South Africa - Institutional

South Africa - Institutional

Investment views

South African economic outlook

Good intentions and a renewed commitment to growth are not enough to make government's financial position sustainable

- Procuring and distributing a Covid-19 vaccine are crucial; supply deficit weighs

- SA's fiscal position was already critical going into the pandemic

- Increased confidence is the elixir for boosting growth; government policy action is a key factor too

- Global growth and China recovery should provide a welcome tailwind; debt a drag

THE MOST IMMEDIATE challenge facing South Africa is to effectively manage the Covid-19 pandemic crisis. The country’s path to recovery will be dictated by its ability to vaccinate enough people to restore mobility and open sectors that are currently restricted. News on this front is sobering. South Africa has not been able to procure a large enough vaccine pipeline to adequately inoculate most of the population. Under the COVAX initiative, we have a commitment to receive enough vaccine to cover 20% of the population as supply becomes available.

In addition to this, government has managed to expedite an additional 1.5 million doses of the Oxford University-AstraZeneca vaccine for frontline workers, which is due in January and February. Beyond this, the outlook is uncertain. Gross global supply has been allocated, and South Africa cannot procure additional doses through bilateral agreements with producers unless it is at the expense of another country. Expanding supply is difficult and will take time, although it is likely that many vaccines currently under development may prove effective and become regulated in the coming months.

Expert opinion is that we will land enough vaccines to cover about 10% of the population by the end of the year, starting in April in variable lots. This implies that the population will still face additional waves of infection throughout the year, with the next likely to hit during the vulnerable winter months. Even though the ANC’s National Executive Committee has mercifully ruled out another hard lockdown, this still exposes the economy to varying and ongoing degrees of restriction, with a potentially devastating impact on the vulnerable services sector and the fiscus.

The failure to have adequate pipeline supply and a credible rollout strategy in place poses a serious and prolonged risk to the economy. Some hope comes from the mobilisation of considerable private sector resources to administer vaccines, but supply remains a constraint. While encouraging areas of economic resilience emerged at the end of 2020, and global tailwinds are potential sources of upside support for growth, domestic health and containment risks are firmly to the downside.

A PRÉCIS OF THE YEAR IN REAR VIEW

The Covid-19 crisis came at a bad time for South Africa. Growth in 2019 was just 0.1%, and in the first quarter of 2020 (Q1-20), the economy was already in recession, deeply constrained by inadequate electricity supply, as well as a range of operational and organisational challenges at Eskom.

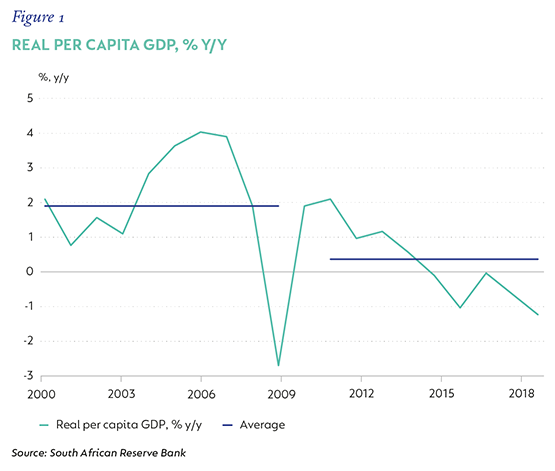

The unemployment rate was 29.1%, and the employment rate had fallen in annual terms in the second half of 2019 (H2-19). Per capita real GDP had declined every year since 2015 and was -1.3% lower in 2019 than in 2018.

Combined, these factors have undermined business and consumer confidence. Companies and households have had limited ability to invest and spend in a weak economy. Both economic and political constraints have also compromised their willingness to do so. Weak economic policy delivery (‘over promise’ fatigue) and uncertainty related to critical aspects of the economy’s regulatory framework combined to render very weak investment activity and associated low productivity.

When the pandemic hit and government implemented an early and hard lockdown, compliance was good, and there was a general support for the initiative. The central bank acted swiftly, cutting the repo rate cumulatively by 300 basis points (bps), reducing borrowing costs to the lowest level since the 1960s and, after some stalling, intervened to ensure financial stability and the smooth functioning of the money and rates markets, with regulatory support for the banks.

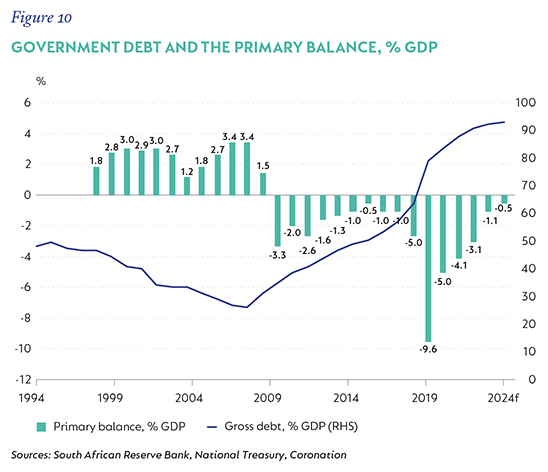

The National Treasury, already constrained by a weak fiscal position, tabled an Amendment Budget in June. The total relief package was billed at R500 billion, but R130 billion was reprioritised from the Budget. Adding this to an anticipated loss in revenue implied a deficit of -14.6% of GDP, with debt likely to step up 18.3 percentage points (ppts) of GDP, from 63.5% to 81.8%, and is expected to rise further over the medium term.

Playing in the background of the economic crisis, the ebb and flow of factional politics continued in 2020. There were notable successes at the reinforced National Prosecuting Agency, but this was tempered by the ruling party’s failure to credibly address corruption and restore confidence. Ongoing delays in the implementation of economic strategies, such as the release of spectrum, remained sources of frustration and criticism.

Attempts to address both the capacity of the State and to get things done, nonetheless, had some successes as the economic crisis helped focus political attention on reviving the economy and the government’s financial position. Despite this, ongoing fiscal support for insolvent State-owned enterprises (SOEs) remained a critical and contentious drain on limited resources.

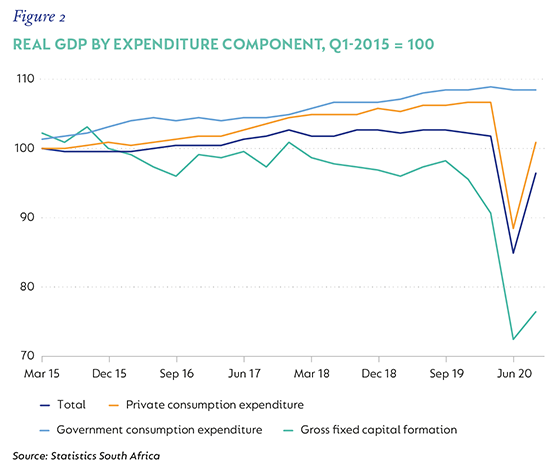

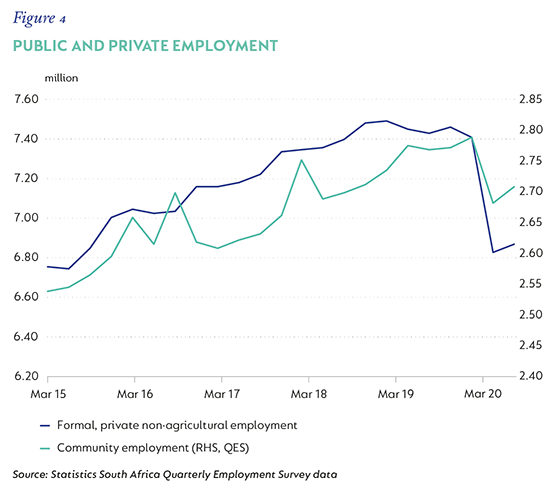

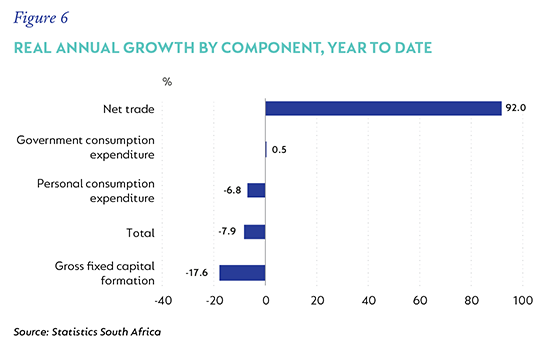

The lockdown in Q2-20 saw GDP collapse by 51.7% quarter on quarter (q/q) seasonally adjusted and annualised (-17.5% year on year [y/y]), with 2.2 million associated job losses. This was the biggest loss of output in South Africa’s recorded GDP history. But the Q3-20 recovery in activity was much better than expected, with GDP rebounding 66.1% q/q, seasonally adjusted average, and accompanied by a partial recovery in employment.

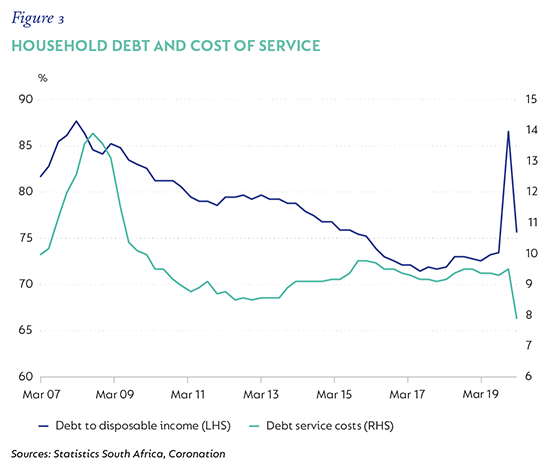

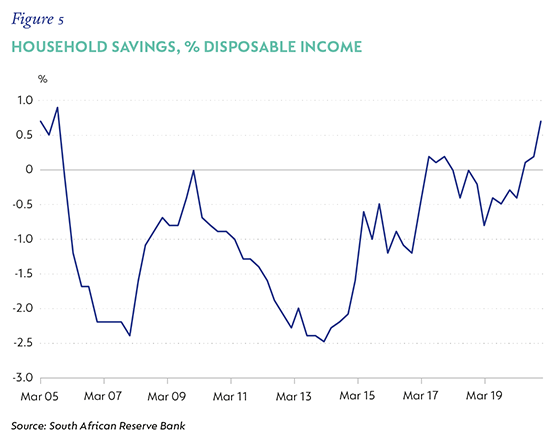

A closer look at the real economy showed some recovery in incomes and stronger household balance sheets, as well as corporate profits. Household real net disposable income recovered from a fall of 15.7% y/y to -3.9% y/y. The household debt burden reduced to 75.7% of disposable income, from a spike to 86.5% in Q2-20 and an average level of 73% in 2019. Importantly, debt servicing costs benefited from materially lower interest rates and, at 7.5% of disposable income, is at a multi-decade low. Credit availability remains good, but is constrained by the limited appetite for additional debt. Household savings rose, with both the inability to spend and rising precaution contributing to the increase. Given the improvement in key household metrics, with growth momentum into Q4-20, we forecast a collapse in real GDP in 2020 of -7.2%.

2021: A MIXED BAG OF OPPORTUNITY AND RISK, THREATENED BY THE FAMILIAR PATH OF POLICY COMPROMISE

Against this weak but improving economic backdrop, the outlook for 2021 hangs in the balance between domestic economic resilience underpinning domestic demand and a combination of the impact of the second wave and the risk posed by existing areas of weakness, including weak policy implementation, electricity constraints, poor public sector capacity and a fragile fiscal foundation. Global recovery factors also count, with the possibility that these may provide a significant tailwind to the South African economy. Government’s growth strategy and commitment to fiscal sustainability – with critical focus on actual implementation – will dictate the shape of the economic outcome.

WEAK VACCINE STRATEGY

The most immediate obstacle to recovery is a currently weak vaccine strategy. Some news of additional vaccine procurement is positive but inadequate. Importantly, government is not expected to implement another economically damaging hard lockdown, but a combination of partial restrictions, ongoing uncertainty and slow vaccine progress will continue to weigh heavily on the services sector, particularly tourism and recreation, with a likely increase in long-term scarring. Foreign tourism will also not recover until South Africa is deemed a safe destination with respect to Covid-19.

OUTLOOK FOR GROWTH RECOVERY

Looking at the drivers of expenditure-side GDP growth, a recovery in consumption expenditure has mixed potential. Private consumption expenditure (PCE) accounts for about 60% of GDP and, in Q3-20, contributed 43.8ppts to the surging recovery. PCE is driven by a combination of employment growth, real income growth, and the availability of credit and consumer confidence – people’s ability and willingness to spend.

After the sharp fall in employment, there has been only a partial recovery, and formal employment is still 6.3% below the pre-crisis level. Although marginal, President Ramaphosa’s Employment Stimulus Programme update in November detailed good progress on this front too.

Incomes remain constrained but also experienced a strong recovery in the third quarter as mobility constraints eased. Net disposable income is down -3.2% year to date in nominal terms – after a 13.6% y/y collapse in Q2-20 – while total compensation is down 1.6%, including the Q3-20 recovery, after falling 7.2% in Q2-20.

In real terms, these are down -6.3% and -4.8%, respectively, year to date, but with solid positive momentum. For households that derive a significant proportion of their income/wealth from financial assets, the loss of dividend income has hurt, but the positive financial market performance should provide a fillip.

Savings balances (which represent residual cash) have surged. Measured as a proportion of disposable income, savings were 0.7%, the highest since early 2005. This is likely a reflection of a combination of an inability to spend and greater precautions taken. But it also creates the potential for a recovery in spending, while low interest rates and reasonably healthy balance sheets provide the opportunity for stronger credit growth as incomes and confidence improve.

We forecast a modest increase in disposable income as employment in hard-hit sectors, such as manufacturing, construction and parts of business services, improves. We see little prospect yet for increased employment in the trade sectors, and this remains a drag. With a forecast of real income growth of 1%, and a small contribution from increased credit utilisation, ongoing low interest rates and some improvement in confidence, we forecast real growth in private consumption of 2.7% in 2021, and 2.5% in 2022.

There is a more positive tilt to the outlook for gross fixed capital formation; but, again, pandemic, regulatory and capacity constraints persist. Private sector investment may get a fillip from the expansion of renewables within the new energy framework, and investment in machinery and equipment could be supported by ongoing adjustments to working from home. However, with profitability under pressure and poor prospects for State-funded investment, we expect gross fixed capital formation to remain weak and detract from growth momentum in the year ahead. Visible progress in reducing the constraint the State places on the economy by engaging more with the private sector has the potential to boost confidence – the magic ingredient for growth.

Net trade was a considerable tailwind for growth in Q3-20, contributing an annualised 38.3ppts to the recovery. Both mining and manufacturing export volumes recovered strongly from the hard stop of Q2-20, and agricultural exports contributed further. While terms of trade remain elevated and domestic demand – notably investment – remains depressed, the recovery in global growth and trade volumes should provide a welcome tailwind to growth into 2021. There is also further potential uplift for export value from a recovering China.

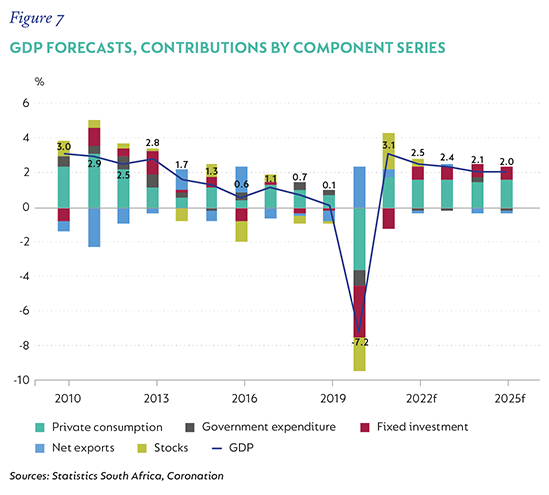

We expect the economy to grow 3.1% in 2021, with uncertain lockdown restrictions a considerable downside risk, while income recovery and net trade should provide a meaningful fillip. This is a below-consensus forecast. Our forecasts assume that capital expenditure will remain a drag on growth in the year ahead, although a more meaningful implementation of energy-related investment could see this number improve. Massive inventory drawdowns were a significant detractor from growth in 2020; a more modest drawdown in 2021 will add positively to growth momentum. We do not assume – given power constraints – any meaningful inventory accumulation over the forecast period.

Importantly, this recovery profile does not see GDP levels return to pre-pandemic levels until 2023.

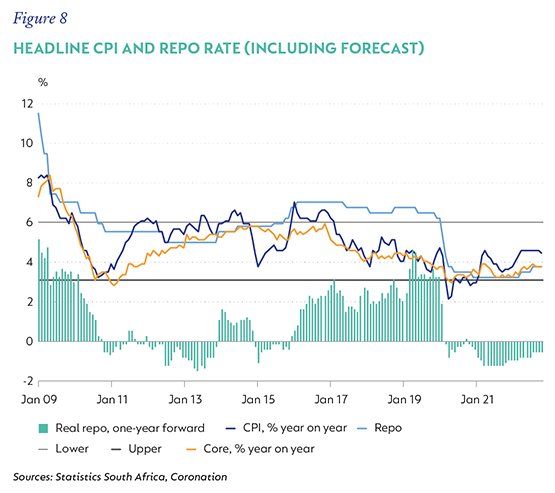

This weak recovery implies that the output gap will remain negative, with little demand-related inflation pressure expected to emerge. Overall headline CPI is forecast to remain below the central point of the South African Reserve Bank’s (SARB) target range in 2021 and 2022, before rising above it in 2023. We expect monetary policy to remain accommodative and see room for the SARB to cut the repo rate again to 3.25% in early 2021, as growth falters once more. At current levels, policy rates are at levels not seen since the late 1960s.

FINANCIAL DEFICIT A HEAVY DRAG

Government finances were the biggest casualty of last year’s crisis and remained a significant source of domestic economic fragility. Of course, better growth would go a long way to boosting revenues and improving the outlook, but South Africa’s fiscal weaknesses extend beyond this. There are three interrelated challenges:

- Weak and disappointing revenue growth, partly owing to weak nominal GDP growth and partly due to the collapse of the tax collection infrastructure. Over-estimating revenues upon which multi-year expenditure is allocated has led to a decade of persistently large deficits.

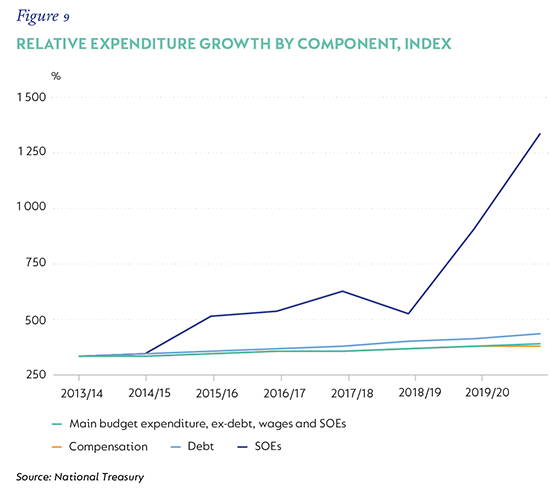

- The composition and size of expenditure, notably the public sector wage bill, and there-fore the rising debt service burden, must change. Decisions related to the size of government were taken as long ago as 2007/2008 when public-sector salary structures were expanded to protect and attract scarce skills in health and education. Several generous multi-year agreements, coupled with aggressive State employment growth, saw the consolidated public sector wage bill expand from 33% of expenditure to 36%. While efforts have been made to limit its expansion through headcount limitation, this has had little effect, as wage growth has outpaced both inflation and GDP growth.

- Ongoing decisions to bail out SOEs have undermined much of the fiscal discipline imposed elsewhere over the past five years. Since 2008/2009, Eskom, SAA, the SABC and the Land Bank combined have cost taxpayers R229 billion. This is no longer affordable.

These fiscal vulnerabilities are well known. Consecutive budgets, and finance ministers, have attempted to right-size the large expenditure commitments – especially the wage bill – but successive crises, mostly related to SOEs, amidst very weak growth, have systematically worsened an already weak position.

The December ruling in favour of the National Treasury in its dispute with public sector unions over the suspension of the final year of its wage agreement in 2019/2020 will go a long way to improve the starting position for right-sizing wages within expenditure. Assuming the full R38 billion is saved, the consolidated public sector compensation budget should return to 33% of expenditure in 2020/2021. While this is clearly a ‘win’ for the National Treasury, much still hinges on the forthcoming wage agreement and the wider government backing of a painful consolidation plan.

Even with some consolidation in our numbers, fiscal metrics remain very weak. With a modest improvement in GDP growth, a slightly more robust rate of GDP inflation (boosted by terms of trade), gains in revenue somewhat ahead of initial expectations, and relatively contained expenditure, the main budget deficit is still set to be -14.3% of GDP in the current fiscal year. Excluding interest costs, this is still a primary deficit of -9.6% of GDP.

A recovery in revenues and improved GDP growth should see this narrow to -10.2% and -5% of GDP, respectively, in the coming year, assuming the new wage agreement limits annual increases to below inflation (we assume 3% nominal). But this deficit is large, and the fiscal adjustment required to push the deficit to a balance – or the surplus position required to stabilise debt dynamics – seems economically and politically unlikely. South Africa also does not enjoy the happy balance of nominal growth rates that exceed the average nominal cost of servicing government debt. In the absence of both, debt will continue to accumulate.

DEBT MANAGEMENT CRITICAL

Rising debt is economically costly; it lowers investment and productivity, and undermines growth through time. It also implies that as debt is accumulated, government is forced to issue more, not only to fund expenditure but also to pay off maturing debt in an endless cycle.

This reinforces the dynamics that compound the problem and may accelerate a crisis. Ultimately, this will become unsustainable. The IMF defines debt as sustainable when a government can meet all current and future payment obligations without exceptional financial assistance or going into default.

History tells us that sovereigns are poor at mitigating the risk of looming debt crises, and financial markets, in a world of extremely low global rates, may not impose adequate discipline early enough.

Our own economic history is littered with many sensible plans and good intentions, but, at best, extremely weak public policy execution. Even with the best intentions and a renewed commitment to a sensible growth strategy, the road to fiscal sustainability for South Africa is likely to remain very challenging.+

Disclaimer:

SA readers

Global (ex-US) readers

US readers

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter