Global (excl USA) - Institutional

Global (excl USA) - Institutional

Investment views

China - a weighty issue?

A weighty issue?

- Unprecedented growth has boosted China from a stagnant economy to a global heavyweight

- China’s dominance of the MSCI Emerging Markets Index is set to strengthen in the near future

- An index that is so dominated by one country poses a problem for passive investors

- Active management is required to price the risks associated with the degree of Chinese state-owned stocks in the Emerging Markets Index

MUCH TIME AND effort have been devoted to understanding the recent rise of China as a major global economic power. It is, however, important to also note that China (or at least the precursor territories making up modern China) was the largest single economy in the world until the late 1800s and had been so for several hundred years. This isn’t surprising, as people have lived a subsistence or agrarian existence with fairly low output per capita for most of human history. Countries with larger populations would therefore have had larger economies. This changed permanently with the advent of the industrial revolution and the advancement of technology, in particular. First the Western European nations, then a rapidly growing US, came to dominate the world economy thanks to massive gains in technology-enabled productivity.

China underwent substantial transformation during this period. Military defeats to Britain in the Opium Wars (which led to the ceding of Hong Kong to Britain) were followed by partial colonial occupation by Japan, a civil war leading to communist control of ‘mainland’ China and the fleeing of the nationalist government to the island of Taiwan in the aftermath of World War II. Following this period, communist mainland China stagnated economically until around 1980. At that point, China accounted for less than 5% of world GDP (despite the country making up 22% of the world population at the time) and the average person was extremely poor relative to someone living in the West (per capita GDP was a mere 1.5% of the average American). Unprecedented sustained economic growth has since transformed China into a middle-income country and, because of its large population, it is today the second largest economy in the world; the largest if you use purchasing power parity.

EMERGING GLOBAL FORCE

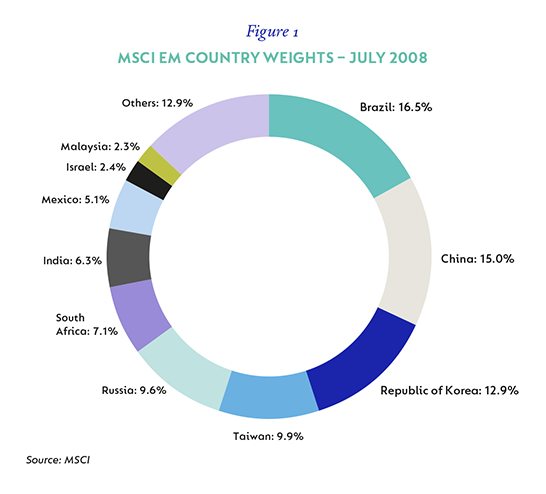

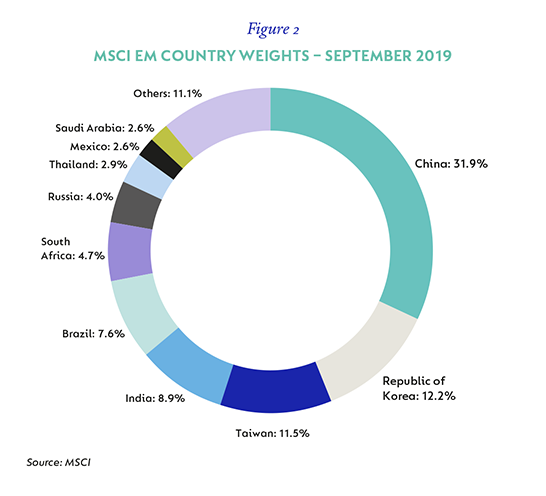

Where China was once just another emerging market (EM) at the turn of the century, today it is the most important EM (see Figures 1 and 2), and one that can make or break the returns of any fund manager. In the run up to the Global Financial Crisis, when commodity prices were still elevated and the currencies of commodity exporters were trading at historical (relative) highs, Brazil was the largest weight in the MSCI Emerging Markets Index at 17%. China’s weight had risen to 15% by this point, from single digits several years before. Fast forward to the time of writing, and China’s weight has reached almost 32%, while Brazil’s has declined to just under 8%. Such has been the scale of China’s growth that the next largest country weight in the index is almost 20% behind it (Republic of Korea).

If all index securities moved in tandem going forward, China’s weight would increase further in the months and years ahead. Currently, the A shares (domestic China listings) have an ‘inclusion factor’ of 15%, meaning that 85% of their weight is not counted within the MSCI Emerging Markets Index. They started the year at 5% and by the end of 2019, the inclusion factor will increase to 20%. All else being equal, this will increase China’s overall weight to 33%. As the inclusion factor edges up further, it could, if it reached 100%, eventually result in China being over 42% of the broader index. An index so dominated by an individual country is problematic for passive or tracking error-conscious investors, but it is a material opportunity for active managers to add (or destroy) value.

EMERGING MARKET OUTLIER

China is in many ways very different from the rest of the emerging market universe. As a start, it is the only country in the index with a weight above 5% where a very large proportion of the listed market consists of state-owned entities. Russia is another country with high levels of state ownership of large index constituents, but is only 4% of the market.

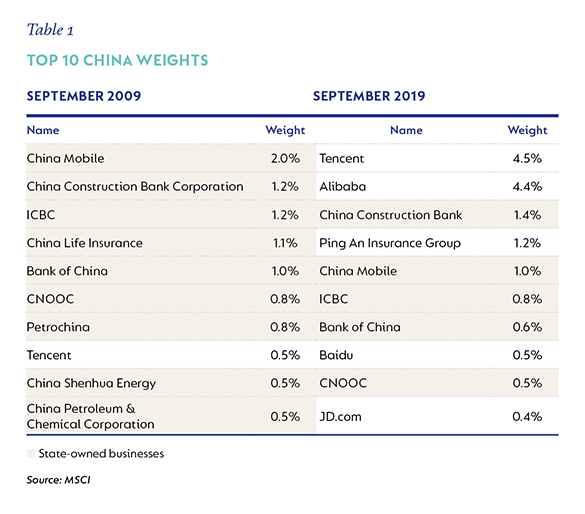

State ownership is rarely positive for minority shareholders in the long run, as the state has often shown itself to be a poor custodian of capital and has other obligations to meet besides maximising shareholder returns. Over time, a high level of exposure to state-owned businesses could likely result in poor absolute returns. A very good illustration of this is shown in Table 1, where the top 10 Chinese stocks in the MSCI Emerging Markets Index are shown at the end of the most recent month and the corresponding month 10 years ago. State-owned businesses are highlighted for ease of reference.

As one can see in Table 1, state-owned businesses have underperformed their private sector peers by a significant margin over the last 10 years, such that five new private businesses have entered the top 10 weights (displacing state-owned businesses), and the only top 10 private sector business from 10 years ago (Tencent) is now the largest stock in the Emerging Markets Index. A passive investor in emerging markets today (like before) has significant exposure to the Chinese state via the state-owned businesses that comprise the index. Additionally, many of the private sector stocks in China face risks and regulations that are unique to China. A good example is the existence of variable interest entity structures. These allow companies in China to list overseas despite their core operations being officially closed to foreign investors. All the main internet stocks (Tencent, Alibaba, Baidu and others) use these structures. We don’t believe it is likely that China would end this practice due to the impact it would have on its capital markets, but the risk is non-zero in nature and does not exist in other countries. China-specific regulation also impacts many other businesses, from censored search results in Baidu to foreign content restrictions in the gaming companies. The high concentration to China should play a precautionary role in both the asset allocation decision on exposure to emerging markets and the decision on whether to invest passively or actively. In our view, the very high China concentration, coupled with state ownership and regulation, materially increases the risks associated with investing passively in emerging markets.

Only an active approach can price for and navigate around these risks. There are many great businesses in China that investors should have access to at the right price and, in our view, their presence in an investor’s portfolio should be valuation dependent, not determined by index weight. This observation is true for all countries, but with China’s high index weight, it is particularly relevant.

Disclaimer:

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter