Global (excl USA) - Institutional

Global (excl USA) - Institutional

Quarterly Publication - January 2017

CONSUMER STAPLES - January 2017

On the face of it, the international consumer staples sector appears to be a no-brainer for investors seeking global exposure.

These companies produce essential products (food, beverages, tobacco and household goods) that generally remain in demand even when times are bad. From Unilever, Nestlé and Anheuser-Busch InBev (ABI) to Heineken and British American Tobacco (BAT) – in our view, the sector has some of the best management teams, strong global brands, solid margins and defensive business models.

Intuitively, it feels less risky to invest in these global brand names, especially since consumer staples remain resilient in uncertain times – ideal for those seeking a secure offshore investment.

Still, we largely steered clear of these go-to companies in recent years. As always, our concern is valuation. While it would be easy to justify an investment in these upstanding companies, we only invest in shares that are trading below our estimation of their long-term intrinsic value. We do not invest in companies because we feel comfortable with them or can associate with their brands. We are solely focused on valuation; we do not want to overpay.

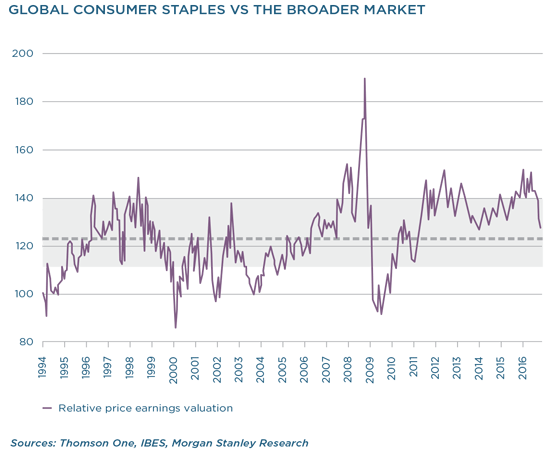

In recent years, consumer staple companies have rerated to trade at a much higher premium to the rest of the market than the historical average. They were in demand not only for their defensive qualities amid a weaker world economy, but also as alternatives to developed market government bonds.

Compared to the record-low returns offered by bonds, these respectable behemoths offered attractive dividend yields, low risk and the high probability of strong earnings growth. Return-hungry investors have been piling into these companies for many quarters, pushing share prices higher.

This trend promptly reversed following the US presidential election results. The market expects the Trump regime to pump money into infrastructure and, in combination with corporate tax cuts, bolster US economic growth. Along with this, inflationary pressures are anticipated, which triggered a sharp increase in long-term interest rates in the developed world. As bond proxies, the consumer staples were dumped in favour of perceived better value elsewhere.

With the prospect of a bump in growth, equity investors pivoted away from defensive workhorse investments to more exciting cyclical companies. Some of our current key holdings – including car companies and the mattress group Tempur Sealy – saw strong gains as investors recognised their value.

But without any change in their underlying prospects, consumer staples lost large chunks of their value. Almost overnight, for example, Unilever’s price earnings ratio went from 21 times to 18.5 with no change in the company’s outlook.

Now our interest was piqued.

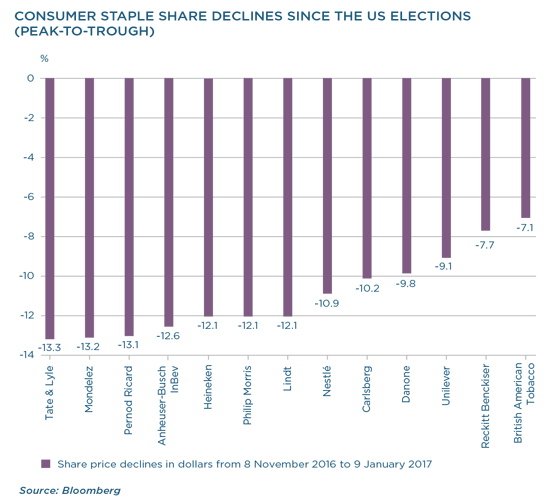

Some of the biggest names in the consumer staple sector suffered large losses since the presidential election, with Heineken and ABI both losing more than 12%. In relative terms, most consumer staples grew much cheaper. Compared to the broader market, the sector’s premium retreated by almost a third in the past 12 months, while its relative price earnings valuation reverted back to the long-term mean.

In our view, the sell-off in consumer staples was somewhat illogical. Nothing changed in the underlying fundamentals of these companies, and in fact, stronger economic growth will be a boon for consumer-facing corporates, particularly well-managed consumer staples.

We have moved quickly to benefit from what we deemeded to be the irrational in the sector. Over the last two months, we have increased our exposure to consumer staples in our Equity, Global Managed and Global Capital Plus portfolios.

We have added to the following holdings (in brackets, the weighting in the Coronation Global Equity Strategy portfolio):

BAT (1.7%) AND PHILIP MORRIS (1%)

In our view, long-term cash flow conversion across the tobacco industry is excellent, as working capital requirements are low and capital spend is constrained. We believe that the tobacco companies have demonstrated extraordinary pricing power and shareholder-friendly capital allocation. In our view, both groups continue to look attractive from a valuation perspective. New tobacco products – particularly the IQOS, Philip Morris’s non-burning cigarette which has found a large market in Asia – could provide a growth fillip in future. In addition to its promising new-generation products, BAT has sizeable activities in the US, which are likely to benefit from the anticipated lowering of corporate tax rates. It is also currently in negotiations to increase its US exposure with the proposed takeover and delisting of Reynolds American, the second largest cigarette seller in the US and owner of the Camel brand.

ABI (1.4%) AND HEINEKEN (1.2%)

The world’s largest brewers enjoy high barriers to entry, powerful brands (with the associated pricing power this affords), distribution muscle, access to cheap capital and top talent, and most importantly, a high level of free cashflow generation. ABI is currently digesting the SABMiller acquisition, which we believe will allow the group to reduce its cost base and improve margins.

UNILEVER (1.2%)

The British-Dutch multinational consumer goods company owns brands like Omo, Surf, Dove and Knorr. The company’s share price is down more than 9% (in dollars) since the US election, despite its aggressive margin and cash targets for the medium term. We are confident that the company’s adoption of a zero-based budgeting process will assist in achieving these goals.

RECKITT BENCKISER (1.2%)

The world’s leading consumer health and hygiene company (with brands including Dettol, Harpic, Durex and Nurofen) has strong pricing power and sells its products across 200 markets. In our view, Reckitt Benckiser has one of the most shareholder-friendly management team in the sector, with a proven ability to deliver operational results.

We have increased our collective exposure to this group of companies by 8% in the immediate aftermath of the US election. Also, we would not be surprised to see more weakness in the US bond market, which has the potential to create further opportunities in the largest consumer staples, given their correlated performance of late. As always, we will continue to be disciplined, valuation-based investors, and will only consider an investment that offers a sufficient margin of safety to our estimate of fair value.

This article is for informational purposes and should not be taken as a recommendation to purchase any individual securities. The companies mentioned herein are currently held in Coronation managed strategies, however, Coronation closely monitors its positions and may make changes to investment strategies at any time. If a company’s underlying fundamentals or valuation measures change, Coronation will re-evaluate its position and may sell part or all of its position. There is no guarantee that, should market conditions repeat, the abovementioned companies will perform in the same way in the future. There is no guarantee that the opinions expressed herein will be valid beyond the date of this presentation. There can be no assurance that a strategy will continue to hold the same position in companies described herein.