South Africa - Institutional

South Africa - Institutional

Factfile: Coronation Global Managed - January 2017

INCEPTION DATE

1 November 2009

PORTFOLIO MANAGERS

Louis Stassen is a founding member of Coronation and a former CIO, with 27 years’ investment experience. He heads up Coronation’s global developed markets investment unit. Neil Padoa is a portfolio manager and head of global developed markets research. He joined Coronation in May 2012 and has 9 years’ investment experience.

OVERVIEW

A selection of our best investment ideas from around the world. Coronation Global Managed invests in a wide range of global asset classes, regions and currencies – with the primary objective of maximising long-term investment returns (over rolling five-year periods and longer). At the same time, it seeks to take on less risk than the equity market and to avoid any permanent capital loss. In addition, the strategy aims to outperform a composite benchmark: 60% MSCI All Country World USD Index (a broad measure of global equity market performance) and 40% Bloomberg Barclays Global Aggregate Bond Index (a performance measure for global fixed income markets).

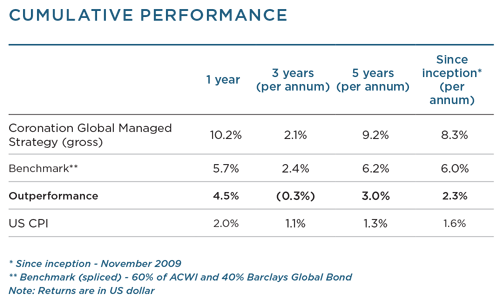

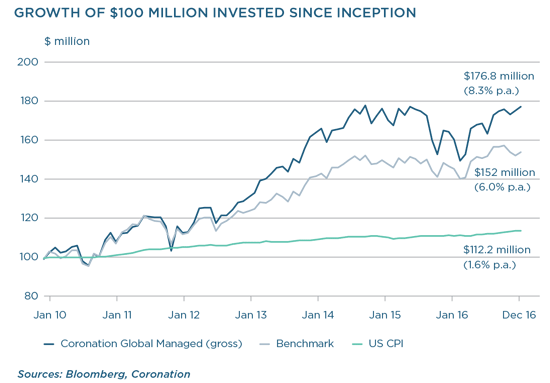

Over the past five years the strategy has delivered an annualised return of 9.2%, outperforming its benchmark by 3% per year (gross of fees). Since its inception in November 2009, it has delivered a return of 8.3% per annum.

ABOUT THE STRATEGY

Coronation Global Managed is an actively managed, global multi-asset class strategy. It is managed according to the same investment philosophy we have used within SA for more than two decades – a tried and tested approach that has enabled us to successfully manage multi-asset class mandates for the past 23 years. Today, multi-asset class mandates represent over 50% of the assets we manage on behalf of SA investors.

One of Coronation’s key advantages is our generalist approach – both in our use of different asset classes to structure our investments and within our investment team. Bucking the global trend towards specialist mandates 20 years ago, Coronation has consistently maintained material assets in multi-asset class strategies. This has given us invaluable experience in managing these strategies through materially changing environments. In addition, we have avoided silos in our investment team. Rather, our integrated global team comprises well-rounded generalist investment professionals with the expertise to evaluate investment opportunities across sectors, asset classes and geographies.

As such, we are now uniquely positioned in how we manage multi-asset class mandates, making the Coronation Global Managed portfolio fairly unique in the international market. Generally, managers tend to offer either specialist asset class building blocks or balanced mandates with formulaic asset allocation, where different building blocks are managed by different managers. In our view a building block route holds the potential to take on unintended views and risks within the portfolio, and ultimately results in poorer risk management. We believe that an integrated, bottom-up approach to asset allocation and security selection results in a more optimal solution for investors.

HOW WE MANAGE THE STRATEGY

At Coronation, we construct robust, antifragile portfolios of our highest-conviction investment ideas. This results from an intense focus on proprietary investment research, across geographies, sectors and instruments. Based on this research – and our assessments of long-term risk-adjusted returns – we construct our portfolios from the bottom up. We do not use systematic or mechanistic measures to determine asset class allocations or rebalance our portfolios. Rather, we make active decisions on individual security selections, asset allocation and risk management on an ongoing basis.

The asset allocation decision is therefore no different to any other investment decision, and could be effected through derivatives or individual security positions (depending on market conditions, liquidity and risk-adjusted opportunity, risk allocations are increased in cheap markets, while capital is protected by reducing allocations in expensive markets).

ASSET ALLOCATION

Given its long-term growth-orientated mandate, Coronation Global Managed is managed with a high allocation to risk-seeking assets. This includes a maximum exposure of 75% to equity (with emerging market equities being capped at 30% within the 75%) and high exposure to listed property. According to our bottom-up selection process, we evaluate all investment opportunities to identify assets trading at material discounts to their underlying long-term value. We also believe that interaction with management is an integral part of our analysis of a company.

With our asset allocation modelling having shown the value of listed property within a balanced mandate, we consider the asset class an important building block in the strategy. We evaluate listed property investments relative to opportunities within the fixed interest space, and as much as 12% of the strategy has been allocated to property since its inception. Current exposure is around 8%.

Within fixed interest, we currently favour credit over government bonds. We maintain our negative view on bonds given an anticipated uptick in inflationary pressures. In addition, we have a strong preference for credit instruments from issuers we are more familiar with, either due to a link to the SA market or our knowledge of a particular industry. Current exposures include Investec, Old Mutual and MTN.

Finally, the cash component of the strategy (a residual component, once all tactical allocations have been made) is actively managed. Given the current anaemic returns being generated by the asset class, we are aware of the temptation to invest cash in higher-risk instruments. However, we view cash as a risk-balancing component within the portfolio, and manage our investments within tight risk constraints. This ensures that we do not raise the strategy’s risk profile and maintain liquidity at all times.

A recent introduction to our investment mix has been merger arbitrage opportunities: investing in companies for which corporate transactions are pending. This exposure may constitute up to 10% of the strategy if we believe that the risk/reward trade-off falls in our favour. A case in point is our current investment in US pharmacy Rite Aid, for which the drugstore chain Walgreens has made a bid. In our view the transaction will offer significant value, and it presented an attractive risk/reward profile as the market was initially cynical of its approval by the Federal Trade Commission.

RISK MANAGEMENT

We apply robust risk management measures when selecting instruments for inclusion in the portfolio, as well as in the sizing of these various instruments (depending on their expected risk-adjusted returns). In addition, we apply hedging when deemed necessary to protect against downside risk. Once again, this is always an active decision, implemented when deemed appropriate by the portfolio managers, and not a mechanistic rule irrespective of market conditions.

OUTLOOK

Uncertainty continues to prevail worldwide. This is both political (in the wake of Brexit, Donald Trump’s election as US president, and rising nativism and populism globally) and economic (particularly around the impact of interest rate normalisation). As such, we maintain a more cautious stance towards equities, and the strategy’s current equity exposure is around 60% (in line with the benchmark weighting). Significant positions include our holdings in the alternative asset manager space in the US and a recent allocation to global consumer staples.

We maintain conviction in the longer-term performance prospects of our alternative asset manager stocks. After detracting from performance for some time, these stocks rerated post Trump’s election on prospects of improved economic growth – and the opportunities this would present for the managers to generate compelling returns for clients. However, we are mindful of noises around a tax overhaul under the Trump administration. While this would increase the attractiveness of US companies poised to benefit from corporate and individual tax reductions (and would therefore create greater investment opportunity), there is also talk of a potential increase in the effective tax rate for the private equity industry. This would have a negative impact on this sector, and we are closely monitoring developments.

Having previously found little value in traditional consumer staples (fast-moving consumer goods such as food, beverages, tobacco and household goods), the fund now has a total exposure of 8%. In the recent past, investors have tended towards overweight positions in this sector as a proxy for the bond market, where yields remained under pressure. However, Trump’s election precipitated a significant sell-off in response to greater bond issuance and improved bond rates. This presented an opportunity for the fund to invest in high-quality consumer staple stocks at attractive valuations.

Due to our concerns around an uptick in global bond levels (which have seen a marked correction already, and are likely to correct further) we currently hold no bonds with interest rate risk exposure. In addition, we have hedged out the interest rate risk associated with our credit counters. Within listed property, our major exposure (roughly two-thirds) remains to the UK market, which sold off as a result of uncertainty around Brexit. The dramatic price adjustment and prevailing price weakness have provided long-term investors with a unique opportunity to buy strong and well-located assets at attractive prices.

Finally, the year ahead will once again hold heightened political risk – in particular, the potential for negative surprise outcomes from upcoming European elections in Germany, France and the Netherlands. While unexpected macropolitical events may contribute to market volatility, we will continue to emphasise our bottom-up selection process. We carefully consider appropriate position sizes and asset allocation weightings within the strategy to ensure a robust portfolio with the ability to deliver on its mandate, despite the outcomes of uncertain macro-events. We do not chase share prices or constantly react to the most immediate newsflow, and where we identify value we are willing to sacrifice short-term returns in pursuit of compelling long-term client outcomes. Often, the portfolio actions that cause short-term pain (buying dramatically undervalued assets while prices are still falling, or selling overvalued assets while prices are still rising) are also those that deliver the most compelling long-term results.