Global (excl USA) - Institutional

Global (excl USA) - Institutional

Investment views

Yield curves

Inverted yield curves, negative bond yields, liquidity everywhere and not a drop to drink

- An inverted US 10-year Treasury yield curve can not only be a predictor, but a cause

- The post-GFC central bank monetary arsenal may well prove ineffective in current conditions

- Times are unprecedented; more than 25% of the global bond market now trades at a negative yield

- It’s not insane to invest in negative-yielding bonds; in current conditions it would be a pity if SA missed the bus

SMALL FORESTS HAVE been razed to the ground and squids worldwide have been sucked dry to help support the volumes that have been written about bond yield curve inversions in recent times. This reached a peak at the beginning of September, when the US 10-year Treasury bond yield briefly fell below that of its short-dated counterpart, the two-year bond, for the first time since 2006. The ensuing frenzy of handwringing and woeful prognostications from market commentators has certainly been eyebrow raising. Yet are they wrong?

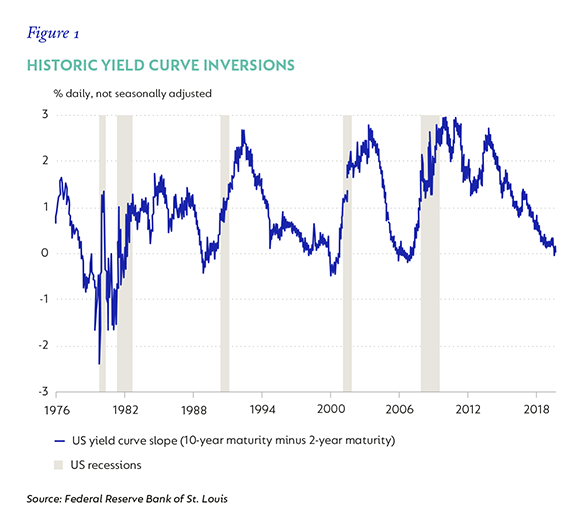

There are respectable justifications for taking heed when long-term interest rates in the US fall below the level of short-term rates. This is a rare occurrence and has been – without contest – the most reliable early warning signal of an impending recession. Out of the 10 instances that the curve has inverted since World War II, only once (in the mid-1960s) did the slope of the curve turn negative without an ensuing recession; conversely, there haven’t been any modern US recessions that weren’t preceded by an inverted yield curve (see Figure 1).

THE ORACLE

But it’s not just the success of this indicator that’s attractive to market watchers; it’s the extent of the forewarning the signal provides. While many other harbingers of a slump in economic activity tend to be practically contemporaneous with the slowdown itself, the yield curve is seemingly able to look over the horizon and provide several quarters’ advance warning.

Just as important as the reliability and predictive strength of this indicator are its simplicity and plausibility. These latter benefits are related. The difference between a long-term interest rate (typically the 10-year bond) and a short-term interest rate (alternatively the policy rate, a T-bill rate or yield on the two-year bond) is the entire metric.

Hence, even as macroeconomic, external and regulatory conditions varied considerably at the times when the yield curve became downward sloping over the past seven decades, all these influences were arguably already incorporated into interest rates. The unconditionality of this metric shouldn’t be too surprising.

After all, bond yields are really just aggregated market expectations of all the macroeconomic factors that influence growth, inflation and policy, and savings and investment decisions.

And if that weren’t enough to solidify confidence in the importance of this measure, there is a causality argument. Most analysts view an inverted yield curve as being anticipatory of an approaching economic slump. However, there is some validity to the notion that an inverted yield curve itself can help promote a negative feedback loop within the broader real economy.

So, it’s not just the collective foresight of the US bond market that – for all intents and purposes – predicts recessions each and every time, but it is the very occurrence of long-term interest rates being less than short-term rates that helps bring about the slump. This negative effect would most clearly permeate through the banking system, which relies on an upward-sloping yield curve to be profitable.

Weakness in the ability of the economy to generate credit almost inevitably harms economic growth, so it’s quite conceivable that yield curve inversion may actually help bring about recessions – which would certainly bolster the metric’s predictive ability!

IS THIS TIME DIFFERENT?

But what are the counterarguments to the implications of the ‘true’ US yield curve inversion that recently arose, or equivalently, to invoke the most dangerous question in economics: is this time different?

There are two key differences for the US bond market between the current era and prior decades. The first is financial repression – the extent to which policymakers have actively influenced bond yields through direct, unconventional means. The second is the substantially globalised nature of G10 sovereign debt markets and how distorted these markets have become through their own central bank involvement.

The former simply means that one can’t necessarily trust the signals being provided by a market that has been deliberately distorted by the Federal Reserve Board (the Fed), principally through its quantitative easing (QE) programme. The latter implies that, even when the Fed isn’t directly influencing US Treasury yields, the substitutability among G10 sovereign bonds means that central bank interference anywhere will filter through to other markets, including the US. These differences certainly lend weight in applying additional scepticism to the signals being sent by the US yield curve. So, to return to the original question: is the intense concern generated by yield curve inversion in the US justified or not? For most people the concise answer would still be ‘yes’, despite the counter arguments. But for long-term investors, the original question itself is largely irrelevant.

US RECESSION: WHEN, NOT IF

Long-term investors are always interested in what’s beyond the next phase of the business cycle. It isn’t controversial to suggest that the US is facing a slowdown. Exactly when it will occur and how deep the slump will be are important cyclical questions, but there are far more significant, secular uncertainties to contemplate.

Indeed, these structural questions are already being posed in many economies and bond markets around the world. The US will very likely face these same challenges in time, but they are immediate for most other developed markets.

Underlying these concerns are two interrelated questions: what is the effectiveness of monetary policy from this point and how (un)sustainable are negative interest rates?

THE FUTURE OF MONETARY POLICY

The key is to recognise that the current, synchronised global slowdown is substantially different to the downturn that materialised in the wake of the 2008/2009 Global Financial Crisis (GFC). Central bank optimists will highlight that this is a positive starting point: the vastly expanded toolboxes of the European Central Bank (ECB), the Bank of Japan, the Bank of England and the Swiss National Bank, among others, can be more quickly and assertively deployed. Previously, short-term policy rates were really the only primary tool to ease monetary conditions, but, through dire necessity, a much broader set of interventions came to fruition, along with a greater willingness to embrace unorthodox methods. The problem is whether the limits of even these unconventional interventions might already have been reached.

The most blatant sign that monetary policy in many parts of the world may be pushing up against an effective limit can be seen in the extent of negative interest rates.

The landscape is unprecedented. Over a quarter of the global bond market (c. $15 trillion of the Bloomberg Barclays Global Aggregate Bond Index) now trades with a negative yield (see Figure 2). And with the US being the second-to-last major bond market with an all-positive yield curve (the UK is the other), this means that nearly 90% of the positive yield being generated from the global investment-grade bond market comes from America.

Furthermore, unlike previous episodes of negative-yielding debt, not only are large proportions of sovereign and investment-grade corporate bond markets trading at below-zero interest rate levels, but this has even infected some parts of ‘high-yield’ bond markets (sub-investment grade or junk), making a mockery of price-based risk discrimination within certain jurisdictions.

NEGATIVE-YIELDING BONDS ARE OBVIOUSLY IRRATIONAL … OR ARE THEY?

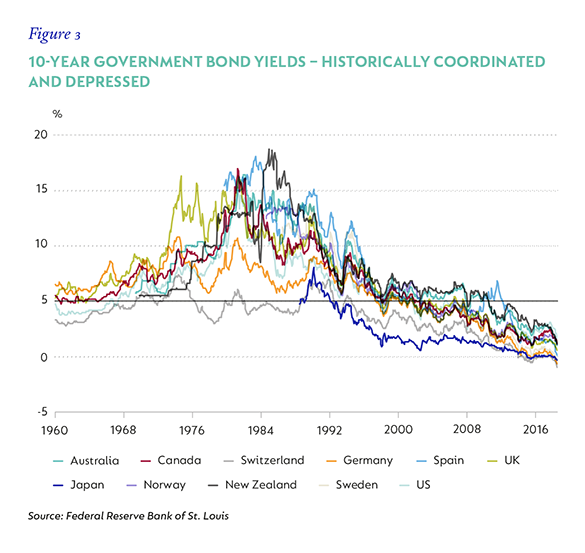

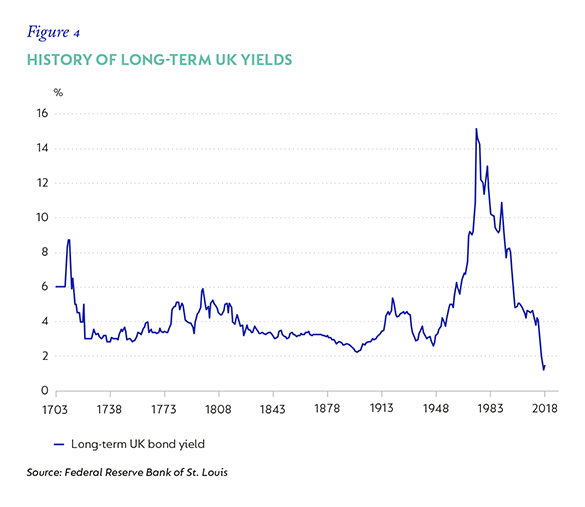

It seems absurd that literally thousands of billions of dollars’ worth of bonds are trading with negative yields; has the global bond market collectively lost its mind, quaffed generously from a “Drink Me” potion and willingly plunged down the infamous rabbit hole (as suggested by the long- and very long-term yields in Figures 3 and 4)?

The answer is: maybe not. There is a variety of rationalisations for holding negative-yielding bonds. The first fallacy to displace is the overwhelmingly widespread notion that buying a negative-yielding bond guarantees a loss-making investment. This is patently not true for holding periods of less than maturity where capital gains outpace the losses from negative yields. It is also not necessarily true for bonds bought with a negative yield and held till maturity. Provided a bond has an initial non-negative coupon (as all bonds currently do) and reinvestment rates aren’t always negative, the total return over the life of the bond may still be positive.

As such, if bondholders were momentum-driven investors with short-term horizons or long-term holders not overly concerned by market-to-market losses in the intervening period, a strange equilibrium could be sustained whereby views for a return to positive rates and even more deeply negative rates could co-exist and negative yields could be maintained.

A less far-fetched rationalisation for the sustainability of negative-yielding bonds for an extended period lies with a more entrenched fear of deflation. In the face of a potentially protracted period of negative inflation, nominal bonds are typically the superior asset class to hold. With declining price levels, any asset that can provide a sustained nominal cash pay-out becomes very valuable.

Another way to see this is to focus on the real yields provided by nominal, fixed-coupon bonds; these can very well be positive in a deflationary environment. And aside from the fixed cash-flow profile that nominal bonds provide, they become even more valuable relative to other asset classes, which tend to struggle in the macro-economic climate that accompanies an extended period of deflation. This is the ‘Japanification’ scenario whereby a similar fate that befell Japan over its lost decade strikes elsewhere, with Western Europe being highest ranking on the candidate list.

An even more reasonable class of justifications for the viability of negative-yielding bonds lies with investment portfolio dynamics. What many bondholders will have found reassuring in recent months is that the ‘safe-haven’ characteristics of bonds trading with negative yields have been sustained. This means that these are still reliable defensive assets.

So, from a portfolio construction basis, while these bonds may well be vulnerable due to exceptionally high valuations, they also continue to provide a nominal income stream and offer their traditional diversification benefits (including capital preservation and negative correlation to growth assets) within a multi-asset class context. And it is these latter characteristics that are highly sought after within any holistic investment portfolio. Indeed, they are scarce enough that investors may even be prepared to pay up for these features; a cost potentially represented by negative yields.

But perhaps the most feasible validation for seeing sustained negative global bond yields lies with market expectations. In the context that the short-end policy rates of major central banks were increasingly seen as being set around or below zero for an extended period, it would be rational to anticipate equally subdued long-term rates. Indeed, provided the equilibrium real rate of interest (or ‘R-star’ in economists’ jargon) was believed to have reset to a very low level, the danger posed by bond yields ‘normalising’ to some pre-GFC long-term neutral level is effectively neutered. Hence it is the notion – increasingly more plausible to investors – that structural factors are responsible for a lower equilibrium real rate (essentially where inflation and unemployment are in balance in an economy).

In particular, globalisation; technological changes, through digitisation; demographics, through the ageing developed world; and even the wage-bargaining process, through the shift in the relative balance of power between capital and labour, have lowered inflation and altered the relationship between inflation and other economic variables. And regardless of where the balance lies in these explanations, provided belief in lower inflation is increasingly attributed to structural rather than cyclical causes, then the more justified the notion of entrenched low interest rates becomes.

NOT A REVIVAL OF THE POST-GFC CENTRAL BANK PLAYBOOK

It appears that central banks and markets have been rapidly adjusting in preparation for a rerun of the post-GFC interval that saw exceptional monetary easing over a protracted period. After all, policy rates have been cut widely, lending operations have been revived, asset purchase programmes reinvigorated and forward guidance is open-ended once again. However, there is a crucial difference this time around.

There is significantly more widespread recognition that monetary policy has reached some – if not all – of its effective limits. Perhaps the greater area of dispute now is around whether exceptional monetary easing, especially negative rates, is actually counterproductive to its own aims or whether these ill effects are long term enough in nature (or manageable) that aggressively loose monetary policy is still better than nothing – even if it’ll do little to solve deeper productivity issues facing most economies.

This complexity was highlighted at the ECB’s September policy meeting. Much of the attention was focused on the Bank’s monetary policy adjustments, especially the de facto open-ended revival of bond purchases to the tune of €20 billion per month. However, the underlying messaging was very clear: monetary policy cannot be the only heavy lifter.

Without fiscal expansion, European growth will remain anaemic and a form of secular stagnation will likely take hold. The departing ECB President, Mario Draghi, even while reviving easing mechanisms for the Euro-area (and adding a few monetary innovations too), unequivocally emphasised that fiscal policy needs to become the main instrument to stimulate demand.

This clear and forceful endorsement from such an eminent policymaker should – in an ideal world – have significant traction in finance ministries across the Continent. Yet this is not a given. Resistance to perceived sovereign profligacy has been legendary in Northern Europe. After all, it isn’t coincidental that the German word for ‘debt’ (Schuld) is the same for ‘guilt’.

The most that can be said is that the debate has already begun to shift. But while this has been a global phenomenon, it has unfortunately been slowest to evolve in Europe – the developed world geography that most urgently needs a different policy configuration.

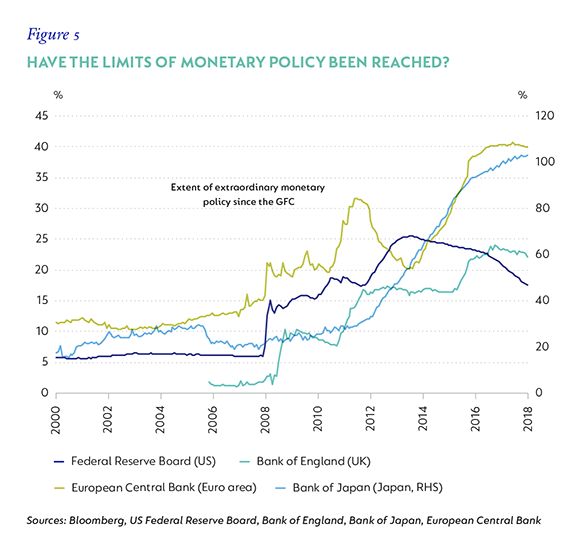

And so, the market’s answers to the imperative questions facing bond investors reflect deep scepticism about the effectiveness of monetary policy tools, both interest rates and unconventional interventions, from this point (see Figure 5). As such, the potential for an extended period of exceptionally low interest rates is seen as quite high, as the political courage to forego extraordinarily easy monetary conditions is seen as absent.

Rates may be negative or slightly positive, but what isn’t doubted by the market is that they’ll remain so for a protracted extent. This itself reflects cynicism about policymakers’ willingness and ability to rebalance policy interventions to favourably boost growth and raise inflation.

THROUGH THE LOOKING GLASS – THE SOUTH AFRICAN CONTEXT

South Africa doesn’t face quite the same monetary policy restraints as those seen in developed markets. Real rates are still very much positive across the curve, inflation is low but set to remain in the upper end of the target band over the foreseeable future, and fiscal expansion certainly hasn’t been kept unduly restrained – in fact, quite the opposite. But it would be absolutely accurate to emphasise that South Africa’s growth issues go well beyond what monetary policy can sufficiently address – just like in much of the rest of the world.

However, with the globalised nature of fixed income markets, the direct influence of G3 (the US, Japan and the EU) risk-free rates on domestic bond yields always needs careful consideration. As such, it is instructive to consider the counterfactual: what would South African bond yields have looked like if there hadn’t been the most widespread and prolific reduction in developed market bond yields over the past three quarters or so?

Even with other countervailing forces, it is highly improbable that South African bonds would have fared particularly well in a world that was pursuing a continued de-escalation away from extra-ordinarily easy monetary conditions.

A higher level of global risk-free rates would have necessitated a commensurate adjustment to South African bond yields, while a reversal of capital flows from emerging markets back to a US dollar base would likely have exacerbated this process.

So, it’s fair to characterise this episode of global interest rate and spread compression as both a blessing and curse for South Africa. Without the offsetting gravitational pull of lower developed market yields, South African bonds would have almost certainly struggled to overcome the intensification of domestic fiscal difficulties.

The curse is that the market signal that this would have provided may have prompted a quicker and more compelling political response to address these difficulties in a more coherent and definitive manner than has been seen to date.

If the market’s prognostication for ineffective monetary policy and an extended period of very low developed-market interest rates pans out, South Africa has a window of opportunity to structurally turn around its current fiscal predicament and avoid a far more rapid and jarring correction to an unsustainable debt trajectory. It would be deeply regrettable if this passing moment of grace were to be squandered and a crisis were necessary to correct the imbalance.

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter