United States - Institutional

United States - Institutional

The third quarter (Q3-22) began with asset prices rallying off a depressed base as markets looked out towards a peak in both inflation and central bank tightening. However, the promising start could not be sustained, and the rally faltered as central banks raised policy rates more aggressively than expected to quash inflation that remains persistently high amidst unemployment levels that remain persistently low. Once again, risk aversion returned, pushing bond yields to levels not seen since before the Global Financial Crises and returning equity indices to levels below those experienced in June.

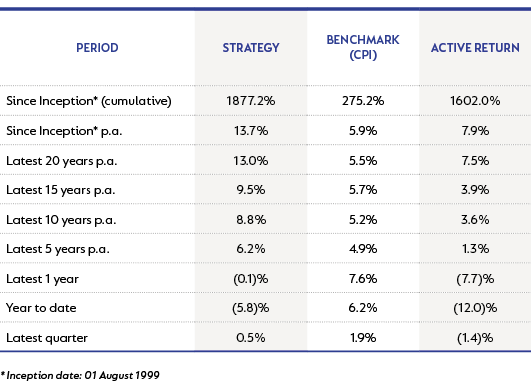

The quarter ended with the domestic Capped SWIX Index 2.4% lower, listed property down 4.1% and the All Bond Index marginally positive. Global markets fared even worse with the MSCI All Country World Index 6.8% lower, the MSCI Emerging Markets Index down 11.6%, and the World Government Bond Index down 7.6%. Ongoing dollar strength was a feature of the quarter, resulting in a rand that was 10% weaker against the USD, cushioning the impact of the declines in offshore markets. Taking into consideration the impact of the negative moves of the first half of this year, over the past 12 months no asset class has delivered returns in excess of South African inflation, which is itself elevated at 7.4% but below levels currently being experienced in most developed markets. As a consequence, the Strategy’s performance as at 30 September 2022 is shown below:

The Strategy’s allocation to global assets continues to be the largest detractor from performance over the past year. Exposure to global stocks contributed negatively to Strategy performance, although rand weakness resulted in positive contributions for Q3-22. As part of our approach to risk management, we maintain a level of put protection (currently approximately 20% of global equity exposure) and this has provided some offset to the negative returns.

Domestic assets have contributed positively to Strategy performance over the past 12 months with good equity and bond selection delivering returns ahead of their respective indices. Within domestic equities, holdings in British American Tobacco, Anglo American, Gold Fields, Exxaro and RMI Holdings were the largest contributors to returns, while holdings in Quilter, ABSA, Spar and Aspen detracted.

RMI has been one of the top performing shares on the SA market over the past year. Following the announcement in September 2021 of the unbundling of its stakes in Discovery and Momentum Metropolitan Holdings as well as the disposal of its stake in the UK property and casualty insurer Hastings, RMI has continued to perform strongly. Proceeds from the disposal have been applied to paying down debt and returning excess capital to shareholders. We consider the remaining business, OUTsurance, to be one of the more attractive growth businesses in our market as it expands beyond the domestic personal lines insurance core business into adjacent insurance markets and other territories. The company is run by a highly entrepreneurial and energised management team that is closely aligned with shareholders by virtue of their 10% shareholding in the business. The share currently trades at a small discount to the valuation disclosed by management in the latest NAV stack-up, which following the group restructure will likely not be disclosed again. We believe the market anchors off this number, which fundamentally undervalues the business. RMI represents about 2% of the SA equity carve-out, or 0.7% of Strategy.

Within domestic fixed income, the biggest contribution came from holdings in inflation-linked bonds (ILBs). We continue to see real yields on offer from SA government bonds as attractive, in part due to the benefits of an improved fiscal position following a period of high commodity prices. This notwithstanding the structural challenges faced by the domestic economy and an ongoing rise in global bond yields. Risk is managed by keeping the duration of the Strategy’s bond carve-out lower than that of the ALBI but at a real yield that remains compelling.

During the quarter we were net sellers of SA equity, and buyers of SA fixed income including ILBs. In addition, we have added exposure to global equities as they continue to sell off and we see the opportunity set as increasingly attractive. Although it is difficult to call currency moves with great conviction, we will take active views when we feel that these moves are extreme, using currency derivatives (the derivatives position will benefit from rand strength and detract if the rand weakens). Towards the middle of the quarter, we closed out a position as the rand strengthened towards R16 to the USD, but at end of the quarter, as the rand breached R18 to the USD, we once again hedged a portion of the currency exposure.

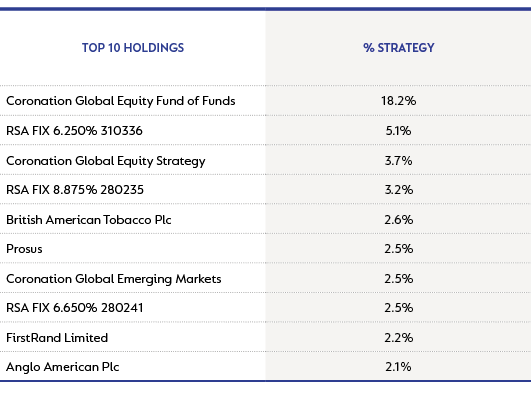

Our asset allocation and top 10 holdings as at 30 September 2022 are shown below:

The global economy continues to face an unprecedented number of challenges simultaneously: an energy crisis, particularly in Europe; growing concern about Chinese policymaking and growth, including the impact of sporadic Covid lockdowns and a troubled property market as well as its intentions towards Taiwan; the ongoing war in Ukraine, in which tensions appear to be escalating further as President Vladimir Putin threatens the nuclear option; as well as significant global inflation and monetary policy tightening. To top this off, at the end of the quarter the debacle around a poorly thought through and unfunded fiscal stimulus package from the new leadership in the UK, forcing intervention by the Bank of England, has contributed to further nervousness in global markets. While this is currently a crisis specific to the UK, there is risk of contagion as fears emerge (rightly or wrongly) about something similar happening in other markets.

These numerous challenges are likely to remain with us in the near future, and recessionary pressures are increasingly evident, especially in Europe. However, towards the end of Q1-23 prices will start to lap a high base, reducing the upward pressure on inflation and providing space for an end to monetary policy tightening. Valuation remains our anchor in allocating capital and although there is clearly downside risk to future earnings expectations, we believe that much of the bad news is discounted in asset prices. After a challenging past 12 months, we see very attractive opportunities in the returns currently on offer in both domestic and global markets, with the notable exception of developed market government bonds. Domestic equities are trading on inexpensive multiples and high dividend yields, domestic bonds offer very attractive real yields, and while global equity indices are not necessarily cheap, pockets of global equities are very attractively priced following a relatively indiscriminate sell-off. While the near term is fraught with uncertainty, we continue to be of the view that the Strategy remains well placed to provide positive real returns over the medium term.

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter