South Africa - Institutional

South Africa - Institutional

Investment views

Cross-border ecommerce set to disrupt the market

The Quick Take

- Low-cost, cross-border Chinese ecommerce platforms are gaining traction in developed markets

- In spite of their growing success, they face significant ESG-related headwinds

- Quality management teams are key to the success and sustainability of these businesses

- Where they compete directly, we remain confident that competitors in our current portfolios can withstand the threat

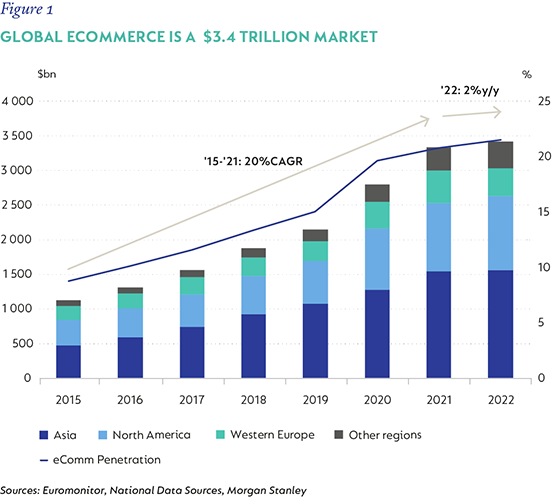

The Covid pandemic provided a perfect backdrop for the ecommerce industry, as much of the global population was in lockdown and looked to online shopping as an alternative. Global ecommerce grew by 30.6% in 2020 and penetration (ecommerce as a percentage of potential retail revenue) rose by 4.6% to 19.7%, up from 15.1% in 2019. While ecommerce growth has returned to the pre-Covid trendline, a subsector of low-cost, cross-border Chinese platforms, such as Shein and Temu, has continued to grow rapidly. Their ultra-low prices of up to 80% lower than those offered by Amazon are proving to be very attractive to consumers in the current inflationary environment. Shein is an online fast fashion retailer that is looking to list in the US later this year and Temu, selling a wide variety of products, was launched last September by the already listed PDD Holdings, which we own in the Coronation Global Emerging Markets Equity Strategy. Figure 1 shows Morgan Stanley’s estimated regional ecommerce growth as a percentage and US dollar value.

SHEIN

Shein is a pure online apparel retailer that grew revenues by a factor of 450 times over the last 10 years, from $50 million in 2012 to $22.7 billion in 2022. With this 80%+ compound annual growth rate, it is now one of the largest fashion retailers globally (Figure 2). Founded in Nanjing in 2008, China by Chris Xu, Shein is unique in that it only sells in international markets, with Xu capitalising on the opportunity to leverage China’s low-cost supply chain into developed economies with high purchasing power.

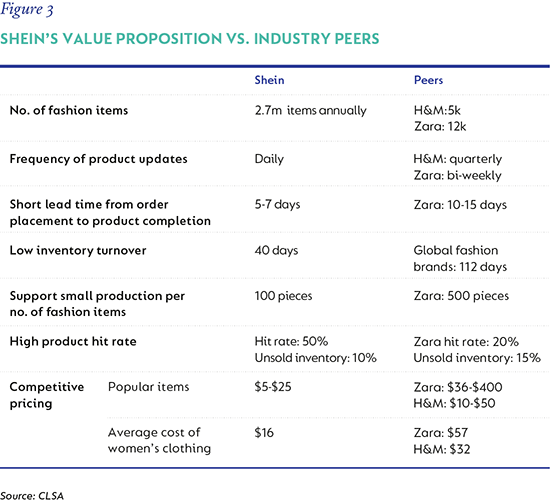

While low price is a key selling point, Figure 3 shows that Shein’s real moat lies in its digitalised operations, which enable it to release 2.7 million fashion items annually, which amounts to more than 7 000 items per day. This digital efficiency also achieves a short lead time (from order to complete product) of five to seven days, and a fast inventory turnover of 40 days. These metrics are significantly better than industry peers and have enabled Shein to respond to the latest fashion trends more swiftly and at lower costs. While delivery takes between eight and 14 days, the option of a free return within 30 days ensures a good shopping experience. Shein’s return rate is lower than the industry average, suggesting higher levels of consumer satisfaction.

DIGITALISED OPERATIONS

This operational excellence is achieved through the digitisation of its entire operation, from digital and social media marketing to data-driven product design, and digital management of its suppliers.

Xu founded the business using search engine optimisation and went on to acquire experience in digital and social media marketing, which is a key customer acquisition driver for pure online retailers such as Shein. The company has been leveraging influencers since 2011 and has partnered with some of the most relevant Gen-Z influencers, such as TikToker Addison Rae and rapper Lil Nas X, and has an industry leading web performance and social media presence. Shein has also successfully managed to channel most users to its app, which has a richer user experience and generates complex data sets. The latter supports deeper customer understanding and enables customised product offerings to individual users. In the US, its biggest market, it was the most downloaded shopping app in 2022, narrowly beating Amazon.

Shein acquires accurate demand insights and designs through online data analysis and offline buyers, rather than relying solely on offline buyer insights, which is the industry norm. Methods include tracking fashion trends by using Google Trends Finder and capturing clothing data on popular colours, prices and patterns from various retail sites. Product design is very much data driven, allowing Shein to respond much faster to the latest fashion trends, thus improving its chances of designing popular products.

With around 300-400 core suppliers and over 1 000 clothing suppliers in Guangzhou, orders are dispatched via software, and suppliers are monitored and judged on four key performance areas, including timeliness of procurement and delivery, the product defect rate and the success rate of a new product. The assessment is supported by data collected from its digital platform, and the worst underperformers are removed each quarter. This ensures the quality of its products and prompt delivery within specified timelines to customers. Suppliers are happy to work with Shein as it adds large stable volumes and provides reliable settlement on a monthly basis, or on a weekly basis, when requested by highly rated suppliers. This improves the suppliers’ business stability, operational efficiency and cash conversion, which is often very poor in the clothing industry.

DISTRIBUTION AND LOGISTICS

Logistics is a critical component for Shein’s business model, as all products are shipped directly from China, thousands of kilometres away from the end consumer. For standard delivery, which takes 12-14 days, Shein charges $4 for freight and offers free shipping for orders above $49. It is estimated that shipping costs $8-$10 per order, so Shein is subsidising 50% to 100% of the freight costs. All products are sent to Shein’s domestic warehouse by local suppliers. Customer orders are then transported by air freight to Shein’s overseas warehouses, with the last mile fulfilled by local post offices or third-party logistics companies. For express deliveries, Shein charges $13 for orders below $99 (otherwise free), products are delivered by international logistics companies, such as DHL and FedEx, from Shein’s China warehouses directly to consumers. This shortens delivery time to 8-10 days.

TEMU

Temu is a newcomer to the cross-border ecommerce space, with a focus on low prices across a wide range of consumer products. It was launched in September 2022 in the US by PDD Holdings, the third largest ecommerce player in China, which hosts over 10 million merchants on its platform and with $18 billion in net cash on its balance sheet. It is bolstered by a strong management team that grew domestic revenue by 63 times over the past five years, and will be able to provide strong financial and operational support to ensure Temu’s success in the international markets.

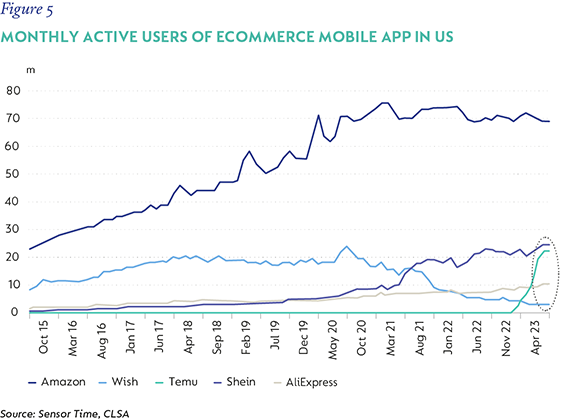

Temu has executed its strategy extremely well, surpassing Shein to become the number 1 downloaded shopping app in the US in 2023, with monthly active users on par with Shein after only seven months (Figure 5). Outside of the US, Temu has quickly entered eight other developed markets and is now the top downloaded shopping app in each of them.

EXECUTION A KEY TO SUCCESS

Temu has a wider category exposure than Shein, with apparel and household goods accounting for 42% and 24% of the mix, respectively, versus Shein’s 80% and 20%, respectively. The remaining 34% with respect to Temu’s mix is comprised of maternity, electronics, appliances, and other products. This is due to Temu using a hybrid model in which goods are provided by third-party merchants on a consignment basis, while Temu provides all the consumer facing operations, such as price setting, logistics and aftersales services. This model ensures that Temu can offer a wide selection of products to consumers, at the lowest prices through a bidding process, while ensuring product quality through stringent quality checks and merchant assessments. Consumer facing operations, such as delivery and return services, are key to repeat purchases and the sustainability of the model. Many earlier players, such as Wish.com, failed due to their inability to provide quality assurance for goods and services provided by the third-party merchants selling on their platforms.

Still in its nascent stage, Temu is currently loss-making due to heavy marketing and logistics investments to gain scale. Its parent company PDD Holdings, went through a similar strategy in China between 2017 and 2020, where its net income margin averaged -36% and it lost a cumulative $3.6 billion. This was the result of marketing spend that averaged 85% of revenue. Over the last two years, after amassing more than 800 million users, PDD reduced marketing expenses to 45% of revenue and generated a 24% net margin in 2022. Temu will likely go through a similar process, and the proven viability of the business model by its parent provides greater confidence as to its sustainability.

CONCERNS ABOUT THE CROSS-BORDER ECOMMERCE BUSINESS MODEL

Import tax on cross-border ecommerce: A number of countries have import duty exemptions for express delivered goods under a certain threshold, such as the US’s De Minimis exemption for orders below $800. Both Shein and Temu have been the beneficiaries of this tax benefit. The challenge is that many markets, such as the EU, the US, and Brazil, have removed, or are in the process of removing, this tax loophole, which will make Shein’s and Temu’s products less price competitive. Given their hefty discounts, a 20% import tax would not significantly erode their price advantage. However, in more extreme cases, such as Brazil’s 60% duty on express delivered goods, the impact would be material. To mitigate this, Shein has committed to establishing local manufacturing capacity in order to bypass import taxes and ensure that it remains competitive. But this will not fully solve the issue, as local manufacturing is unlikely to be as cost competitive as it is in China.

Environmental impact of fast fashion: According to the UN Environmental Programme, the fast fashion industry is the second largest consumer of water and is responsible for 8%-10% of global carbon emissions. The industry has seen a significant increase in apparel consumption, with the average consumer buying 60% more items of clothing and keeping them for half as long compared to 15 years ago. The trend is still on the rise and, according to the UN Framework Convention on Climate Change, emissions from textile manufacturing is projected to increase by 60% by 2030. Given Shein’s incredibly low prices and huge numbers of new items introduced each day, it has made purchasing new clothing easier and more affordable than ever, which will contribute to the industry’s growing environmental impact.

Environmental impact of cross-border ecommerce: A study by the MIT Center for Transportation & Logistics shows that ecommerce’s carbon footprint is 17% lower than brick and mortar retail, with parcel delivery significantly more carbon efficient than customer transport; but this is partly offset by higher packaging usage. However, the air freight used by Shein and Temu for the cross-border transportation is 144 times more carbon intensive than sea freight, making the overall environmental impact of the business model much higher than traditional retail.

FUTURE OUTLOOK, IMPACT ON AMAZON AND OUR EMERGING MARKET HOLDINGS

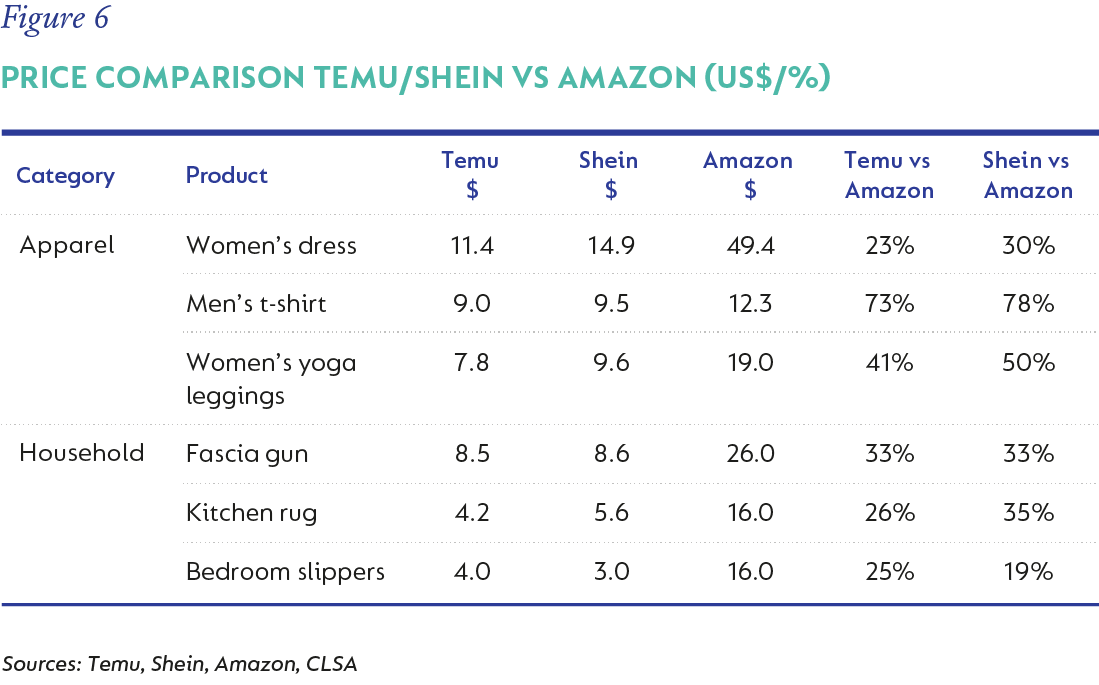

Both Temu’s and Shein’s products are significantly cheaper than Amazon’s (Figure 6). Given the prevailing inflationary environment, both platforms are likely to do well as consumers trade down and become more likely to look out for a bargain.

While Shein and Temu are growing fast, their gross merchandise values (GMV) of $29 billion and less than $1 billion, respectively, in 2022 are tiny compared to Amazon’s more than $600 billion GMV. Apparel and accessories account for 17% of Amazon’s GMV in the US and, while it would be negatively impacted by Shein, the main threat Shein poses is to other apparel retailers. Amazon’s prime members are accustomed to two-day deliveries, and are thus less likely to tolerate the 8-14 day delivery offered by the upstarts.

Currently, given their large discounts, Shein and Temu provide an attractive alternative for price-sensitive consumers. However, Temu could pose a significant threat to Amazon, as we’ve seen in the Chinese ecommerce market. There, Pinduoduo grew to be the third largest ecommerce player, with its price lead strategy succeeding at the expense of the leader, Alibaba, whose ecommerce market share declined from around 75% in 2017 to less than 45% in 2023.

Shein’s growing presence in Southeast Asia, India, and Latin America will have a negative impact on our holdings such as MercadoLibre, Shopee and Lojas Renner.

Shopee and MercadoLibre have 25% and 7% respective exposure to the Brazilian fashion market and will be negatively affected by Shein’s growth. However, the biggest impact will be on Lojas Renner, the largest clothing retailer in Brazil. That being said, while we are cognisant of the risk, we remain positive on Lojas Renner. This confidence is based on the fragmented nature of the Brazilian apparel market and the consequent opportunity to take market share from weaker players via its well-executed omnichannel strategy that combines the strength of brick and mortar and ecommerce models.

Temu’s near-term focus is on developed markets, so it is not in direct competition with our emerging market holdings at present. We hold its parent company, PDD Holdings, which will benefit from its growth – we estimate that Temu contributes 14% to PDD’s fair value.

OVERCOMING THE CHALLENGES

The environmental impact of fast fashion and cross-border ecommerce, and the social impact on local retail employment all pose significant challenges to this business model. Additionally, given the geopolitical tension between China and the West, they could face political hurdles accessing the developed markets in the future. However, while it won’t be smooth sailing, the management teams of both companies are capable executors and will likely be able to navigate through the choppy waters.

Disclaimer

SA retail readers

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter