Global (excl USA) - Institutional

Global (excl USA) - Institutional

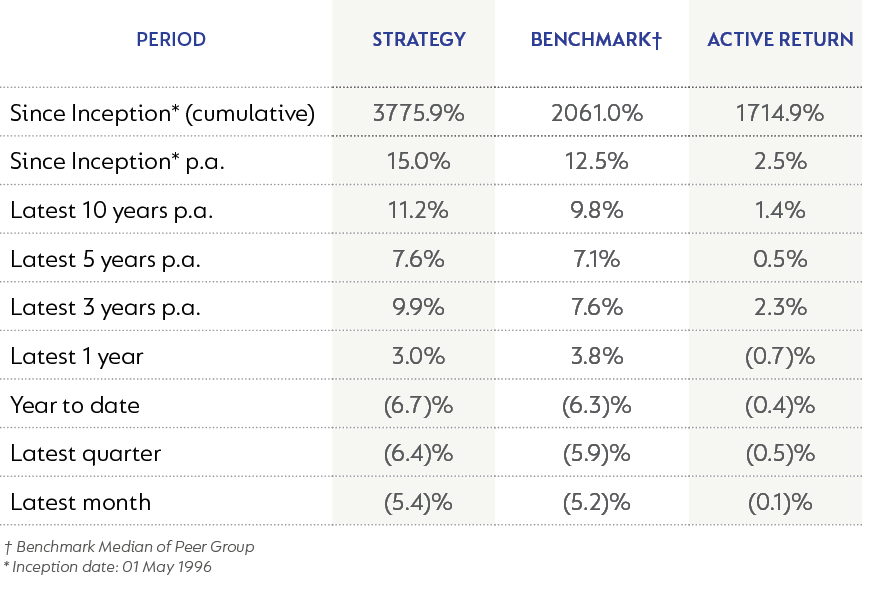

With local and global financial markets declining materially in the first half of this year, the Strategy has generated negative returns over this period; however, the twelve month returns remain positive. The Strategy continues to perform well against its benchmark over all meaningful time periods.

The second quarter of 2022 (Q2-22) continued the trend of extremely volatile markets, with a bearish bias. The JSE fell just over 10% but was a relative outperformer in global markets where the S&P 500 Index was down over 15% (in USD). The key driver of these negative moves was the rampant inflation across the globe and the expectation that interest rates will rise significantly from current levels in order to tame inflation. Markets appear unable to distinguish between good news and bad news, as every data point that arrives is accompanied by extreme moves, creating very unpleasant market conditions.

The Strategy’s performance as at 30 June 2022 is shown below:

While higher interest rates will clearly be negative for highly rated shares with long-dated payoff profiles, it is bullish for many financial companies that have suffered a decade of low to negative interest rates. However, the market has been indiscriminate in its sell-off, with very few shares or sectors delivering positive returns. The one sector that has been positive is the energy sector, where high oil and gas prices, partly due to the sanctions from the war in Ukraine, are driving strong profit growth. However, this has not been the case for other commodities, where we have seen a very brutal sell-off, even though the shares had never fully discounted high commodity prices before sell-off. The apparent fear of a slowdown, due to higher interest rates, has created a sharp sell-off, even though the companies are still generating strong cash flows at current commodity prices.

On top of the global negative sentiment, the local equity market is likely to suffer more pressure from the relaxation to Regulation 28, which sees the offshore allowance increased to 45%. Despite the evident value in the local market, we expect a number of local funds to externalise more assets, resulting in continued selling pressure locally until these flows have moved. We think this is not the right time to be doing this, as the relative valuation still strongly favours domestic assets, and as a result we are using the local weakness to build holdings at attractive valuations.

Local inflation, while outside of the South African Reserve Bank's (SARB) inflation targets, is nowhere near the extreme levels we are seeing in the historically low inflation regions of the developed world. This is due to the generally more restrictive monetary policy applied by the SARB compared to the rest of the world during the Covid lockdowns. As a result, we do not see an extreme rate tightening cycle in SA. Instead, we expect one more likely to be in line with our more recent past. This contrasts strongly with developed markets, where we expect interest rates to rise to levels not seen in well over a decade, and this will have an impact on their capital markets and economic growth.

Within our domestic equity allocation, we have added to our commodity exposure, given the unwarranted weakness we have seen in share prices as referred to above. After having sold down our platinum group metals (PGM) exposure last year, this has been the main area where we have added to in our strategy. The PGM basket price remains at levels where the companies will be generating significant free cash flows. Key now is for these flows to be returned to shareholders and not wasted on peak cycle M&A. This is a key focus of our engagements with these companies. We have sold out of the Strategy’s gold position, which worked as a defensive holding in inflationary times, and instead have put this to work in the (now much cheaper) equity markets.

Our large holding in Naspers/Prosus was the one bright light in this quarter, as their recent announcement to deal with the structural discount was taken positively by the market. This is our largest equity holding, which has had a torrid two years, so it was pleasing to see the strong recovery. We expect that once the discount closes, there should still be further upside from the potential recovery in Tencent as China emerges from its multi-year Covid lockdowns.

The past quarter also saw continued good earnings growth from our bank holdings. The economic recovery and higher interest rates helped them recover from the negative impact of the Covid lockdowns. All of these holdings should present earnings in the next month and the trading updates have indicated earnings are ahead of market expectations. Results should be accompanied by good dividends, helping to drive healthy underlying returns in a market where we are unlikely to see much capital appreciation.

We have increased our global equity exposure, the majority of this being from our put protection maturing deep in the money. This derivative protection, put on last year as global equity markets soared, has proven to be very valuable. Now that the developed markets have sold off, we think it is appropriate to allow our exposure to rise but funded from cash. The result of this is that our equity exposure is higher than it has been for some time, reflecting our expectation of where future returns will come from.

Even though global interest rates have started rising faster than previously expected, we still find most global debt instruments to be expensive. The real yields are still negative and not offering much value. Our position in SA government bonds has remained fairly steady. Credit has not repriced meaningfully and is also still not offering much value.

Property has suffered as interest rate expectations have started to rise, with global property particularly hard hit. However, given the value opportunity in equity, we have not made meaningful moves into this market.

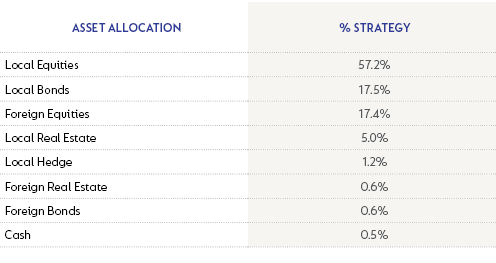

Our asset allocation as at 30 June 2022 is shown below:

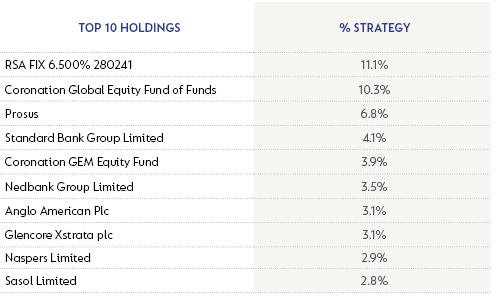

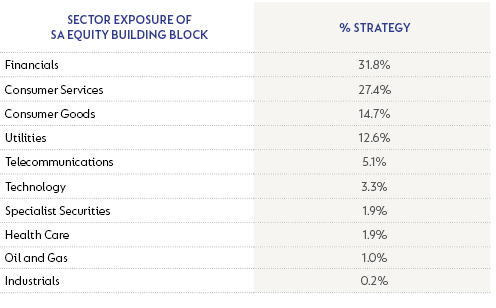

Our top 10 holdings and sector exposure as at 30 June 2022 is shown below:

In these capital markets, volatility appears to have become part of the normal course of business. We believe this is something investors will need to become accustomed to. Long-term returns are still excellent, and one needs to be cognisant of the need to stay invested for the long term in order to generate real, inflation-beating returns. We think valuations are currently very supportive of this objective.

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter