Global (excl USA) - Institutional

Global (excl USA) - Institutional

Investment views

Aspen Pharmacare Holdings

“The margin of safety is always dependent on the price paid. It will be large at one price, small at some higher price, nonexistent at some still higher price.” – Benjamin Graham, The Intelligent Investor

- To reap the benefits of a long-term view, the cost is often short-term discomfort

- Margin of safety is key when assessing the attractiveness of a share

- A high price earnings multiple can signal a death knell for a share should earnings expectations disappoint

- A focus on fundamentals is essential when investing in an unpredictable world

“The margin of safety is always dependent on the price paid. It will be large at one price, small at some higher price, nonexistent at some still higher price.” – Benjamin Graham, The Intelligent Investor

THE DEFINING ASPECT of Coronation’s investment philosophy is our long time horizon. We follow a common-sense, valuation-driven process through which we attempt to cut out the noise and buy undervalued stocks that offer a large margin of safety. Unfortunately, this usually coincides with periods when the share price is under pressure, either due to negative news flow or the share falling out of favour with investors. Our time horizon, which spans at least five years, often accepts short-term underperformance to deliver market–beating returns over meaningful periods. While this sounds simplistic, it is hard to implement in practice. Long-term investing requires patience and courage. One must be prepared to own shares that are out of favour and almost guaranteed to underperform in the short term. While this goes against one’s natural instinct, the results are rewarding over time.

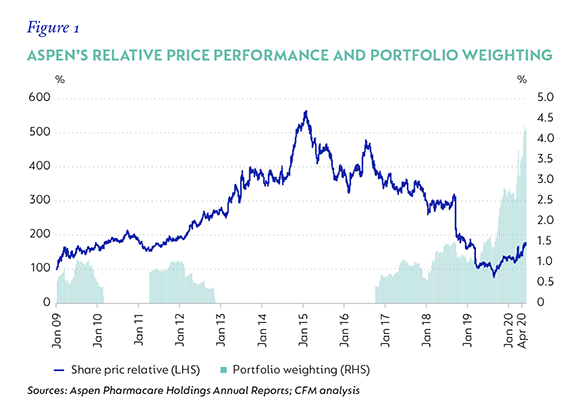

A good example demonstrating our investment philosophy is the history of our holding in Aspen Pharmacare Holdings (Aspen). We owned Aspen early on in its golden run as the business was transformed from SA Druggists into the leading South African generics company and then into a global specialist pharmaceutical company. From a base of R5, the share outperformed for more than a decade and peaked at R440 a share. Coronation sold early, missing much of the upside in later years. This is illustrated in Figure 1, which depicts the weighting of Aspen in Coronation’s Houseview Equity Strategy and its share price performance relative to the FTSE/JSE All Share Index over time.

Figure 1 shows that post Coronation exiting its holding in Aspen in October 2012, the share continued to outperform significantly, returning more than double that of the market between 2013 and mid-2015. Aspen’s share price peaked at R440, at which point it earned R12.19 per share to yield a price earnings multiple of 36 times. While the underlying fundamentals of the business remained unchanged, it continued to enjoy healthy returns and generate significant amounts of cash; this was more than discounted in its rating, with the share trading above our assessment of its fair value. In short, we believed the share price offered no margin of safety.

THE IMPACT OF GLOBALISATION

Aspen embarked in earnest on its globalisation strategy around 2009, when it concluded the first of three transformational deals with GlaxoSmithKline (GSK). Post-2009, it globalised at a rapid pace, concluding several large acquisitions with Pfizer, Merck, AstraZeneca and Nestlé. Today, the business is focused on three main therapeutic classes:

- Anticoagulants (blood thinners) – Aspen is the second-largest provider of injectable anticoagulants worldwide after Sanofi;

- Anaesthetics – Aspen has a 20% market share in anaesthetic products worldwide (ex-US); and

- High-potency and cytotoxic products, with a focus on oncology and female health.

These therapeutic classes have the following traits in common:

- They are niche and post-patent, which means that there is no pending earnings cliff. Once a patent expires, more affordable, generic products can compete and erode the profits enjoyed by the originator product. This also ensures predictability of future cash flows.

- Multinationals dispose of these products as they are regarded as non-core, which means that they are often neglected, resulting in product volumes declining over time. This presents Aspen with an opportunity to arrest the decline and eventually grow volumes. This can be achieved by placing more sales representatives behind these products and growing distribution in emerging markets where per-capita usage is lower.

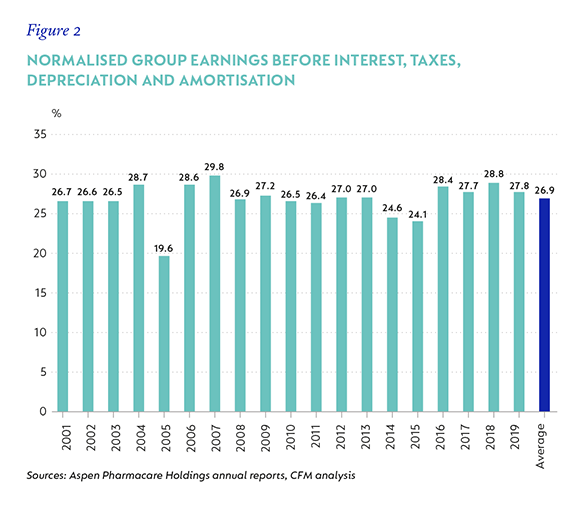

- The products are complex to manufacture, which negates the competitive threat from Asian players that prefer products with long production runs (such as antibiotics) where they can drive down the cost of goods. Manufacturing is the cornerstone of Aspen’s business model and it leverages its scale to reduce the cost of goods through better procurement and improved production efficiency. This is key to protecting gross margins – pharmaceutical companies are highly regulated and price increases are often controlled by government. Aspen’s excellence in manufacturing has resulted in its operating margins remaining relatively stable over time, despite pricing pressure (regulatory and competitive), as shown in Figure 2.

The transformation into a global pharmaceutical company was overseen by two of South Africa’s most entrepreneurial managers, Stephen Saad (CEO) and Gus Attridge (deputy CEO), who together own 16.5% of the company, aligning their interests with those of shareholders. Aspen’s track record of earnings delivery is impressive.

Figure 3 shows that the company has grown earnings at just over 21% per annum since its listing. Also apparent is the significant slowdown in earnings growth over the last three and five years. The combination of a high price earnings multiple and weak earnings growth resulted in the share de-rating relative to the market over the last five years.

Towards the end of 2018, the share price collapsed, eventually reaching a trough of R65 due to concerns about:

- A stretched balance sheet and the short tenor of debt borrowed to fund a series of company-transforming acquisitions.

- Although most of the recent acquisitions were successful, one of the largest (the purchase of anticoagulant products from GSK) has been disappointing.

- Organic earnings delivery in developed markets, especially Europe, has disappointed.

- The impact of African swine fever on the anticoagulants business which uses pig mucosa (in the production of heparin) as an input.

These issues have damaged the credibility of management and called into question Aspen’s business model of using debt to acquire post-patent products from multinationals and growing them in emerging markets.

After not owning Aspen for many years, we started buying in late 2016 and added to this holding as the share price continued to come under pressure as investor sentiment swung from euphoria to pessimism.

While the above concerns were real, and we believed they were adequately discounted by the market – at its low, Aspen’s price earnings rating collapsed to just below five times, providing a significant margin of safety. The share now offered an attractive risk-adjusted return for the long-term investor.

While the share has recovered from its lows, we think the market has underappreciated the significant strides management has made in addressing investor concerns:

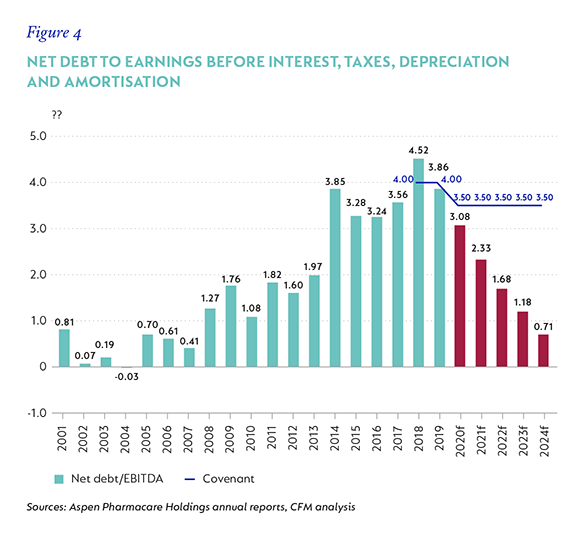

- Net debt levels have been significantly reduced following several large disposals. Aspen sold its infant milk nutritional business to French dairy group, Lactalis, for R11 billion. It also recently sold its Japanese operations to Sandoz for R5.2 billion. These disposals reduced Aspen’s net borrowings from a peak of R53.5 billion to just over R33 billion as at 31 December 2019, thereby creating some covenant headroom. Furthermore, cash-flow generation in its most recent results was very strong as management focused on reducing the investment in working capital. Aspen’s capital expenditure cycle reduces significantly from 2020, which should allow debt to be paid down faster. The reduction in net debt levels removes the risk of Aspen needing to raise equity to bolster its balance sheet. This is depicted in Figure 4.

- Management has a stated target of reducing the net debt to earnings before interest, taxes, depreciation and amortisation ratio to close to two times. They believe that this will allow for sufficient financial flexibility to allow Aspen to capitalise on acquisitive opportunities. We believe this is achievable given the focus to unlock the investment in working capital and the reduction in future capital expenditure requirements.

- Aspen has built up a significant buffer in heparin stock and has nearly two years of supply. This is due to it being vertically integrated into the manufacture of its anti-coagulant products. The buffer stock protects it from short-term spikes in heparin prices caused by African swine fever and reduces the risk of stock-outs. This should allow it to either supply competitors, capitalise on high heparin prices, or gain market share in the event of competitors being unable to meet demand.

- There are plans to address the weak performance from its anticoagulants division by introducing a strategic partner into its developed European business. This will result in an initial cash injection (once a portion of this business is sold) and should result in better volume performance as the strategic partner assists in placing more sales representation behind these products.

Furthermore, emerging markets currently contribute 46% of the revenue generated by anticoagulants. Per capita anticoagulant usage is lower in emerging markets, which should support future volume growth as the contribution of emerging markets to sales increases.

- Demand for Aspen’s sterile portfolio of anti-coagulants and anaesthetics has increased due to the Covid-19 pandemic:

- Blood clots are treated by administering anticoagulants, and there is increasing evidence that Covid-19 leads to blood clots in patients that may result in pulmonary embolism.

- Anaesthetics, especially muscle relaxants, are administered to patients who require ventilation. This should support volume growth for the foreseeable future until such time that a vaccine is developed.

At the time of writing, the Aspen share price has recovered to R150, after reaching a trough of R65. It has outperformed the market by a factor of two from this low.

Despite some recovery, Aspen trades on an attractive one-year forward price earnings multiple of 9.3 times and just under nine times our assessment of normal earnings, and remains a 4.2% holding in our clients’ portfolios.

Recent news flow has also been supportive – an injectable steroid, dexamethasone, has proven to reduce Covid-19 deaths by a third in patients on ventilators and has also shown to reduce fatalities by a fifth among patients who were receiving oxygen support. Aspen is a major manufacturer of dexamethasone injections in South Africa as well as other markets such as the UK. We had no special insights into these extraordinary developments, and we simply owned Aspen as we believed that the risk-adjusted returns and resultant margin of safety were attractive.

In today’s volatile financial markets where asset prices are determined by the news of the day, it’s easy to miss the wood for the trees. Patience, courage and a long time horizon are required to make rational, long-term decisions. In a world where time horizons are collapsing, we remain committed to our proven philosophy of investing for the long term. +

Disclaimer

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter