United States - Institutional

United States - Institutional

Investment views

There is still opportunity out there

Long-term thinking and rigorous research needed to spot opportunities.

The Quick Take

- Despite the negative news flow, South African equities offer some attractive opportunities today

- Finding these opportunities requires skilful analysis of business fundamentals and searching for attractive valuations

- We believe there are companies with growth opportunities, strong cash flow generation and appealing fair values

- These companies often move against the tide, and the pharmacy group Dis-Chem is a good example

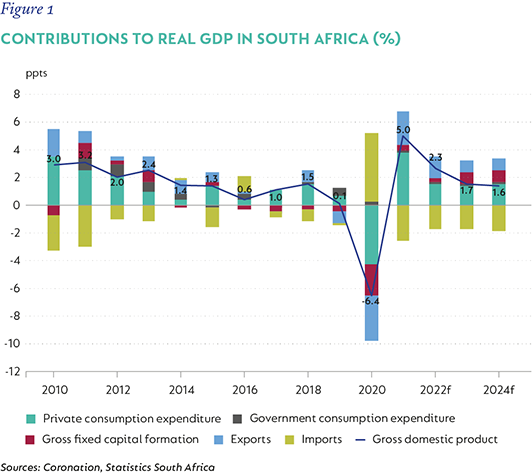

IT MAY SOUND surprising to hear that we are finding appealing investment opportunities in South Africa. After all, it has been a painful decade for the country. The graph below (Figure 1) not only paints a thousand words, but also shows the degradation of domestic economic growth in the form of “death by a thousand cuts”.

Like many other countries, South Africa’s post-pandemic recovery will take place with pre-existing growth impediments and a much-elevated national debt burden. A nascent recovery will also have to navigate new developments and risks such as higher global inflation, decarbonisation trends and a move to an increasingly digital world. If this was difficult to do before, it will now be an even harder task to undertake.

STAYING FOCUSED ON INVESTMENT PRINCIPLES

But, by focusing on a few investment principles, we think there are still some attractive prospects to be found. These principles include:

- Looking for businesses with growth opportunities:

In a sluggish economy, it is difficult for overall industries or sectors to show meaningful growth. But, within these sectors, there are usually winners and losers. Individual businesses in a sector can “win” by taking market share from weaker or more poorly positioned incumbents. These winning businesses are not always apparent. Usually, they are the businesses moving against the tide – those investing heavily in expansion or efficiencies now, often to the detriment of near-term earnings. Their long-term goal, however, is to increase their share of the market pie. - Identifying businesses with strong cash flow generation:

In the South African space, our preference is to invest in high-quality companies that are high cash flow converters and have solid balance sheets. These businesses have the necessary resources to keep investing in their operations to build scale, operate efficiently and improve their product and service offerings to clients. Their financial strength also means they are less vulnerable to the economic impact of negative events. - Identifying businesses that are mispriced when compared to our assessment of their intrinsic valuations:

Many domestic facing companies have fragile macroeconomic outcomes priced in. As a result, many shares look cheap. Cheap shares don’t always make good investments, though. At Coronation, our investment process looks at the normal earnings power of a business over a sufficiently long-term time horizon. This will capture the effects of an economic cycle and any other external impacts on our valuation. Our resultant fair values are often flexed to understand how companies will perform under different scenarios. The outcome of this is a robust fair value that allows us to identify shares that trade at attractive prices relative to their intrinsic valuations. It also gives us the conviction to take portfolio positions when we think the market is pricing in either a too harsh or a too optimistic outlook.

DIS-CHEM: LOOKING ATTRACTIVE

The above principles provide a good framework for our team to think about potential investment opportunities that can be represented in our portfolios. An example of a current portfolio holding that we think fits these general criteria is Dis-Chem.

Dis-Chem operates in the resilient pharmacy sector that can do well even in a constrained South African economy. The overall defensive nature of healthcare spending results in healthy like for like sales growth in the industry.

In addition, there is still a significant opportunity for the formalisation of the pharmacy sector in South Africa. In many other developed markets, corporate pharmacies usually have the majority share of the industry. In South Africa, Clicks and Dis-Chem have a market share of around 50% of the sector, with the rest made up of small independent pharmacies. The combination of organic sales growth and market share gain opportunity supports long-term real revenue growth forecasts for Dis-Chem.

Since IPO, the Dis-Chem management team have invested heavily in their business. They have built new distribution capacity, invested in new retail and operating systems, rolled out new stores and more recently bought businesses in adjacent categories like baby and primary healthcare. These investments have dented short term earnings and margins (and has been one of the key reasons behind the de-rating in the share price post IPO). We believe that these investments have been for the long-term benefit of the business as they strengthen the operating efficiency and support the growth potential of the business.

Strong cash flow generation

One of the by-products of these investments is that the cash flow generation of operations has improved considerably. Pre-IPO, the business had a historic three-year free cash flow conversion ratio of 19%. This means that 19% of the business’s earnings were converted into free cash to either pay down debt, make acquisitions or increase shareholder returns. Clicks, Dis-Chem’s nearest comparable peer, had a three-year free cash flow conversion of over 100% at that time. Dis-Chem’s potential to increase its cash flow generation was clear to us.

Dis-Chem’s investments into a more efficient supply chain and systems since IPO have indeed paid off. They have allowed the business to unlock working capital investment and release significant cash. The current three-year historic free cash flow conversion ratio of the business is north of 100%.

Attractive valuation

Dis-Chem trades on a rather full 1-year PE multiple of 25 times. However, we think near term earnings are understated, partly due to the impact of the investments listed above, as well as the more recent impact of Covid-19 on the business. As these impacts move out of the base, we expect the business’s robust revenue delivery to translate into strong earnings growth while maintaining high cash flow generation characteristics. As such, we see the 1-year PE multiple unwinding to a very reasonable 11 times over our investment horizon.

THERE ARE ALWAYS OPPORTUNITIES OUT THERE

Investing in our local South African companies will not be simple, given the many challenges our economy faces. It is easy to label domestic facing businesses as un-investable and thus ignore the investment set right on our doorstep. But there are some interesting investment opportunities in this space if you focus on businesses with good fundamentals that trade at appealing valuations. Our long-term thinking and rigorous research process allow us to spot these opportunities and give us the patience to wait for our investment thesis to emerge, thereby generating healthy portfolio returns for the benefit of our clients.+

Disclaimer

SA retail readers

SA institutional readers

Global (ex-US) readers

US readers

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter