United States - Institutional

United States - Institutional

IN RECENT YEARS there has been a gradual shift away from leftist parties which have held sway across the Latin American region for the greater part of the last 20 years. In their national elections, countries such as Chile and Argentina elected presidents who are to the right of the political centre, while countries like Colombia and Ecuador have also recently elected presidents closer to the centre than their left-leaning predecessors. There is a variety of reasons for this shift, but the central theme has been that government spending in many countries had ramped up to unsustainable levels and change was needed.

BRAZIL’S PRECARIOUS DEFICIT

Regrettably, Venezuela, the country most in need of a change in government, remains ruled by the same clique responsible for its evolution from the wealthiest country in Latin America (in GDP per capita terms) to a socioeconomic basket case. Venezuela’s descent is unprecedented for a non-war nation in Latin America and seems to be interminable as more and more refugees depart for neighbouring countries, fleeing the effects of a perfect storm of policy weakness, corruption, housing and food shortages, and hyperinflation. Estimates of an exodus of four million people out of a population of 32 million indicate the scale of the humanitarian crisis at hand.

STRONG-ARM TACTICS BY REGIONAL HEAVYWEIGHTS

With the above in mind, 2018 served up two very interesting elections in the region’s two biggest economies – Mexico and Brazil. First up in Mexico was far-left Andrés Manuel López Obrador, known to most by his initials ‘AMLO’, having lost the previous two elections to Felipe Calderón (2006) and Enrique Peña Nieto (2012). In the case of his defeat to Calderón in 2006, the margin was so narrow (35.9% for Calderón to 32.3% for AMLO) that he proclaimed himself the ‘legitimate’ president after alleging electoral fraud in favour of Calderón. Mexico’s election tribunal ultimately ruled against these allegations, but the perceived lack of legitimacy took its toll on Calderón’s presidency.

In 2018, there was no doubt about the election result – AMLO won an absolute majority of votes and beat his nearest challenger by over 30%. The result was greeted with some fear by the market, given the new president’s historic aversion to market-based solutions to economic problems. Obrador has railed against neoliberalism and has been very critical of the energy sector reforms introduced by his predecessor that ended the monopoly of state-owned oil producer, Pemex. These reforms were necessitated by years of declining infrastructure investment and a drop in output from 3.5 million barrels per day (bpd) in 2004 to under two million bpd in 2017, with a corresponding impact on Mexico’s fiscus. Should these reforms be reversed, and if the new government acts on its promise to freeze energy prices, the fiscal situation in Mexico could deteriorate rapidly.

The experience with fuel subsidies in other countries (such as Indonesia) suggests that freezing fuel prices benefits the middle classes far more than the poor and is rarely good policy, as it diverts scarce state resources away from investment. Another worrisome early action was an informal referendum called by AMLO shortly after winning the presidential election (that was not carried out by the official electoral authority). The referendum, that was held prior to AMLO's inauguration. After a large majority of those who took part voted against the new airport, he announced he would respect the vote outcome despite the negligible turnout of one million voters in a country of 130 million people and despite the new airport being one-third built and with billions of dollars in financing having already been raised.

The direction of Mexico under AMLO will be important during his tenure. His six-year term will have at least two years of overlap with Donald Trump’s presidency and the US President’s historical animosity toward migrants from Mexico (and those from elsewhere who use Mexico as their transit route to the US) looks set to have a substantial impact on their relationship. AMLO has been characterised by Western media as a “fiscally responsible populist” which, if accurate, suggests that Mexico should muddle along for his six-year term. This is better than a Venezuela-style implosion but does not suggest that Mexicans will experience a sustained improvement in their living standards either.

FROM PEAK TO TROUGH

From an investment perspective, the bigger impact on the emerging markets universe will be made by the election in Brazil. The country has been under left-wing PT (the Workers’ Party) rule since Lula da Silva’s election in 2002 through to the removal of his successor Dilma Rousseff (who, like Lula, also won two consecutive presidential elections) via impeachment in 2016. The early years of PT government went well, largely sustained by the commodity boom, as Brazil is a big exporter of iron ore and agricultural products. The country rebounded very quickly from the 2008/2009 Global Financial Crisis (GFC) and looked set to finally break its historical reputation as being the perennial ‘country of tomorrow’.

Alas, the foundations of Brazil’s growth under the PT government were quite poor – heavily reliant on consumer spending, unsustainable minimum wage increases, fiscal largesse and the commodities boom. There was also substantial corruption in Petrobras, the state-owned oil company that had been used to enrich many politicians and businessmen through rigged contracts and outright bribery.

The boom years also saw Brazil’s currency appreciate significantly against its trading basket, which made manufactured exports uncompetitive and imports much cheaper. Brazil therefore maintained historical tariff and non-tariff barriers while the rest of the world was reducing these, further eroding international competitiveness. The deterioration in the fiscal situation eventually led to a hard landing in 2015 and 2016 when a combination of an economic contraction of 7% and double-digit inflation plunged the country into its most severe recession on record. The currency also depreciated by 85% against the dollar over the one-year period from September 2014 to record lows since the introduction of the Real in 1994, an event that brought an end to persistent hyperinflation.

Despite having just been re-elected in 2014, public opinion moved rapidly against then-president Dilma Rousseff as the economy continued to deteriorate. This leading to her eventual impeachment by Brazil’s Congress and Senate on charges of breaching Brazil’s budget laws. Vice President Michel Temer served the remainder of her four-year term, achieving very little during those two years due to corruption allegations against him. This hindered his ability to attain Congressional support for some of the tough reforms that Brazil needs to enact to deal with its perilous fiscal position and very burdensome regulations that retard economic growth.

The 2018 election therefore came down to a showdown between left and right. Da Silva intended to run again as the constitution imposes a two-term limit for consecutive elections, but after sitting out at least one cycle a former president is free to run again. Unfortunately for him, he was jailed earlier in the year for corruption and, after losing several appeals, he was declared ineligible to stand. His party nominated Fernando Haddad, a former Mayor of São Paolo, as its candidate. With centrist parties failing to gain traction, Haddad came up against Jair Bolsonaro, a Congressman for close to 30 years. Bolsonaro has been described in the media as Brazil’s Donald Trump, due to his tendency to make provocative and unconventional statements. He has spoken fondly about Brazil’s time under military rule (he served in the military before entering Congress) and denigrated certain groups of people based on his staunch religious views.

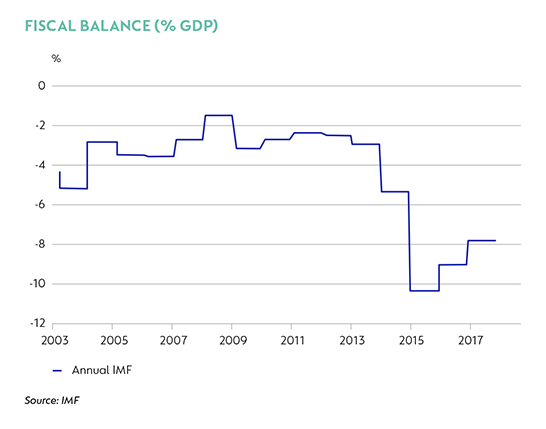

With the Brazilian electorate very angry with the PT party for its failings under Messrs. Da Silva and Rousseff, it was almost inevitable that whatever the shortcomings of the alternatives, the leading non-PT candidate would win. That eventually came to pass, as Bolsonaro won comfortably in the second round of the election by around 10 percentage points. The scale of the task awaiting his administration is daunting – Brazil runs a budget deficit that has exceeded 5% of GDP for each of the last four years. Government debt to GDP is now in excess of 70% and continues to rise. With close to double-digit interest rates and a poor credit rating, Brazil must spend 6% of GDP just servicing the interest on its debt. Brazil’s generous pension and social security system allows many public employees to retire in their fifties (with a life expectancy of 75 years) and spending on these benefits consumes over half the federal budget. Without drastic entitlement reform, it will be impossible to get Brazil into a sustainable fiscal situation. Bolsonaro lacks a majority in Congress to force through reforms without cross-party backing, so there is potential for continued deadlock and the fiscal situation to spiral further out of control.

Because of these challenges, the administration put in place by Bolsonaro is very important. Early indications are that good technocrats will be placed in charge of key administrations and that the incoming government is committed to cutting red tape and making Brazil an easier country to do business with.

There are many attractive domestic industries in Brazil that we believe have good investment opportunities. The fragmented nature of the higher education sector, the clothing and food retail sectors and the healthcare industry overall provides an opportunity for market leaders and entrepreneurial management teams to deliver high returns for shareholders over the medium to long term.

Our Global Emerging Markets strategy continues to identify and research these potential investment ideas to complement the existing 12% of the strategy that is currently invested in Brazil. After several tough years, valuations in Brazil remain very attractive in a variety of businesses, even relative to the overall global emerging markets universe after its decline last year.

This article is for informational purposes and should not be taken as a recommendation to purchase any individual securities. The companies mentioned herein may currently be held in Coronation managed strategies, however, Coronation closely monitors its positions and may make changes to investment strategies at any time. If a company’s underlying fundamentals or valuation measures change, Coronation will re-evaluate its position and may sell part or all of its position. There is no guarantee that, should market conditions repeat, the abovementioned companies will perform in the same way in the future. There is no guarantee that the opinions expressed herein will be valid beyond the date of this presentation. There can be no assurance that a strategy will continue to hold the same position in companies described herein.

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter