United States - Institutional

United States - Institutional

Economic views

What will be the cost?

“Battles are never the end of the war” – former US President James Garfield

- End-March data from around the world show the devastating economic fallout of Covid-19

- China and developed markets may partially recover by end of Q2-20, but emerging economies will bear the brunt to year end

- SA’s already considerable headwinds have intensified; our fiscal position is precarious

- Will this be the impetus for the policy action that has thus far been lacking?

“Battles are never the end of the war” – former US President James Garfield

THE CORONAVIRUS IS at once a health crisis and an economic crisis, which has already pushed the world economy into a recession. By trying to limit the human cost of the virus, governments are imposing a massive economic cost through lockdowns that close economies, which may well have longer lasting and more deeply damaging consequences that we cannot yet foresee. It’s possible that the ultimate socioeconomic price that the economic crash exacts will be hard to balance with the actual human cost of the virus. This is the tragedy we face.

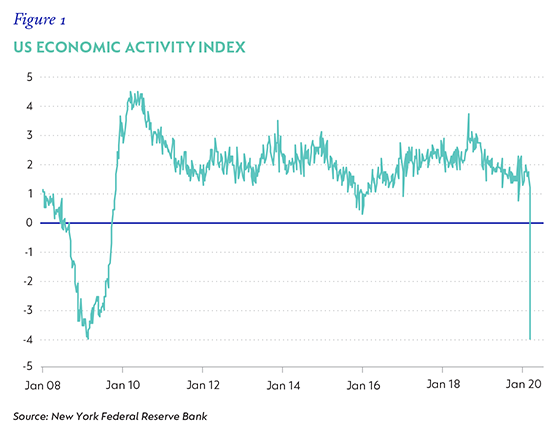

The sudden halt in economic activity over the past three months is unprecedented, and there is enormous uncertainty about the path ahead. With the oil price collapse, further demand-shock complexity is added to the mix. Early activity indicators have recently been published, showing the depth of the economic impact. Most charts look like the latest data point is an error (Figure 1). At the time of writing, China’s GDP for the first quarter of 2020 (Q1-20) contracted -6.8% year on year (y/y).

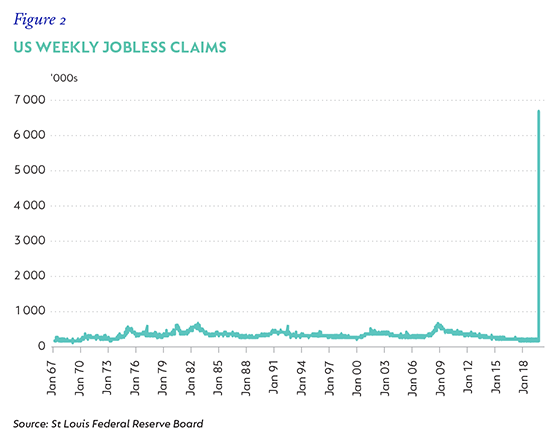

In the US, data measuring initial weekly jobless claims – the first indication of applications for unemployment benefits – double-spiked to never-before-recorded levels, dwarfing all crises since 1967 when the data starts. Cumulatively, weekly claims increased to over 22 million over the past four weeks, implying a spike in US unemployment to 20% in April – a level last seen in the Great Depression (Figure 2).

In response, economists who started revising global growth forecasts lower when China was hit by the virus at the start of the year, assuming supply chain and demand-related disruptions, are now in an ongoing cycle of downward forecast revisions. This latest set of data will show a deepening deterioration in coming months, given the tightening policy response that is widening the net of lockdowns during that time.

This places us squarely in the realm of the unknown, with not much more than (educated) guesswork informing forecast revisions.

Part of the challenge in assessing the economic impact of these shocks is, first and foremost, the ‘novel’ aspect of this virus: it’s new, and we simply don’t know how the pandemic will evolve. It’s also extremely difficult to untangle the complex interrelationships between the uncertain evolution of both the severity and the duration of the economic shock, and what these mean for future recovery. Further, the effects of the swift and unprecedented global monetary and fiscal responses need to be considered, and the degree to which these measures can protect underlying economic resilience and assist recoveries on the other side.

What we know about the economic crisis currently unfolding is broadly shaped by the following assumptions:

- Asia

China’s economic growth collapsed in Q1-20. Early data suggests a modest second-quarter (Q2-20) recovery. Countries within Asia that are closely integrated into Chinese supply chains and trading patterns should suffer coincident weakness, but to varying degrees. For instance, with the early enactment of containment policies, South Korea and Taiwan have shown relatively lower infection rates and, to date, less severe cases, and stand to benefit as China recovers. - The developed West

Western Europe and the US are likely to see the depth of their economic slowdowns straddle Q1-20 and Q2-20. Growth had probably already contracted in Q1-20, based on what we are seeing in PMI and employment data. However, the intensity of the weakness is most likely to be felt in Q2-20 (and perhaps beyond), as public policies aimed at containing contagion were implemented at different paces and with different intensities in these regions. - Non-Asian emerging markets

The impact on non-Asian emerging markets remains uncertain, but these countries will certainly not be immune. The full impact on Southern Hemisphere countries is mostly yet to be seen. Initial transmission lagged, and government responses have varied widely. Emerging economies have different socioeconomic profiles but, broadly, have weaker healthcare systems; lower quality institutions (including financial); and large proportions of the population - whose immune systems are more likely to be compromised - living in close proximity, makes social distancing almost impossible. In addition to the social challenges, emerging markets are facing tighter financial conditions and are more likely to suffer the consequences of a return-to-normal demand sooner than developed economies. It’s very likely that the economic impact on emerging economies will be more enduring than for their developed counterparts and may linger through year-end.

UNPRECEDENTED STIMULUS

It also isn’t clear that the depth of the economic downturn will be any real guide to its recovery; this will depend on the effectiveness of interventions to contain and treat the virus. Importantly, global policymakers have mobilised enormous fiscal and monetary resources, estimated at close to 6% of global GDP. These interventions primarily aim to:

- Ensure that financial markets are liquid and continue to function – these are the lifeblood of the global economy;

- Ensure that companies don’t close, forcing a permanent loss of economic capacity; and

- Protect jobs.

While the depth and breadth of these interventions are unprecedented, it’s still too early to estimate their effectiveness. In some cases, the announced policies have yet to be implemented. But the most important issue is that these policy responses aim to mitigate the demand shock that has come as a result of lockdowns.

Mitigating the supply shock, namely enabling people to return to work, requires a resolution to the health crisis. At this stage, this would require a much broader base of testing for the virus so that governments, companies and households are comfortable enough to start a slow pace of normalisation. Again, we are hostage to its unknown prevalence, and this remains a weak link in any assessment of an economic recovery.

The IMF recently published its Spring World Economic Outlook. Amidst great uncertainty and predicated on a moderate recovery in the second half of 2020, global GDP is expected to shrink -3.0% in 2020, and then recover to an above-trend 5.8% in 2021. Within advanced economies, the US economy is forecast to contract -5.9% in 2020 and then recover to growth of 4.7% in 2021. In Europe, the impact of the pandemic has been more severe, with a recession measuring -7.5% this year, to recover 4.5% in the next. The uncertainty regarding emerging markets is acute – in many cases the worst is likely still to come, with considerable health and economic vulnerabilities. Emerging market growth is expected to contract 1.0% in 2020, and to rebound 6.6% in 2021, led by a 9.2% growth recovery in China. Despite these strong growth recovery forecasts, neither developed nor emerging market GDP is expected to recover to pre-crisis levels over the forecast period.

THE LOCAL SITUATION

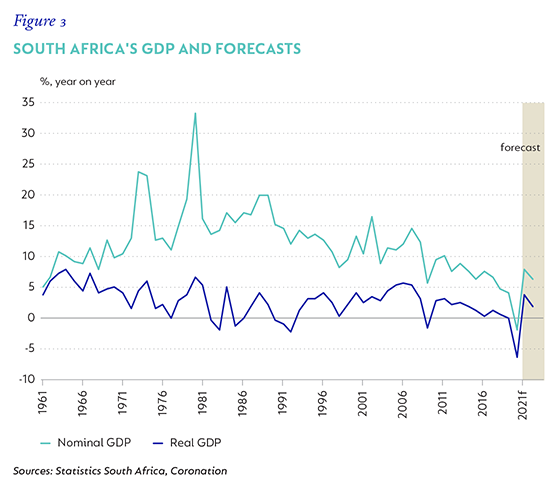

South Africa faces these same challenges, but with even greater health crisis uncertainty and an unfolding economic crisis against which we have very little defence, due to our already weak economic position. Even before the lockdown, most economists had lowered growth forecasts due to severe electricity constraints, and GDP was broadly forecast at below 0.5% in real terms, following a paltry 0.2% growth in 2019 (Figure 3) .

In February, the Minister of Finance warned that the fiscal deficit would amount to 6.8% of GDP, and that the total funding of this deficit and other fiscal obligations would be even bigger, at 8%. On 23 March, President Cyril Ramaphosa announced a three-week lockdown starting 26 March to ‘flatten the curve’ of infection. The decision will most certainly limit the ultimate human cost and better prepare the fragile healthcare services sector for an inevitable escalation in infection. As elsewhere, however, the economic cost may be higher and longer lasting than the health crisis. The lockdown effectively cripples about 45% of the productive economy. While some essential services, and small parts of the retail sector remain open, tourism and related industries are not only completely shut, but will take a long time to recover. The export sector will also be hard hit, including agriculture.

Since then, the lockdown has been extended a further two weeks to the end of April, with few changes to the imposed restrictions. Some parts of the mining and agriculture sectors, as well as industries associated with essential services have seen some conditions lifted, but the lockdown on the rest of the economy, for now, is acute.

Forecast revisions to account for such an unprecedented shock suggest GDP may contract by between 5% and 10% in 2020. Recently, the South African Reserve Bank (SARB) released updated forecasts, which now see GDP contracting -6.1% in 2020, with a modest rebound to 2.2% in 2021. Our estimates suggest a -13% y/y contraction in Q2-20, and a weak recovery into year end, given the uncertain progress of the pandemic, both globally and at home. At Coronation, our expectations are for a marginally tighter contraction of -6.4% in 2020 and a more ‘robust’ rebound of 3.8% in 2021. Again, this still implies that the level of GDP at the end of 2021 will be below where it was in 2019 (Figure 3).

Such weak economic growth, coupled with a much lower oil price, should keep inflation at low rates in the short to medium term, although some pass-through from the weaker currency and supply disruptions seem likely as things normalise. Consumer price inflation is forecast to average 3.4% in 2020 and 4.0% in 2021.

POLICY ACTION

Policymakers have been quick to respond. The SARB’s Monetary Policy Committee announced a cumulative 225-basis point cut in the repo rate this year, from 6.50% to 4.25%, enabled by weak economic growth, low inflation and well-anchored expectations. In addition, the SARB has acted to ensure that the financial markets continue to function properly and that there is sufficient liquidity to meet cash demand. The SARB has introduced twice-daily repo operations and increased the term of its refinancing that it will purchase government securities in the secondary market, should dislocations arise.

On the evening of 21 April, the President announced a R500 billion (~10% of GDP) government response package. This aims to meet a range of needs, including support for the vulnerable (extended Unemployment Insurance Fund (UIF) payments and direct transfers to households), wage support, protection for companies via loan guarantees and tax relief, municipal assistance, and financial support for the healthcare sector. Of the R500 billion, R200 billion is for a loan guarantee scheme, R100 billion is to create and protect jobs, and R70 billion will go towards tax relief through the granting of deferred payments.

Final funding arrangements have yet to be published by the Minister of Finance in a pending Appropriation Budget. But, as far as we can account, of the total R500 billion, R130 billion will be reprioritised from existing Budget allocations, while multilateral funding from a combination of loans from the IMF, the World Bank and the New Development Bank could yield about R120 billion. The loan guarantee scheme of R200 billion is through partnership with the local banks and the SARB. This is likely to be a contingent liability at first, with an uncertain drawdown – so the actual cost is uncertain, and the impact on government’s contingent liabilities will also depend on whether the full scheme is taken up.

Future deficits will be affected by the proportion of loans that turn bad. The remaining resources include the UIF, which we think will fund some of the job protection and wage support allocations. Overall, additional funding is likely to be significantly less than the total package implies, but will, on balance, add to the large fiscal fall out of the crisis.

In addition, the ultimate fiscal cost will depend on the economic recovery after the lockdown, which is, in part, dependent on the duration of the lockdown. However, the fiscal intervention is a welcome support that should materially assist in limiting the downside risk to economic growth from this crisis.

FISCAL SQUEEZE

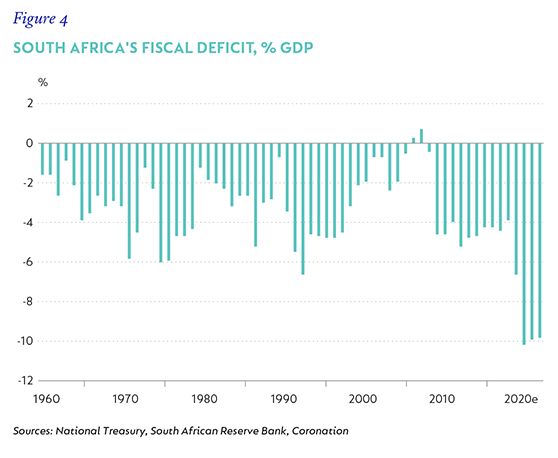

The fiscal implications of this are extremely negative. The fiscal deficit is expected to exceed 10% of GDP in our baseline and will be greater once we include the details of government’s response the crisis (Figure 4). The sharp drop in revenue and the likely very-low nominal growth that follows a shock like this, makes funding the shortfall extremely difficult. Under our baseline, the public sector borrowing requirement will exceed 11% of GDP in each of the next three years. Government debt will continue to accumulate, with nominal growth well below nominal funding costs, with the latter likely to rise (Figure 5).

A THREE-PEAK CHALLENGE

Policymakers are going to face three material challenges in coming months: the impact of the pandemic on the people and economy of South Africa, with a structurally damaged fiscal position that requires funding; ongoing pressure on capital flows from the financial account, which complicates that funding; and the likely pressure this will place on the financial system.

While government’s crisis response is a necessary intervention, it remains to be seen whether it has enough credibility to anchor market expectations about the effectiveness of the programme and the likely impact on fiscal sustainability in the longer term. The SARB has shown willingness to respond timeously to financial constraints and has the capacity to do so. We expect these interventions to increase in coming months, but warn that they are not without risk, and we expect SARB policy to remain prudent. In this regard, some external funding arrangement(s) seem inevitable, both in the short- and the longer term.

CAN WE FIND OUR FOOTING?

In such an uncertain environment, it’s difficult to know what to do, but where possible – and especially in light of South Africa’s fragile fiscal position – proactive contingency planning can go a long way to support confidence and reduce uncertainty. In the eye of the crisis, global financing institutions are more likely to respond more generously than they would otherwise, albeit not without the necessary conditionality.

We are encouraged by President Ramaphosa’s timely intervention to mitigate the pandemic’s damage; we are aware of the hard work being done by the National Treasury to prepare for the interventions that will be needed; and the partnering of private and public health officials ahead of time will surely improve South Africa’s healthcare officials ahead of time will surely improve South Africa’s ability to respond. Members of the private sector have also contributed generously to support policymakers, public efforts and small enterprises.

Let this also be an opportunity for government to accelerate and implement its growth strategy with critical vigour, because the best way to address these challenges is to help, by all means possible, the economy to grow.

Disclaimer

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter