Global (excl USA) - Institutional

Global (excl USA) - Institutional

Economic views

The rubber and the road

We can’t afford not doing better

- The outlook for SA is bleak, but firm action by the administration could soften the landing

- A clear plan to service inexorably rising debt is crucial

- National Treasury is the lead actor in how the Covid-19 drama plays out

- The possibility of zero to negative growth is a stark reality

SOUTH AFRICA'S FISCAL position is precarious. Finance Minister Tito Mboweni tabled a Special Appropriation Budget (SAB) on 24 June. This was necessary because the financial allocations associated with the Covid-19 pandemic response exceed the amount allowed by the Public Finance Management Act in a single fiscal year. The new baseline outlined in the SAB reflects the devastating economic and fiscal damage meted out by the Covid-19 pandemic on an already very weak economy. This is how things stand:

- GDP growth is expected to contract 7.2% in 2020 and recover by just 2.6% in 2021 (Coronation: -9.8% and 3.4%, respectively). This implies that the level of GDP will only return to 2019 figures by late-2023.

- The associated revenue loss is expected to be R300 billion, (6.1% of GDP; Coronation: R314 billion).

- Expenditure is expected to rise by R36 billion, adding to the redirected R100.9 billion, to complete a R145 billion support package for the economy.

- The main budget deficit is forecast at 14.6% of GDP from -6.8% in 2019/2020, and with a rise in debt service costs expected, the primary deficit is expected to widen from -2.7% of GDP to -9.7%.

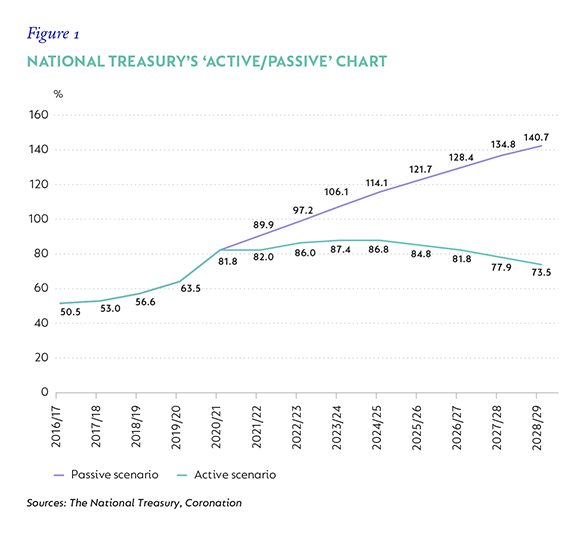

- Gross government debt will rise from 63.5% to 81.8% in a year.

The SAB presents alternative ‘active’ and ‘passive’ approaches to managing the longer-term impact of the crisis on government finances, especially on its debt burden. The ‘active’ approach requires R250 billion of expenditure consolidation and revenue adjustments over the next two years, to return the fiscal balance to neutral and help stabilise the debt profile, with a peak at 87.4% in the fiscal year 2023/2024. The ‘passive’ approach makes no meaningful adjustment and leads to an explosion in government debt.

The National Treasury reportedly secured ministerial support for the ‘active’ scenario before tabling the SAB, which means government has, de facto, committed to a painful consolidation of its spending, even if the full amount seems unrealistic. Despite massive efforts by the National Treasury to intervene in the most effective and sustainable manner, the weak starting position (low growth, poor policy execution, maladministration of State-owned enterprises [SOEs], and ongoing costly fiscal support of these entities) and the anticipated long-term impact on the fiscal position have made financial markets understandably more wary of its commitment.

But is it sustainable?

There is no single empirical or widely agreed upon definition of what constitutes fiscal sustainability, and there is no inviolable measure for the tipping point into crisis. But there are points of general agreement. The International Monetary Fund (IMF) defines a sustainable fiscal position as one which allows the government to meet its debt servicing obligations in the short, medium and long term without the need to make policy adjustments, which is implausible from an economic or political standpoint, without default or renegotiation given the financing costs and conditions it faces.

There are several important criteria implicit in this definition which need to be looked at more closely:

- Government needs to be able to service its debt, for which it needs to be solvent and have access to liquid financial markets.

- Servicing debt should not require a material change in behaviour – that means the government should not already have been running large deficits for a long period beforehand.

- The government’s economic and fiscal strategy needs to be credible.

Debt dynamics

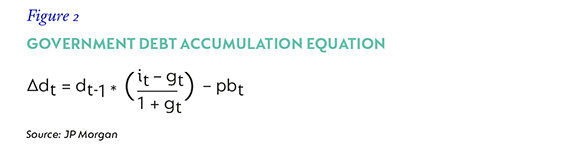

We have discussed debt accounting in a previous article, but it is worth highlighting again that debt dynamics are complex, and non-linear. The evolution of public debt is a function of three things: i) the existing stock of debt (a result of past policy decisions); ii) the interplay between growth and debt service costs (influenced by markets and past policy decisions) and iii) the primary balance (directly influenced by policy decisions) all captured in the simplified equation shown in Figure 2.

This equation highlights the complexities and interconnectedness of the dynamics that drive debt accumulation. For instance, for countries with a low stock of debt (dt-1), the primary balance plays a large role in debt dynamics, and government decisions to run surpluses can generally stabilise debt. For countries with a big existing stock of debt, the rate of growth relative to the cost of servicing debt has a bigger influence, potentially increasingly undermined by an unfavourable starting point. Managing this relationship doesn’t guarantee stabilisation without an improvement in the primary balance, but it helps buy time.

The dynamics of debt

This crisis is expected to profoundly impact government debt dynamics globally. In South Africa, the pandemic impact, which hit an economy already in recession, with rising debt service costs and weakening nominal growth, will add 18.3 percentage points of GDP to the stock of government debt this year. This puts us firmly in the latter camp, where growth and interest costs are most influential, but the primary balance also has to adjust to stabilise debt dynamics.

Before the crisis, South Africa had seen its debt stock grow from 26.5% in 2008/2009 to 63.5% last year. The IMF Debt Sustainability Analysis, published in January 2020, showed that most of this deterioration was because of the large deficits run from 2010/2011 to 2018/2019 – an average of 4.9% of GDP over the period. These persisted for a variety of reasons, including the growing public sector wage bill, ongoing support for SOEs and much weaker post-Global Financial Crisis growth. In parallel, government financing needs accelerated from 2% of GDP to 12% in 2018/2019, and an estimated 15.8% in 2020/21.

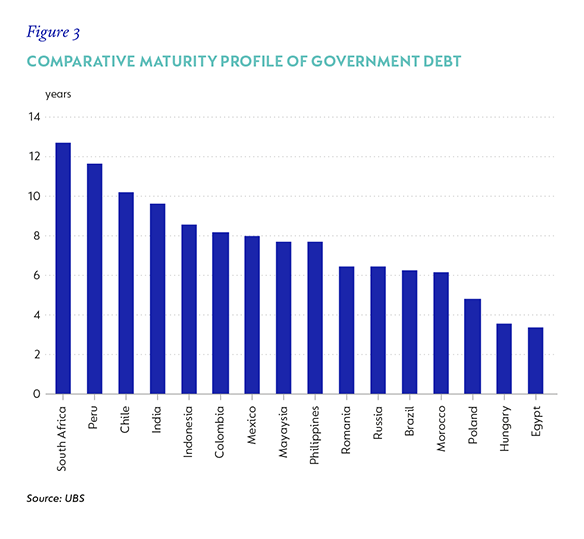

Mitigating factors include a very favourable maturity structure of outstanding debt. South Africa’s average term to maturity of its marketable debt is 12.8 years, which means it takes a long time for a change in market interest rates to materially impact the overall rate of interest government pays on its outstanding debt.

With these dynamics already at play in the accumulation of debt in South Africa, we are right to question the sustainability of government’s position going forward. We believe government will be able to reduce some of its expenditure in line with the SAB commitment, but that the planned 8% of expenditure over two years will simply not be politically possible. However, if much of the R101 billion reallocated in the current fiscal year is not back-tracked, government will be in a stronger starting position to limit spending in 2021/2022 and 2022/2023. Moreover, Finance Minister Mboweni has two powerful tools with which to impose some austerity – the reality that there simply is not additional revenue to spend (there is no money) and the real risk that ultimately South Africa may need additional financial assistance from an international organisation like the IMF, which will carry painful conditions. We think a saving of R110 billion to R120 billion is possible through a combination of permanent reallocation of some departmental, ministerial spending and grant saving, the withdrawal of specific Covid-19- related support, and perhaps a more aggressive stance on public sector wages under a new agreement from next year. We expect taxes to rise in line with the SAB directives.

A low bar

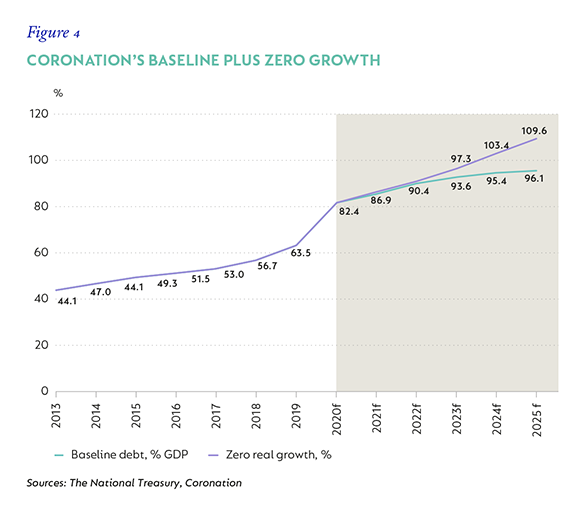

Under this baseline, we see the primary deficit narrowing from 10% of GDP in 2020/2021 to -3.2% in 2023/2024 and -1.1% in 2025/2026. While debt service costs are expected to rise only slowly given lower policy rates, changing funding strategies and the favourable debt structure, we think costs will rise. In addition, the persistently large deficits implied by the forecast will need to be funded. This year’s huge public sector borrowing requirement of almost 16% of GDP is being helped by international financing flows (the IMF and the World Bank) and a large increase in domestic issuance. Next year and the year after that will see smaller, but still-large financing needs without the support of these international flows. Local and foreign market participants will need to absorb this issuance and it is unclear to what degree they will be able to do so, and at what cost.

The alternatives are unattractive. The associated increase in debt would still see it approaching 100% of GDP over the next five years, albeit at a slowing pace.

Whether or not this inexorable rise is sustainable comes down to whether the market thinks government’s strategy is credible. This not only applies to its consolidation delivery, but its growth strategy too. Looking back at the IMF’s definition of sustainable debt, it highlights that the policies needed to stabilise debt should not be inconsistent with past behaviour and therefore does not require a massive leap of faith from the market to believe its intentions. Unfortunately, the government’s inability to reign in deficits over the past decade, either by stimulating much-needed growth or by cutting spending are discouraging, and the steepness of the South African yield curve is testament to this uncertainty. However, past performance is not always a perfect predictor of future outcomes. There are powerful incentives to deliver, and an even more desperate economic imperative to help stimulate growth. Failure to grow will see debt explode – and risk the loss of market access.

The time is now

Because debt sustainability in South Africa’s case is closely linked to its growth recovery, it could be argued that allowing fiscal accommodation to remain in place for longer would help build growth momentum and give the fiscus a firmer footing in the longer term. However, unlike emerging markets that have stronger starting positions and may have headroom and credibility to delay crisis-related consolidation in order to support growth, South Africa can no longer rely on unconditional support.

There are signposts to watch. A growth strategy, starting with the allocation of spectrum later this year and progress with energy sector transformation, which could both boost productivity, is essential. The Medium-Term Budget Policy Statement in October will give some indication of baseline spending allocations, (possibly excluding the wage agreement which may not have been concluded at the time). Any payments to SOEs outside of existing allocations will be indicative of government’s commitment – and political mettle. The February Budget in 2021 should provide a transparent framework by which government is measurable and accountable to markets going forward.

It is true that the post-Covid-19 world, especially for emerging markets, is going to be a precarious place and that relative performance will count. Markets will assess government nonetheless, and experience suggests that sovereign crises happen slowly at first, and then very fast. We cannot afford to waste the opportunity to do better.

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter