South Africa - Personal

South Africa - Personal

PDD Holdings is the owner of online retailed Pinduoduo and cross-boarder ecommerce platform Temu.

During the quarter, PDD holdings (PDD) reported results that, under normal circumstances, would have been a cause for celebration. Revenue was up almost 90% year-on-year (yoy), with margin expansion leading to operating profit up 150% yoy. Free cash flow conversion also exceeded 100%. Yet negative comments by management about long-term profitability coming under pressure and the need to reduce take rates (commission on sales) to make the ecosystem more sustainable for merchants led to the share dropping by 40% in a short space of time, only to recoup most of the losses in the week before the end of the quarter to leave it only slightly down for Q3-24.

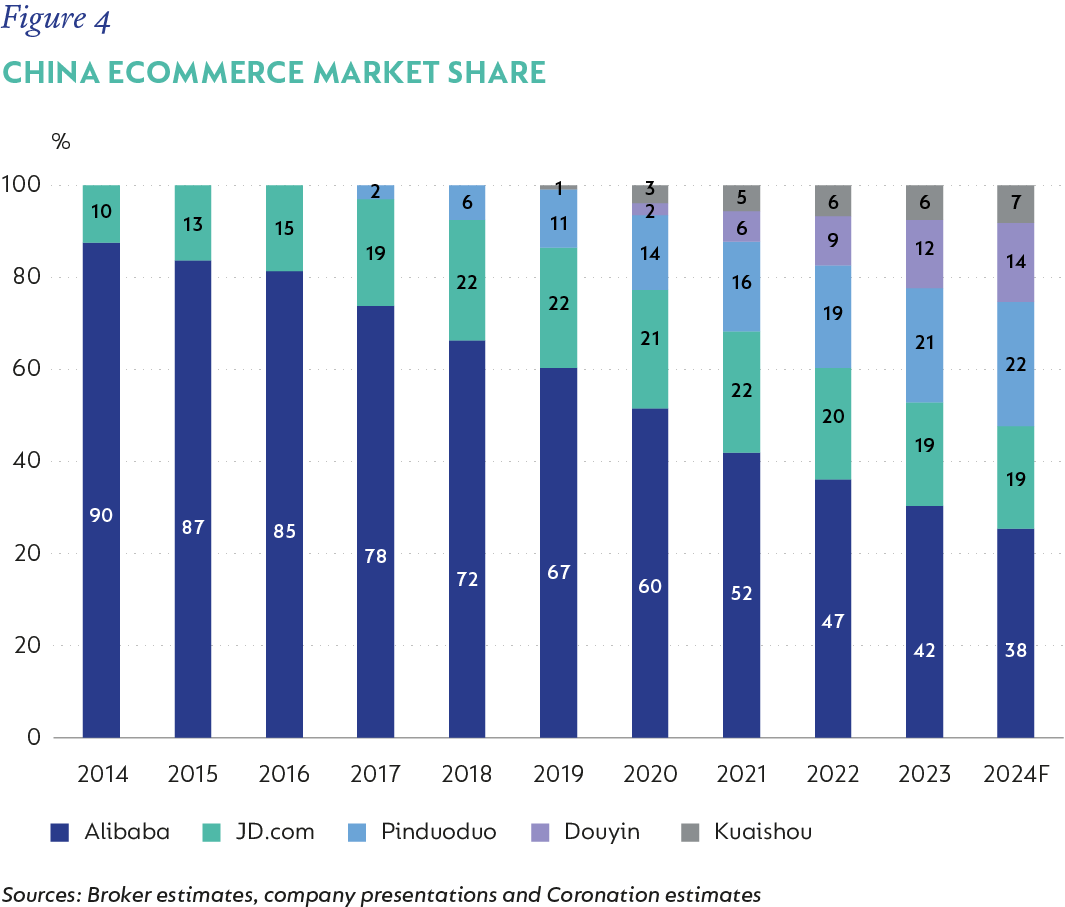

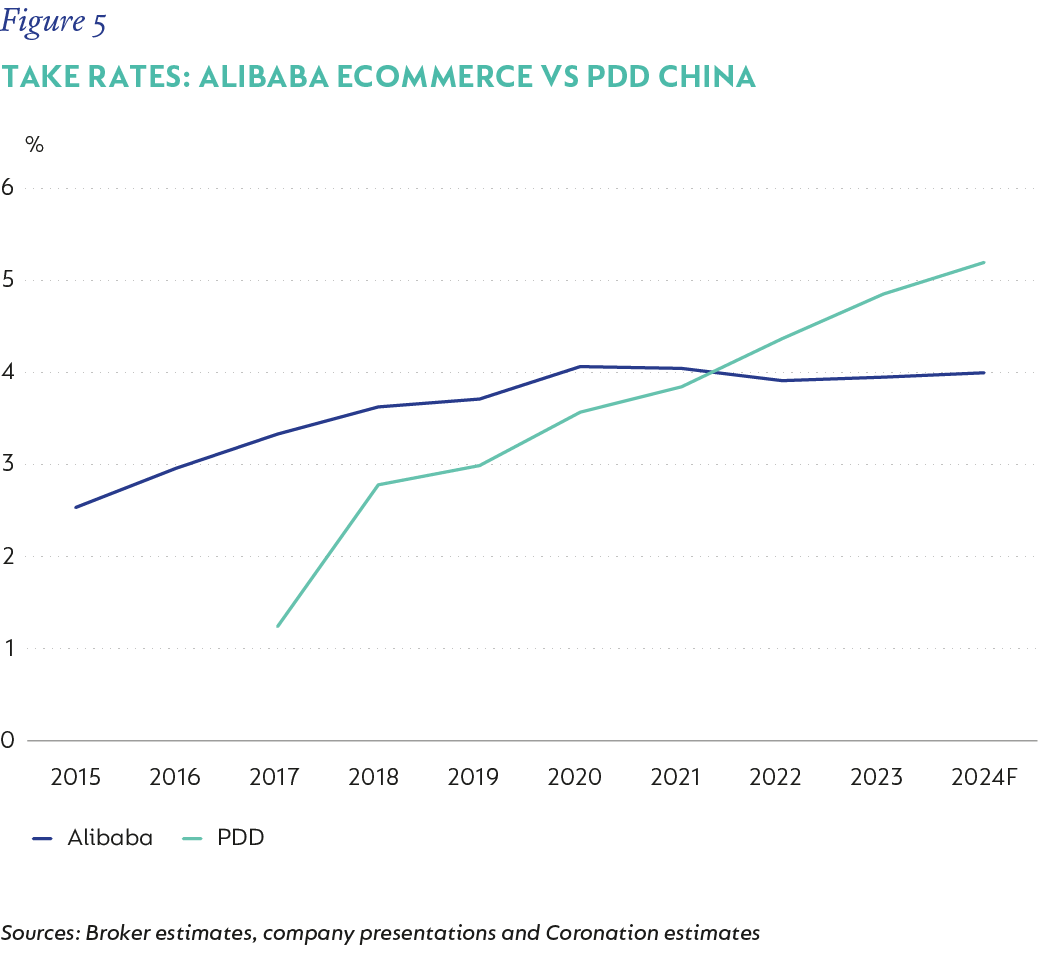

A key criticism of PDD is that the business is somewhat opaque, with little interaction with investors and the sell-side, and limited disclosures outside of the required operating metrics we find in results releases. These are valid criticisms, but we have done a lot of work to understand PDD’s culture, management style, incentives and moat around its business model, and believe that the reasoning has more to do with a desire not to assist competitors to counteract the threat PDD poses to them. This is why PDD has taken so much market share from Alibaba (in particular) over the years and why its take rates have been able to expand beyond that charged by Alibaba (see figures 4 and 5 below).

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter