United States - Institutional

United States - Institutional

Investment views

Click to travel

Experiences are trumping consumerism.

The Quick Take

- Covid-19, economic uncertainty, and Ukraine war have provided opportunities to invest in leading travel companies at attractive valuations.

- Consumer sentiment is weak but there is significant pent-up demand for travel.

- Booking Holdings and Expedia generate significant free cash flow with shareholder-friendly management and capital allocation.

‘If there’s life, there’s travel.’ - Barry Diller, Chairman of Expedia during the depths of the Covid-19 pandemic

The Covid-19 pandemic was highly disruptive to travel, with wide ranging restrictions resulting in a collapse of bookings. The initial Covid-19 lockdowns were an existential threat for the travel industry. However, once the worst of the restrictions were over, the subsequent stop-start nature of the recovery coupled with concerns about inflation and recessionary conditions, have given active investors opportunities to buy into some of the leading travel exposed companies at attractive valuations.

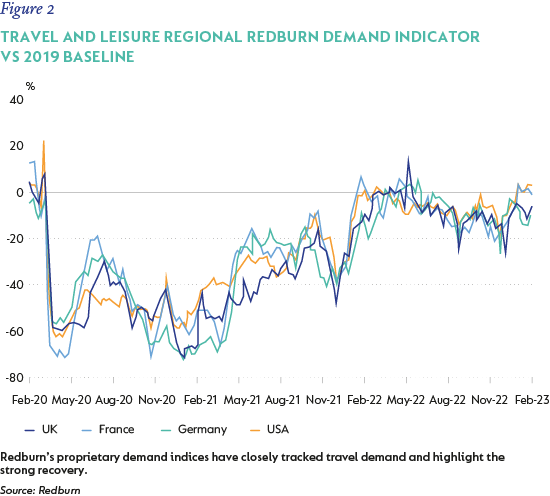

High levels of inflation stemming from the after effects of the pandemic and the war in Ukraine have resulted in weak levels of consumer confidence globally (Figure 1). Despite this, pent up demand to travel has meant that as Covid-19 restrictions ended, travel demand has recovered back to pre-Covid levels (Figure 2). Consumers have prioritised spending on travel and other experiences over buying more ‘stuff’ after being stuck at home for several years.

Coronation’s global funds’ exposure to travel is through positions in the online travel agencies (OTAs). These businesses are capital light and generate significant levels of free cash flow. The OTAs principally service leisure travel demand and have little exposure to formally managed business travel and the associated structural headwind from the proliferation of virtual meetings post-Covid.

THE MAIN ATTRACTION

Booking Holdings, owner of the eponymous Booking.com, has been our preferred pick. The company has a decade plus track record of excellent execution, strong leadership, and exceptional free cash flow generation. For the decade ending 2019, strong growth in the rate of travelers booking their accommodation online allowed Booking to compound room nights, gross bookings, revenues, and earnings per share (EPS) at 30%, 26%, 20% and 26%, respectively. It is undeniably the blue-chip company within the online travel landscape.

With online bookings now accounting for approximately 50% of all accommodation bookings, the industry is more mature. In the next decade we don’t expect Booking to come close to matching the last decade’s phenomenal growth, but still believe that the company has an attractive future. This view is underpinned by travel demand outgrowing global GDP growth and further modest gains in the penetration of online accommodation bookings.

After releasing its results for fourth quarter of 2022 in February this year, the company substantially increased its stock buyback authorisation to $24 billion, representing a quarter of the current market capitalisation! The company will return 100% of its substantial free cash flow to shareholders over the next three to four years as well as assume a modest level of leverage to buy back stock. This should allow the company to buy back approximately 8% of its shares in issue annually over this period. We expect the company to be able to compound earnings per share at a mid-teens rate over our investment horizon.

The stock has recovered strongly off its lows, but still trades at an approximately 19 times rolling 12-month forward EPS. We still believe it offers reasonable value.

ALSO ATTRACTIVE

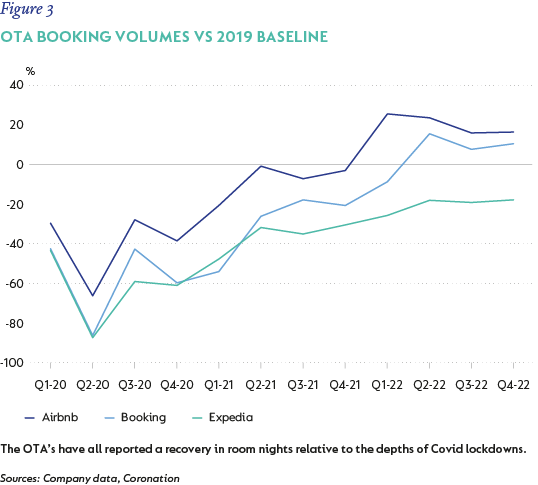

Expedia has a history of inconsistent execution. Having put off some long overdue structural reforms, management used the opportunity presented by the pandemic to restructure its business and resolve some longstanding inconsistencies in its business model. For instance, the company’s disparate group of brands would often compete against one another in Google’s key word auctions, inflating the auction bids without gaining incremental bookings. Addressing these structural issues required the company to walk away from some low-margin uneconomic business, ceding some market share to competitor Booking.com in the process. This is evident in Expedia lagging Booking.com in post-Covid room night recovery, as illustrated by Figure 3.

Lingering fears about ongoing market share losses to Booking.com, a more highly levered balance sheet and questions surrounding marketing efficiency have resulted in the stock lagging Booking materially. With Expedia trading on approximately 13 times our estimate of rolling 12-month forward EPS[1] and a double-digit free cash flow yield, we believe the stock is pricing in a scenario of ongoing share losses to Booking.com and the potential impact of a weak macroeconomic environment on travel demand. The company, while operating with a higher degree of leverage than Booking, is also actively buying back stock, albeit not as aggressively.

Airbnb is the last of the three online travel companies in our consideration set. In just over a decade, Airbnb has established a phenomenal brand that has become synonymous with alternative accommodations. The term Airbnb has entered the vernacular as both a verb and a noun. The most powerful demonstration of the power of the Airbnb brand occurred during the initial Covid lockdowns. Faced with an abrupt and almost complete halt of all business overnight, the company was left with little option but to cut costs aggressively to try and save the business. All marketing, including performance marketing in Google’s search channels, was turned off. That this had almost no impact on the business demonstrates the power of the brand. Once lockdowns ended, travelers sought out Airbnb’s website and app directly. Today, the company sets itself apart from its online travel peers by sourcing 90% of its customer traffic directly, rather than via Google or other channels.

Once the initial lockdowns ended, Airbnb benefited from travelers looking to avoid crowded cities and hotels, and to travel in groups with close friends and family. Strong growth coupled with Covid-induced cost discipline has resulted in strong growth and a significant positive inflection in margins. The business has grown up overnight.

Airbnb is a great business with a rosy outlook, but a full price earnings ratio of approximately 31 times EPS, which doesn’t reflect $1 billion of annual stock-based compensation, leaves us waiting for a more attractive entry point.

CONCLUSION

Travel is a cyclical industry, and we are realistic about the potential for recessionary economic conditions negatively impacting travel demand in the months ahead. There are, however, several mitigating factors:

- As patient long-term investors, we expect travel demand, whilst cyclical, to continue to outgrow global GDP growth through an economic cycle, as it has done for many years. With the headwind from lower business travel now in the base, we believe that GDP-plus type growth is achievable off of this new base.

- Valuations of the OTAs we hold in the funds still screen as attractive, in some cases pricing in what we believe to be a dire outcome.

With this in mind, we are optimistic about the long-term value that these holdings offer our clients.

[1] We add back stock-based compensation to reported non-GAAP EPS.

Disclaimer

SA retail readers

SA institutional readers

Global (ex-US) readers

US readers

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter