Global (excl USA) - Institutional

Global (excl USA) - Institutional

Economic views

Inflation hurts the poor most

“I don’t think it is an exaggeration to say history is largely a history of inflation, usually inflations engineered by governments for the gain of governments.” – Professor Friedrich von Hayek, economist, philosopher and Renaissance man.

The Quick Take

- The surge in global inflation has complex drivers, and, as yet, there is no end in sight

- Inflation does not impact everyone equally, the poor are always hardest hit

- South Africa has so far managed to avoid the sharp rise in inflation seen elsewhere, but this is no longer the case

- Higher policy rates, and a new target, are necessary to ensure inflation does not become unaffordably persistent

EVERYONE KNOWS WHAT inflation is – more or less. Certainly, inflation is very personal, it affects the prices we pay for our goods and services. It has a material impact on our ability to choose what we spend our money on and how much money we have to spend!

But we need to look beyond personal circumstance and even local economics to understand that the reach of inflation is much wider. There is an enormous body of academic research on the matter and much of modern history is permeated with the history of inflation. Inflation has been used by politicians and policymakers to control and manipulate sociopolitical outcomes, it has shaped politics, impacted societies, and had a material effect on the economics and politics of the poor. In 1974 Gerald Ford, America’s 38th president, famously declared inflation to be “Public Enemy Number One”.

BUT WHAT EXACTLY IS IT?

Consumer inflation is broadly defined as a generalised increase in prices formally measured by a surveyed basket of ‘goods and services’ consumed by an average household. The items within the basket are weighted by the proportion of income they consume, the biggest weights are usually rentals or shelter, utilities, transport costs and food items – all of which change very little over time. But the weight of these items varies meaningfully depending on the household income of the consumer. In a country like South Africa, poor households spend a large proportion of their incomes on staples like food and fuel (including transport), where demand is inelastic. When these prices increase, the squeeze on residual income can be devastating.

There are also different measures of inflation. Typically, ‘headline’ inflation measures the whole basket, weighted appropriately, while ‘core’ inflation excludes items where prices can be volatile (like food and fuel) as an indication of the persistence of underlying price pressures. Policymakers tend to watch core inflation measures more closely, but headline inflation is important too; not just because it is a real time indicator of changes in the cost of living, but because it influences price expectations, which drive long-term inflation outcomes.

IS INFLATION ALWAYS BAD?

No one likes inflation and almost any related quote casts it in a bad light. Former US President Ronald Reagan said, “Inflation is as violent as a mugger, as frightening as an armed robber and as deadly as a hit man!”. Perhaps more accurately, economist Kevin Brady said, “Inflation destroys savings, impedes planning and discourages investment. This means less productivity and a lower standard of living”.

But not all inflation is bad. Low levels of predictable inflation encourage spending, provide incentives, increase profitability, and support revenue growth. But long periods of high inflation, which is unpredictable, has negative socioeconomic consequences.

For consumers – whose spending can account for 60% to 70% of GDP – high inflation not only limits current spending, but it also undermines the ability to save and consume in the future. High inflation undermines investment, by lowering the pool of available savings and constraining investors’ ability to make a realistic assessment of the future return on that investment. Via higher interest rates, inflation raises the cost of borrowing, ultimately lowering the growth potential of the economy.

WHAT CAUSES INFLATION?

For something so well covered in academic literature, its causes are still well debated. Certainly, our ability to accurately predict inflation has proven poor. Milton Friedman famously said, “Inflation is always and everywhere a monetary phenomenon”, and long-lasting episodes of inflation have generally been accompanied by a long period of loose monetary policy. Put differently, when money supply grows persistently faster than economic output, purchasing power diminishes and prices rise. This ‘quantity theory of money’ is one of the oldest economic hypotheses.

But there are other short-term drivers that can also affect prices. Supply shocks, such as the oil crises of the 1970s and the Covid-19 pandemic, abruptly limit the supply of critical inputs (fuel, labour) and raise the prices of those specific items. These shocks tend to be temporary as demand either adjusts to the increased cost of the product, or supply improves. However, as we now see, prevailing economic conditions can affect how durable the price effects of a supply shock can be.

Similarly, demand shocks push up prices where underlying supply is unable to respond fast enough. These are often the result of expansionary policies. The Covid-19 response also visited a demand shock to inflation as massive income support collided with low policy rates, easing mobility restrictions and supply shortages of key consumer goods, such as cars. The result was a big boost to growth, and an even bigger boost to goods inflation.

Lastly, expectations play a key role in determining longer-term inflation. If companies and households (price and wage setters) anticipate higher inflation and embed these expectations into contract pricing and wage demands, these become part of future inflation, and are reinforcing. Expectations tend to be based on high-frequency purchases and are influenced by headline rather than core inflation. This makes expectations the link by which inflationary shocks become more durable.

INFLATION TODAY

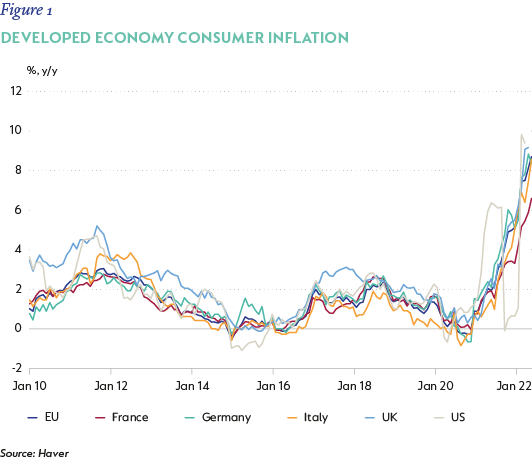

The rapid and now sustained rise in inflation across the globe that started in mid-2021 is the result of a confluence of factors (Figure 1). The first was the very strong recovery in global growth (the post-pandemic rebound in aggregate demand was much stronger than any post-crisis recovery seen in decades) and was well supported by both fiscal and monetary policies – which remained highly accommodative.

Secondly, demand for consumer goods has remained very strong, supported by savings accumulated during the crisis and the strong recovery in economic activity. The impact on prices has been aggravated by consecutive supply shocks (most recently intensified by the war in Ukraine and China’s rolling Covid-19 lockdown policies), which have seen commodity prices soar, and inhibited a more meaningful supply response to high prices and strong goods demand.

More recently, price pressures have also spread to services, with labour markets tight (vacancies now exceed the number of unemployed people in the US and UK) and a booming housing market (mostly in the US) pushing rental and owners’ equivalent rent price pressures up within the measured inflation basket.

This experience is a lesson that, while it is tempting to dismiss supply shocks as temporary, sector-specific shocks can spill over into other sectors and become more pervasive. And, despite a long period during which inflation expectations have remained low, expectations are not shatterproof, they notice changing common components around us. This leads to higher wages and entrenches higher inflation.

WHAT’S HAPPENING IN SOUTH AFRICA

Inflation in South Africa (SA) has been better contained than in many peer emerging markets, and some developed economies too (a first in many years). This in part reflects a less enthusiastic policy response from the central bank during the pandemic: while the South African Reserve Bank (SARB) slashed the repo rate by 300 basis points (bps) to 3.5%, it only actively intervened to provide additional liquidity temporarily early in the crisis when markets became dysfunctional. Despite much pressure to provide additional headroom and lower longer-term rates, the SARB resisted. As the recovery gained traction, it moved early to start normalising interest rates, with the first rate hike implemented in November 2021. Fiscal policy’s pandemic interventions provided some income relief, but were targeted at the very vulnerable, and not enough to materially boost aggregate demand.

Secondly, the economic recovery has been incremental, and weak. Not only was the KwaZulu-Natal/Gauteng unrest in 2021 a major disruption, but the arrival of the Omicron Covid variant conspired to keep growth in the services sector well below pre-pandemic levels, and unemployment high.

Lastly, the increase in global commodity prices resulted in a strong boost to domestic terms of trade and a surging current account surplus. This protected the currency and limited the pass through of higher global prices to domestic goods. Importantly, food inflation, which is driven by global prices and domestic supply and demand dynamics, remained reasonably well-contained.

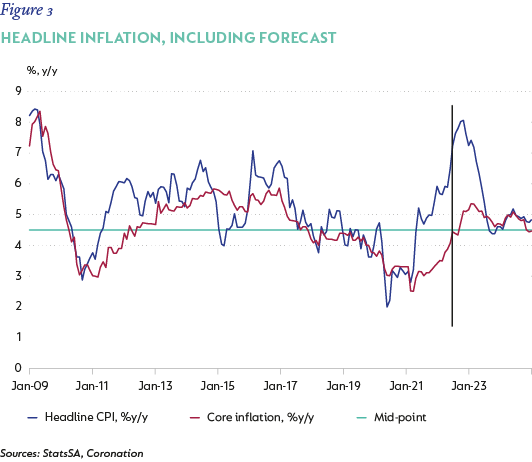

But SA is a small open economy, and not disconnected from the rest of the world. While these factors have helped contain domestic inflation, data for June was higher than expected. Headline CPI accelerated from 6.5% year on year (y/y) to 7.4% y/y, boosted by a 1.1% monthly gain. Of this, 0.2 percentage points (ppt) came from rising food prices, 0.6ppt from transport and 0.3ppt came from a more generalised rise in goods and services inflation. As a result, core inflation rose from 4.1% y/y to 4.4% y/y.

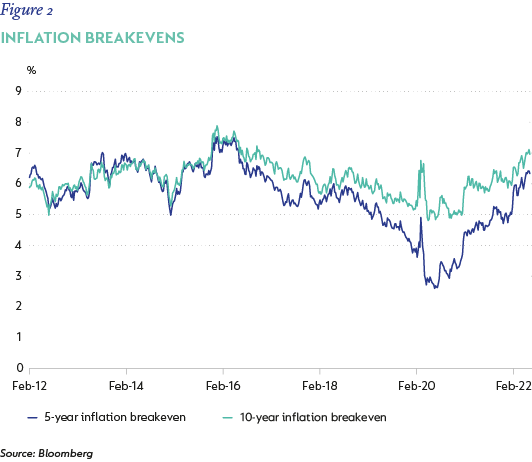

Surveyed inflation expectations have also risen. According to data released by the Bureau for Economic Research (BER) for the second quarter of 2022 (Q2-22), average inflation is seen at 6.0% in 2022, 5.6% in 2023 and 5.4% in 2024, considerably higher than the 5.1%, 5.0% and 5.0% respectively registered in the Q2-22 survey. Market-related expectations, as measured by the breakeven difference between nominal and inflation-linked bonds, have risen to 6.3% over five years and 7.3% over 10 years.

PRESSURES WIDENING – A GRAVE CONCERN

Looking ahead, there are sufficient reasons for concern that inflation is set to rise further from here. Not only are there coming fuel price adjustments as both persistently high international prices and a weaker currency are realised, but the suspended fuel levy will be reintroduced in August. Food prices are also going up. Food carries a 15.3% weight in the headline CPI basket and has a material influence on changes to headline CPI. While grains and cereals (which include bread and rice and items like pasta) aren’t the lion’s share of the food basket, their price drivers ultimately affect a substantial portion of the basket as they are inputs to the meat and dairy portion as livestock feed.

Global grain prices have been rising steadily for almost two years, reflecting the interplay between supply constraint (exacerbated by the war in Ukraine) and strong demand. Domestic supply has helped mitigate some of this pressure, but is not enough to offset it. Producer price inflation data show strong pipeline pressures have gained momentum and a hefty May consumer inflation food price surge shows these are being passed on. We expect food inflation to peak in the low teens towards the end of the year, before moderating slowly in 2023 and then reaching long-term average levels of between 5% and 6% into 2024.

Core goods prices are also starting to rise. The areas of pressure, for now, have relatively small weights, but vehicles, appliances and furnishings are seeing prices rise off a weak base, while clothing and footwear inflation is set to accelerate too. Again, producer inflation is signaling pipeline pressures are building here too.

With a heavy weight in the overall basket, this is a key contributor – along with elevated fuel prices – to the acceleration in inflation toward 8% y/y at the end of the third quarter of 2022 and into the fourth quarter, before a slow reversion towards the SARB’s target in 2024 (Figure 3).

The challenge for the central bank will be creating sufficient tension, such that expectations – measured by forward-looking market rates as well as surveyed expectations – do not see this rise as durable, and adjust long-term forecasts, which become reinforcing. Managing this will pivot on how strongly the central bank reacts to the increase in prices now, so that the public understands that inflation will return to target and price increases will not be accommodated.

WHAT CAN BE DONE?

The central bank has limited conventional tools at its disposal: the policy rate, which sets the level of short-term borrowing costs combined with its own ability to adequately communicate its commitment to the inflation target with a level of conviction that people believe.

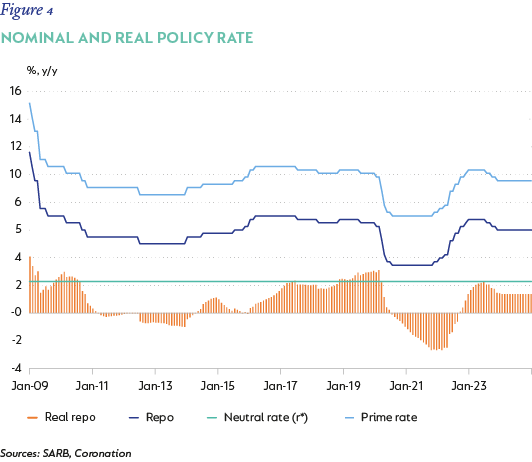

The Monetary Policy Committee (MPC) has already raised the repo rate by a cumulative 200bps off the pandemic-low of 3.5%, an early starter and an advantage to managing expectations. At the last meeting, recognising an increase in global and domestic inflation risk, the MPC voted to accelerate the pace of tightening to 75bps, signaling its willingness to more aggressively tighten in the face of deteriorating conditions.

A key part of setting monetary policy is the estimation of an inflation-adjusted (real) policy rate, which is consistent with a neutral state, where policy is neither stimulating activity, nor acting as a constraint. This neutral rate (r* in academic literature) is neither a peak nor a target rate, but more like a destination where policy is likely to normalise as the central bank fulfills its mandate.

The MPC’s current assessment of neutral is a real repo rate of 2.3%. There is much debate about what determines this, and whether this is the ‘correct’ level, but, directionally, this is significantly higher than the current rate. Using current inflation (measured as a 12-month average to date), the real repo rate is presently at -0.8%. On a forward-looking basis using an estimate for average CPI over the coming year this is -2.2%, which implies the current setting is still meaningfully accommodative in the face of rising inflation and deteriorating expectations. For interest rates to be strictly ‘neutral’ by the SARB’s assessment, the policy rate should be about 400bps higher.

While the MPC takes a wide range of factors into consideration when setting interest rates, to achieve the central bank’s mandate requires it to raise the policy rate towards a point of neutrality. The accelerated pace of policy tightening in May and July will move the repo rate into a positive real position in coming months, removing much of the recent accommodation. We expect the repo rate to rise towards 6.5%-7% (10.5% prime rate) early in 2023 (Figure 4), with some risk that interest rates move above these levels, should wage pressures arise and expectations remain elevated.

The need for an anchor

Another consideration may be the (timely) introduction of a new inflation target. The current target range has been in place since February 2000 and is high relative to SA’s peers and trading partners, which undermines competitiveness. The National Treasury, in consultation with the SARB, sets the target, and it is possible that a new, lower target will be announced in time. This may seem draconian when inflation and interest rates are already rising, but it is precisely when inflation is high and expectations are at risk, that a new anchor becomes a visible reminder of the central bank’s commitment to its mandate.

High inflation and rising policy rates are painful in an economy that has been struggling to grow for more than a decade. In addition, the impact is felt most by consumers, many of whom are already under pressure.

But the lessons of all previous periods of prolonged inflation show that persistently high inflation is felt most by the poor, for whom the cost-of-living impact is most severe and resources scarcer. This is not to say that the adjustment won’t be painful, but, while SA remains a low-growth, high-unemployment economy, we cannot afford the cost of high inflation.

Disclaimer

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter