Global (excl USA) - Institutional

Global (excl USA) - Institutional

Quarterly Publication - April 2017

POPULISM: FUELLED BY FEAR - April 2017

Brexit, the recent election of Donald Trump as US president and the upsurge in Eurosceptic parties over recent years are widely deemed indicative of a rise in ‘populism’. This umbrella term is hard to define: the representation of a populist political ‘left’ and the policies it is likely to implement will be different from a populist ‘right’. Another challenge is distinguishing between politics that may give rise to dangerous isolationist and divisive policies, and a more moderate representation of the interests of vulnerable groups. Using the term carelessly risks ignoring some of the nastier characteristics that have accompanied truly populist politics in the past. More often than not, political parties representing minority interests – the economically excluded or downtrodden, and a range of interests in-between – are labelled populist when this may not necessarily be the case.

WHAT IS POPULISM?

We have all read headlines in the past months about the politics of anger, but beneath the anger is always fear. Having established that there is no single definition of populism, and no common ideology that defines populist politics, it helps to distinguish between the ends of the spectrum and identify a number of common traits.

In today’s language, ‘leftist’ political populism would likely see lower- and middle-income voters stand against a wealthy, politically powerful and economically influential elite – movements akin to the labour movements of the past. ‘Rightist’ populism is more likely to see the same groups uniting against an elite accused of protecting or supporting outsiders – movements characterised by anti-immigrant, racially resentful politics. This is an ‘us and them’ kind of politics, which holds the politically influential elite to ransom for a range of grievances, with a particular focus on foreigners or minorities. In both cases, the people most likely to vote for a populist party or candidate tend to be economically vulnerable – those who are older, have experienced job losses or income stagnation, or feel they face a threat to their social or national identity, survival, livelihood or personal wellbeing.

There are other shared characteristics, aside from a broad division of the population into ‘the people’ and ‘the elites’. Populist movements tend to show fierce antagonism towards intellectuals (today’s ‘liberal elite’), favouring instinct over education. They champion polarising, divisive views and generally display contempt for the judiciary, and possibly also for the military and other political powers (such as government intelligence). Protectionist trade policies tend to feature, along with a willingness to implement capital controls and nationalise assets. There is usually also a strong intolerance of a free press.

POLITICS WITH A LIVELY PAST

Populist ‘uprisings’ are not uncommon – especially in the US. During the late 19th century, the farmers and labourers who constituted the People’s Party in the US (also known as the Populist Party, or simply The Populists) united against capitalist interests perceived to be driving inequality. The party called for the nationalisation of essential economic infrastructure – notably the railways – and was very critical of private banking.

Over time, the People’s Party joined other labour movements, and in 1896 endorsed a Democratic candidate, who swept to victory through the People’s Party’s constituencies. Having lost its independent identity with this endorsement, the party never really recovered. However, a number of US presidents who have followed have favoured ‘populist’ policies as part of their election platform – most recently (and visibly) President Trump.

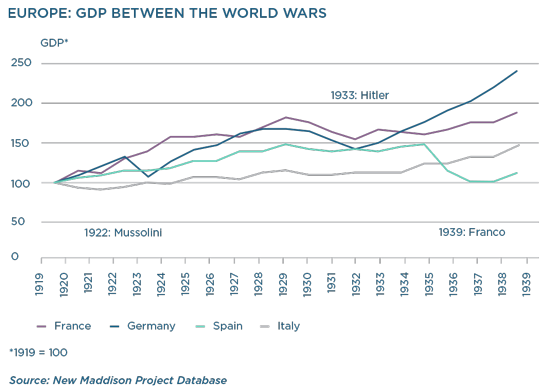

By the early 20th century, a new wave of populism emerged in Europe, which became more intense during the mid-war period, undoubtedly fuelled by the economics of post-World War I Europe, the Great Depression and the trade wars that coincided at the time. The political climate was characterised by nationalism in France and Francisco Franco’s Spain, fascism in Italy and Nazism in Germany, especially between the two world wars as ‘rightist’ populism fuelled the rise of the National Socialist German Workers’ Party under Adolf Hitler.

THE MODERN HISTORY

After World War II, populism faded with the careful, deliberate integration of social and political policies by Western governments of the time. In fact, the past 40 years or so have been an anomaly, with very little populist political activity globally (outside of Latin America) and almost no populist activity in developed economies.

Most notably, in the aftermath of World War II, the US, UK and European governments consciously implemented a strategy to ensure that economic development was strong and integrated enough to prevent such a war from ever happening again. For these countries, this meant that domestic policy initially focused on creating jobs and getting people employed. The success of this combined effort was the ‘golden era’ of growth in the 1950s and 1960s, when employment (primarily through union jobs in manufacturing) ensured rising wages, healthy gains in output and advancements in technology. But the economics were not all good: full employment led to rising wages, which fuelled inflation.

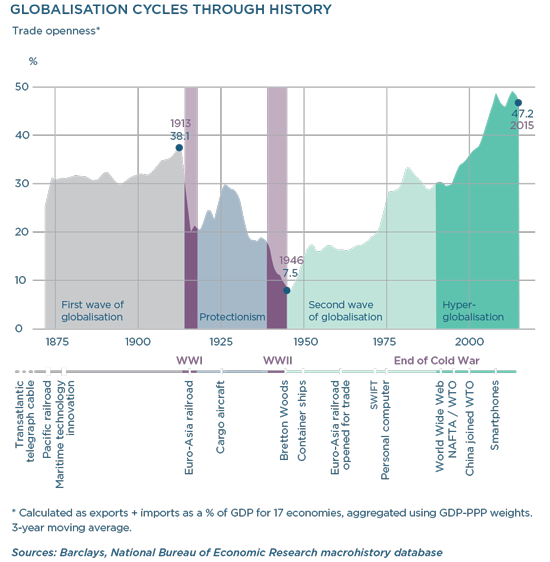

During this time, foreign policy – especially trade policy – actively promoted more open, integrated systems. Globalisation re-accelerated after the war, with the Bretton Woods agreement committing 44 countries to an integrated, gold-linked currency system that facilitated trade convertibility and established the US dollar as a reserve currency. The International Monetary Fund (IMF) and the World Bank were established in 1945; the IMF to monitor foreign exchange movements and facilitate reserve lending (trade), and the World Bank to aid war-torn countries’ rehabilitation. Technological advancement helped the world become more accessible, as container ships improved the speed and cost at which goods could be moved. In an effort to form the International Trade Organisation (the precursor of the World Trade Organisation), 23 nations signed a General Agreement on Tariffs and Trade in 1947.

These programmes were initially very successful. However, by the mid-1970s, high inflation led to somewhat of a revolt by the creditors within Western economies – the investors, banks and wealthier households. With the election of Margaret Thatcher as British prime minister in 1979 and Ronald Reagan as US president in 1980, there came a shift in economic policy focus – both leaders actively pursued policies to lower inflation and break trade unionism, benefiting the wealthy more than the indebted workers. (“Low-priced Asian manufacturers cost less. Unions are bad!”)

Since the late-1970s, economic policy in developed Western economies has been dominated by a move to inflation-fighting monetary policy, a prolonged trend of falling interest rates and the disintegration of trade union movements. Globalisation also picked up pace, with Asia opening to trade and a visible acceleration in trade agreements. Overall, the period was very good for ‘creditors’ but bad for households with debt, mostly in the middle classes. The process has also been reinforcing: as ‘creditors’ have benefited, their political preferences have been reflected in the elected leaders of most Western countries.

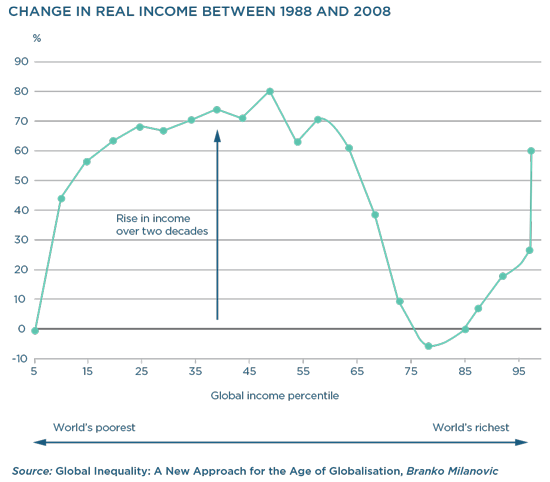

This has left many voters disenfranchised. A well-known study by economist Branko Milanovic introduced the so-called ‘Elephant Chart’, providing an insightful snapshot of the impact this process has had on global incomes. Between 1988 and 2008, the combination of lower inflation (and interest rates) and trade openness led to an increase in real incomes for almost everyone in the world … except the middle classes of the West. For these people – many of whom are male, middle-income earners and perhaps less educated in the post-war industrial era – income remained almost unchanged for 30 years.

The acceleration in credit growth from the early-2000s enabled these households to live beyond their stagnant means and to accumulate wealth as housing and other asset prices boomed. The market crash in 2009 – and in particular, the housing market collapse and spike in unemployment in the US and, to a lesser degree, the UK – was devastating. Despite the best efforts of economic policy, income was lost. So too were wealth and social identity, while fear crept in.

While covering the history behind the rise in modern populist politics across a broad spectrum, it bears remembering that the circumstances affecting individual countries differ. So too do the issues that are fuelling current voter unhappiness. In the US, Trump’s standpoint is somewhat of a mixture of populist policies, as he takes his cue from both the ‘leftist’ Rust Belt and ‘rightist’ anti-Mexican/anti-Chinese sentiment. In the UK, France and the Netherlands, lost wealth, stagnant incomes, immigration and the oppressive weight of governmental fiscal burdens – especially in the EU, where economic health differs so widely by country – are all aggravating factors.

In SA, the turning political tide bears worrying characteristics of other populist regimes, which are all increasingly visible: the antagonism towards intellectuals, xenophobia, challenges to a free press, interference with institutions and the judiciary, a rejection of conservative Western economic policies, demands to capture or nationalise private assets and an ‘us’ versus ‘them’ rhetoric.

WHAT IS NEXT?

History has not judged populist governments kindly – and with good reason. In many cases, populist policies were initially successful: growth accelerated and government spending fuelled investment. But excesses were hard to fund and reign in. Skyrocketing inflation and currency collapse have tended to be the catalysts for populist regimes’ downfalls, but the rehabilitation of fiscal and external accounts, and the rebuilding of institutions, take time – and come at great economic cost.

The experience of countries such as Chile in the 1970s and Peru in the 1980s is instructive. Both countries had experienced a period of economic hardship. The promise of radical economic change to an impoverished electorate saw the election of (two different kinds of) populist candidates in Salvador Allende in Chile and Alan García in Peru. Economic reform achieved under IMF programmes, limited as it was, created sufficient economic headroom for both leaders to implement highly expansionary economic agendas focused on the redistribution of income and the restructuring of the economy. In both cases, conservative policies were actively rejected. Among the economic justifications was a consensus that fiscal risk was exaggerated, or even unfounded. Although successful at first – employment and wages rose, inflation moderated and economic growth accelerated – bottlenecks ultimately emerged as domestic demand expanded rapidly, and import demand with it, putting pressure on reserves. Inflation, exchange controls and deteriorating fiscal balances led to shortages over time, and ultimately, to unstable politics and economic collapse.

SA may well be at risk of repeating some of these mistakes. Certainly, recent changes in key policymakers and the reiteration of the ruling party’s commitment to ‘radical economic transformation’ echoes the party mandates of Chile and Peru to a degree. How this commitment translates into policy changes and a new economic agenda remains to be seen, but any large-scale utilisation of state funds on unaffordable infrastructure may well precipitate an increasingly unsustainable fiscal (and external) position.

Globally, the biggest challenge for the world today is not the immediate economic impact of Brexit, or the future of the US under a Trump administration. Rather, it is the realisation that the neoliberal order that has dominated economic and political policy agendas over the past 70 years is at best under threat, and at worst breaking down. In some cases, policy reviews may not be a bad thing.

Countries with ageing populations (like the US and many European countries) need a pragmatic, agreed policy on immigration. In Europe, failure to agree on fiscal and banking integration has hamstrung the finely crafted union. In the UK, discontent over service delivery, economic stagnation and liberal immigration policies require all these issues to be re-examined. More broadly, the failure of economies to grow inclusively after the global financial crisis might necessitate a review of crisis-related legislation.

Importantly, the demands of populist electorates in the US, Brexiteers in the UK and Eurosceptics across Europe need to be considered and addressed by mainstream parties. The problem is that these parties may find it difficult to address the institutional and economic issues that have fuelled the rise in populism in the first place. Finding the right kind of jobs – with sufficient pay – in a world of integrated supply chains and disruptive technologies, while providing effective social support as populations age, sounds impossible. But failure to do so will further threaten moderate political legitimacy.

Arguably, Europe is in the most challenging position here. Both the US and UK have political and economic levers to pull, which Europe does not. It is easier for the US and the UK to replace their leadership within an election cycle, should economic outcomes disappoint. This may result in a more moderate (but still protectionist) nationalistic approach to domestic policies than we have seen. It will not fix the problem, but it could ultimately affect the process. In Europe, the reform process – in fact, almost any process – is hampered by unequal economies, and the disintermediation of politics and fiscal policy.

Unless there is an adequate response by moderate governments, macroeconomic performance improves and the fear that is fuelled by loss of income abates, the populists will continue to gain ground. While the initial response of markets and even economies may be positive, history suggests that poorly coordinated policies in a multipolar world are not good for growth, and may have severe unintended consequences.