United States - Institutional

United States - Institutional

Investment views

Next-generation entertainment

Cable operators leading US broadband internet momentum

- The TV shift from linear to OTT is still nascent in the US and momentum will increase

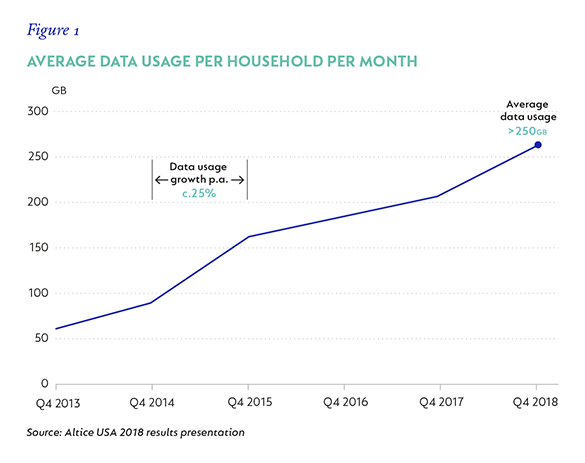

- The average US cable household consumes over 250GB per month

- Broadband internet will be the backbone of next-generation entertainment

- Broadband is now the primary product sold by cable operators, while pay TV is less relevant

IN THE LAST edition of Corospondent, we discussed how consumer habits have evolved with respect to entertainment and how viewership continues to shift away from traditional live television to on-demand video streamed over the internet. The transition of entertainment and communication to online is still in its infancy and we expect the trend to continue. Against this backdrop, we believe cable operators are well placed as the leading providers of broadband internet in the US.

Both Charter Communications and Altice USA have materially outperformed the market year to date, up around 45% and 70%, respectively, and we continue to hold both as core positions in our active global equity portfolios. Although the market has traditionally focused on cable’s declining pay-TV business, broadband internet is the primary product sold into the home. With the strong growth in its customer base, broadband now contributes almost all of the free cash flow generated by the cable operators. As consumers continue to shift to streamed video, broadband will become the backbone of next-generation entertainment, the importance of which will continue to rise, and our view is that the cable investment case is misunderstood and under-appreciated by the market.

As reflected in Figure 1, these strong structural trends have resulted in a rapid increase in data demand, with the average US cable household consuming over 250 Gigabytes (GB) of data per month, while households that don’t subscribe to traditional pay TV use roughly double that.

This is a clear illustration that cord cutters consume more data as video content is streamed via the likes of Netflix and other over-the-top (OTT) providers. Data consumption is only set to increase further, with Altice USA disclosing that its most data-hungry homes (the top 10% of users) consume one Terabyte of data per month and have 15 or more connected devices. In time, it’s fair to expect this to become the norm as streaming-use cases expand to include higher quality video as well as connected home and gaming applications.

WHAT IS CABLE?

Cable was initially conceived to bring free broadcast television to mountainous areas unable to receive adequate signal through the air via antenna systems. A cable system can be thought of as an electricity grid transmitting data from one point to another, and at its core consists of a mix of copper and fibre transmission lines. Today, most US homes and businesses have cable running past them, dug into the pavement decades before, and cable has both an advantaged infrastructure and natural monopoly in most US towns and cities. The rapid construction of cable infrastructure started in the mid-50s and was followed by decades of footprint expansion and consolidation led by players such as the legendary John Malone.

The cable-use case soon shifted from broadcast to pay TV, leading to the establishment of well-known channels such as ESPN and HBO. For many subsequent years, cable was primarily focused on selling a traditional bundle of pay-TV channels, as DSTV does today. Cable is a scale game, and years of footprint consolidation means that the three major listed US operators – Charter Communications, Comcast and Altice USA – now pass 51 million, 58 million and nine million homes or businesses, respectively!

THE SHIFT TO BROADBAND

It’s no secret that traditional, ‘linear’ TV subscriber numbers are declining, and we expect this to continue. Cable operators have repositioned themselves with broadband as the primary focus, enabled by extensive plant upgrades that started at the turn of the century and continue to this day.

Much of the original footprint has been replaced with fibre, and networks have been digitised and upgraded, resulting in speeds of one Gigabit per second (Gbps) being readily available. Operators have already identified a realistic, low-cost path to 10Gbps.

As a result of its well-established position and advantaged infrastructure, cable has continued to take share of the US broadband market and today serves two thirds of all broadband-connected homes. Most US homes are passed by both cable and a telco line offering DSL (think Telkom); the latter offers insufficient speeds and continues to lose market share as data consumption explodes.

New competition is unlikely due to the cost of laying fibre and the questionable return on investment in doing so because of the difficulty in prying customers away from entrenched providers. Much of this cable was originally put down decades ago and it’s often near impossible to overbuild this infrastructure from a town planning or regulatory perspective. Today, the provision of broadband internet is cable’s primary cash generator.

WHAT ABOUT CABLE’S TRADITIONAL VIDEO BUSINESS?

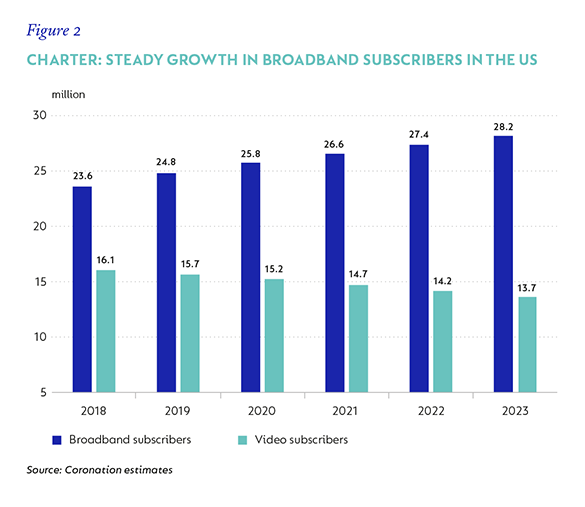

Figure 2 illustrates that while broadband is now clearly the primary service being sold into the home, video still comprises a significant proportion of cable operator revenue, although video users continue to decline by 2% to 3% per year. The video backdrop is one of intense competition, with traditional distributors like cable and satellite losing out to OTT platforms.

Furthermore, new services from deep-pocketed companies such as Disney and Apple are due to launch imminently.

This fight for eyeballs is driving content costs up, with timeless shows like Seinfeld and Friends recently costing around the $400 million to $500 million mark for new multiyear carriage deals, according to press reports, while Apple is reportedly spending over $15 million an episode on The Morning Show starring Jennifer Aniston and Reese Witherspoon.

IS IT VIDEO’S TURN TO DIE?

What does this challenging backdrop mean for cable operators?

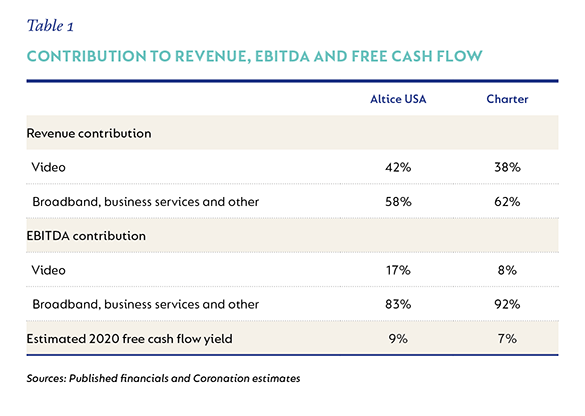

Table 1 clearly shows that video’s contribution to cable is smaller than the revenue headline suggests. Due to significant programming costs paid to channel and content owners, video is a very low-margin business and is estimated to contribute under 20% of total earnings before interest, tax, depreciation and amortisation (EBITDA) for the likes of Charter and Altice USA. Content costs are paid on a per-subscriber basis, and so naturally decrease in line with declines in the video subscriber base, smoothing the overall impact of video’s downward trajectory.

Furthermore, video contributes only marginal free cash flow to cable operators due to the high cost of putting set-top boxes into homes. We believe that the current pace of video subscriber declines is very manageable, and that new cable initiatives, such as the launch of aggressively-priced bundled mobile plans, will bring benefits such as broadband churn reduction, filling the gap that video once filled. While video is still an important element of the cable triple-play bundle, its contribution to free cash flow and therefore company valuation must not be overestimated.

TRADITIONAL VIDEO’S LOSS IS BROADBAND’S GAIN

While content owners slug it out for eyeballs and continue to write bigger cheques for new shows, a fast and consistent internet connection remains paramount to delivering the required streaming experience. It’s estimated that over 75% of internet traffic is video use, which clearly illustrates how a traditional video subscriber loss is broadband’s gain.

As the traditional television bundle is replaced with skinnier online options and individual apps, a complicated experience arises for consumers used to having all their video needs met in one place. In response, cable is making the right moves to leverage its primary broadband relationship into being the aggregator of choice in the modern world of streamed video, with set-top boxes now including OTT options in an easily searchable format.

WHAT ARE THE KEY RISKS TO CONSIDER?

Could technological change challenge cable’s advantage in the provision of broadband internet? We continue to monitor global developments around 5G and its potential to allow mobile operators to play a larger role in home broadband. 5G is the next generation of radio network technology and should bring significant benefits to the average mobile phone user, including higher speeds and increased capacity. US telecom giants like Verizon and T-Mobile have different strategies, but both envisage using 5G technology to provide home broadband. While we are not dismissive of this threat, the amount of data consumed by the average US household and the growth thereof make it difficult for mobile technology to compete with fixed alternatives such as cable and fibre.

The average US mobile customer uses under 10GB of data per month; even a tenfold increase in mobile capacity – the upper range suggested by industry experts – will struggle to compete with the average cable household consuming over 250GB per month and growing rapidly. 5G will also allow the use of previously untapped spectrum1 bands, and certain use cases will enable high-capacity home broadband solutions in limited circumstances. This high-frequency signal does not travel far and therefore requires more towers (connected with fibre) near to the end- consumer – an effective densification of the network. In these use cases, the lines between wired and wireless will become increasingly blurred and, ultimately, cable companies are well placed due to their ownership of existing wired infrastructure.

CONCLUSION

While cable stocks have performed strongly this year, Charter and Altice USA trade on 2020 free cash flow yields of around 7% and 9%, respectively – still a significant discount to the overall market. We believe this is too cheap, considering both companies have excellent, shareholder-friendly management teams and offer the potential for explosive free cash flow growth on the back of growing earnings and declining capital intensity.

In our view, the market is still overly focused on video declines and isn’t adequately rewarding cable operators for their strong, incumbent position as the leading providers of broadband internet. Broadband is a must-have, sticky product for consumers, and offers attractive margins and growing free cash flow profiles to the providers. We do not believe that this is reflected in current cable valuations. We continue to hold both Charter and Altice USA as core positions in our global portfolios.

1. Spectrum refers to a range of radio waves used by telecommunication providers for wireless communication purposes.

Disclaimer:

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter