Saudi Arabia (+0.3%) closed the year flat. Over the year, the fund returned 35.5% compared to the MSCI Frontier Markets Index, which was up 31.9% and the benchmark (3 Month USD Libor + 3.5%), which was up 4.8%.

This quarter also saw the three-year anniversary of the fund. Over this period, the fund’s annualised return of 7.2% per annum outperformed both the benchmark return of 4.3% per annum and the MSCI Frontier Markets Index return of 5.0% per annum, placing it in the top third of frontier funds . While this is still early days, we are very pleased with the fund’s track record thus far.

We are a firm believer in running concentrated portfolios of high-conviction ideas. We believe that this is a key differentiator of the fund compared to many other ‘active’ funds that hold a significant number of stocks and often look more like an index than a portfolio. The impact of a concentrated portfolio is that a handful of stocks can have a significant impact on performance. 2017 bore testament to this. Over the year, the main contributors to the fund were two stocks, Eastern Tobacco and BRAC Bank, which contributed a combined 10.4% to the fund’s performance.

We continue to believe that the fund holds some incredibly exciting companies that trade at well below our estimate of their intrinsic value. We are also often able to find businesses that just do not exist in other, more developed, markets. We have highlighted two of these opportunities below.

- Al Eqbal Tobacco – Al Eqbal is the global market leader in shisha molasses sales, with an estimated 40% market share by volume and a 60% share of the profit pool. Al Eqbal is a dominant global multinational with a market capitalisation of only c. $1 billion. The company is best positioned to benefit from shisha increasing in popularity globally, and from an industry in the midst of formalising. The runway for growth is long.

- Grameenphone – Grameenphone is the mobile market leader in Bangladesh, with 53% share of industry revenue and the largest network coverage. Bangladesh has a population of 163 million people and is the densest among those countries with a population of more than 10 million. The number of towers or base stations needed to provide coverage to the country is relatively low. This results in the cost to service the population being very low and profitability per tower is thus incredibly high. It is this dynamic which allows Grameenphone to achieve very healthy and sustainable earnings before interest and tax margins despite Bangladesh having some of the lowest call rates globally.

We continue to remain focused on identifying companies in global frontier markets that trade below our estimate of their intrinsic value. By doing so, we believe that the fund will perform well and deliver attractive returns to our investors.

We monitor the performance of 26 frontier fund managers on a monthly basis; all data, sourced from Bloomberg, reflect managers’ gross returns and include dividends where they are paid/reinvested.

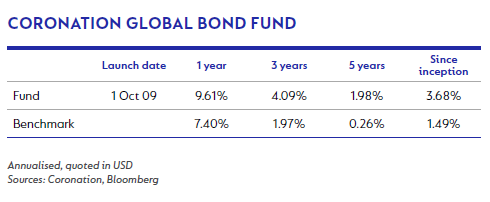

Core developed markets posted modest returns over the quarter as the upswing in global growth continued and inflationary pressures remained absent. Corporate bonds enjoyed another strong three-month period as risk appetite continued to be healthy. Support for emerging markets remained robust with the performance of outlying markets, for the most part, driven by political developments. Despite rising short-dated yields, the US dollar continued to languish. The fund returned 1.21% for the quarter and 9.61% for 2017, compared to returns of 1.08% and 7.4% respectively from the Bloomberg Barclays US Aggregate Bond Index.

Volatility within the US Treasury market remains very low, with 10-year yields having traded around 2.35% for most of the quarter and one-year realised volatility having fallen to its lowest level since the early 1980s. Meanwhile, the US yield curve has continued to flatten aggressively, with two-year yields rising 40 basis bps during the quarter, while 30-year yields fell 10 bps. The vast majority of the movement in rates during the quarter came through changes in real rates, given that breakeven rates were very stable throughout the period. The Fed raised the Fed funds rate by another 25 bps in December (the rate's upper band is now 1.5%), and its projections suggest a further three rate hikes in 2018. This is in contrast to the market, which currently prices only two rate hikes. Jay Powell, a Fed governor since 2012, is set to replace Janet Yellen as chairperson in February. While markets do not anticipate material policy changes, Powell’s apparent willingness to embrace the nitty-gritty of financial markets may prove valuable as the Fed continues to wind down its balance sheet.

When the Fed updated its Summary of Economic Projections in December, its GDP projection for 2018 rose from 2.1% to 2.5%. The subsequent minutes revealed this amendment captures some of the anticipated effect (seen at around 0.5% in 2018 and probably slightly less for 2019) from the tax reform package that was passed in December. Longer-term expectations for GDP growth were left unchanged and most economists are sceptical of the administration's claims that the reform will lead to a sustainable boost to growth. Given the already tight conditions in areas such as the labour market, it is more likely that the reform (which comes with a frontloaded bias) will merely magnify the cyclicality of the current cycle.

It may seem odd that the debt ceiling issue remains unresolved at the very time the US has passed $1.5 trillion worth of tax cuts (over a period of 10 years), 30% of which will be frontloaded over 2018 and 2019, boosting the fiscal deficit by just under 1% in these two years. A divided Congress had to agree on a long-term spending bill by 19 January to avoid another government shutdown, with the new tax bill potentially bringing forward the date (to mid-March) at which the US Treasury will exhaust its cash reserves. To add to the fiscal mix, the Trump administration, now emboldened by the passage of the tax bill, has said it will make infrastructure the next big legislative priority. However, delivering tax cuts to the already healthy consumers and private sectors of the economy will make it more difficult to fund any upgrades to the country's ageing public infrastructure that could improve the economy's competiveness and potential growth rate.

While we believe US Treasuries are less expensive than some developed markets, we still expect a gradual rise in US yields, in particular in maturities beyond five years where we believe the aggressive yield curve flattening (and lack of term premium) has gone too far.

During the quarter, the fund switched some of its exposure to ten-year maturities into five-year maturities.

Sentiment towards Europe has improved markedly and economic activity looks balanced and sustainable, with euro area GDP likely to be around the mid-2% level in 2018. Core inflation measures signal that some upward pressure is under way, and pressures on wage growth are also likely to become more prominent in 2018. For now though, the ECB’s commitment to ultra-low rates and continued quantitative easing remain extremely powerful drivers of yields. Markets expect the ECB’s deposit rate to remain negative until early 2019, guided by ECB president Mario Draghi’s comments that rates will not change until ‘well past’ the end of its asset purchase programme (current purchases will fall from €60 billion to €30 billion a month from January 2018), which is expected around the third quarter of 2018.

In the UK, Gilts performed well despite the Bank of England (BOE) reversing the 0.25% emergency rate cut in November that has been put in place following the Brexit referendum decision. The UK was deemed to have made ‘sufficient progress’ to begin phase two of Brexit negotiations. While that may seem encouraging, it merely brings one closer to the make-or-break decisions that need to ultimately take place. With inflation above target, it seems likely that the BOE will hike rates again during 2018. With long real yields in deeply negative territory, there seems little value given the uncertain backdrop.

The Emerging Markets Bond Index spread was little changed during the quarter, at 310 bps. Sentiment remains supportive, with the view that developed rates are unlikely to rise far enough to undermine the hunt for yield. Local currency debt should, for the most part, garner some support from benign inflation outlooks, amidst a softening in food prices. Debt metrics are arguably decelerating at a reduced pace, and in most cases at a no worse rate than in developed markets. The fund's hard currency emerging market exposure is biased towards shorter maturities. During the quarter, we increased the fund's exposure to these instruments through buying bonds issued by SA, Turkey and Qatar. The fund also increased its exposure to local currency SA government debt after a substantial sell-off in late October, but subsequently reduced its exposure following the ANC elective conference in late December, after which these bonds rallied significantly.

The outlook for corporate credit, meanwhile, looks more challenging after another very strong performance this past quarter. Credit spreads are now largely back to pre-financial crisis levels as corporate bonds outperformed government bonds by another 1% during the period. This takes their annual outperformance of government bonds to around 3.5% for 2017. Stronger economic growth and slightly more debt-friendly corporate behaviour do lend support to credit markets, but valuations arguably already reflect this, and in the absence of significant drawdowns, the market may be complacent. Despite large volumes of new issuance, inflows into the asset class have meant that credit availability has often been scarce, dissuading selling and dampening volatility. The challenge for credit markets in 2018 will be how they wean themselves off the support that has emanated from central banks' quantitative easing programmes. While national quantitative easing programmes are important, the cross-border effects are also material. In this regard, the reduction in the ECB’s programme is especially interesting, as low rates in Europe have resulted in investors selling European bonds to the ECB and buying assets overseas. These volumes are not immaterial, with net foreign buying of US spread products equal to half the net issuance of US investment grade issuance in 2017. Global buying from central banks during 2018 will be approximately $1 trillion less than in 2017. The fund added some exposure to MTN debt and bought a new tier one issue by Investec PLC, funded through selling existing, more senior exposure. The fund's Old Mutual debt holdings were tended for at attractive levels and we sold our exposure to Barclays and Absa. The fund has been very active in convertible bonds (Intu Properties, Impala Platinum, Remgro and Brait), which we believe are attractive.

Within foreign exchange markets, the continued US dollar weakness is noteworthy as it is at odds with the rising interest rate differentials, relative upside surprises in economic data and more recently the likely support that should flow from the US tax reforms. For now it seems the politics of a Trump administration are outweighing the fractious politics within Europe. As a result, the fund is once again using the euro as a funding currency for positions within emerging markets. The fund has exposure to Mexico, Turkey and SA. Domestic politics meant that all three countries' currency markets were volatile during the quarter, allowing the fund to take advantage of this by varying its exposure. In frontier markets the fund remains exposed to Egypt and Argentina.

The fund remains underweight duration, predominately via low duration positons in Europe and no exposure to Japanese bonds. We retain our preference for US bonds and the US dollar generally. The fund's exposure to mainstream credit is low (we see these areas as most vulnerable to lower quantitative easing), with our preference for higher yielding assets being expressed via short-term emerging market bonds and convertibles. We see value in some emerging markets, but less global liquidity will mean increasing headwinds. We continue to view low levels of volatility as the result of a lack of market conviction rather than a sign of healthy dynamics, and believe this argues for greater risk premiums going forward.

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter