Global (excl USA) - Institutional

Global (excl USA) - Institutional

Personal finance

Coronation Retirement Annuity: Tax Benefits, Access & How It Works

Summary

A retirement annuity (RA) is a simple, tax-efficient way for South Africans to save for retirement through unit trusts. Contributions are tax-deductible up to certain limits, and investment growth within the fund is exempt from local interest, dividends, and capital gains tax while invested. Access before retirement is very limited, which helps keep your savings focused on retirement.

WHAT IS A RETIREMENT ANNUITY (RA)?

A retirement annuity (RA) is a personal retirement savings vehicle that allows South Africans to invest for retirement in a tax-efficient way. An RA invests in unit trusts and offers tax benefits designed to help you grow your nest egg for retirement. If you’re self-employed, an RA can be used as a single solution to house all of your retirement contributions. If you work for an employer, it can be used to supplement your existing employer fund contributions.

WHAT ARE THE KEY BENEFITS OF A RETIREMENT ANNUITY?

An RA offers dual tax benefits that make it a popular way to build up capital that will benefit you in retirement.

- Tax-deductible contributions (up to certain limits)

RA contributions are tax deductible up to certain limits. For example, contributions can be deducted from taxable income up to 27.5% or R430,000* annually, whichever is lower. This means contributing to an RA can reduce your taxable income and your tax bill. - Tax-free growth while invested

Investment growth while invested in the RA is tax free. This allows compounding to work on the full gross return rather than the after-tax remainder.

- Built for long-term saving

Money in an RA is meant for retirement, and access before then is very limited, subject to the two-pot rules and guidelines.

HOW DOES A RETIREMENT ANNUITY WORK?

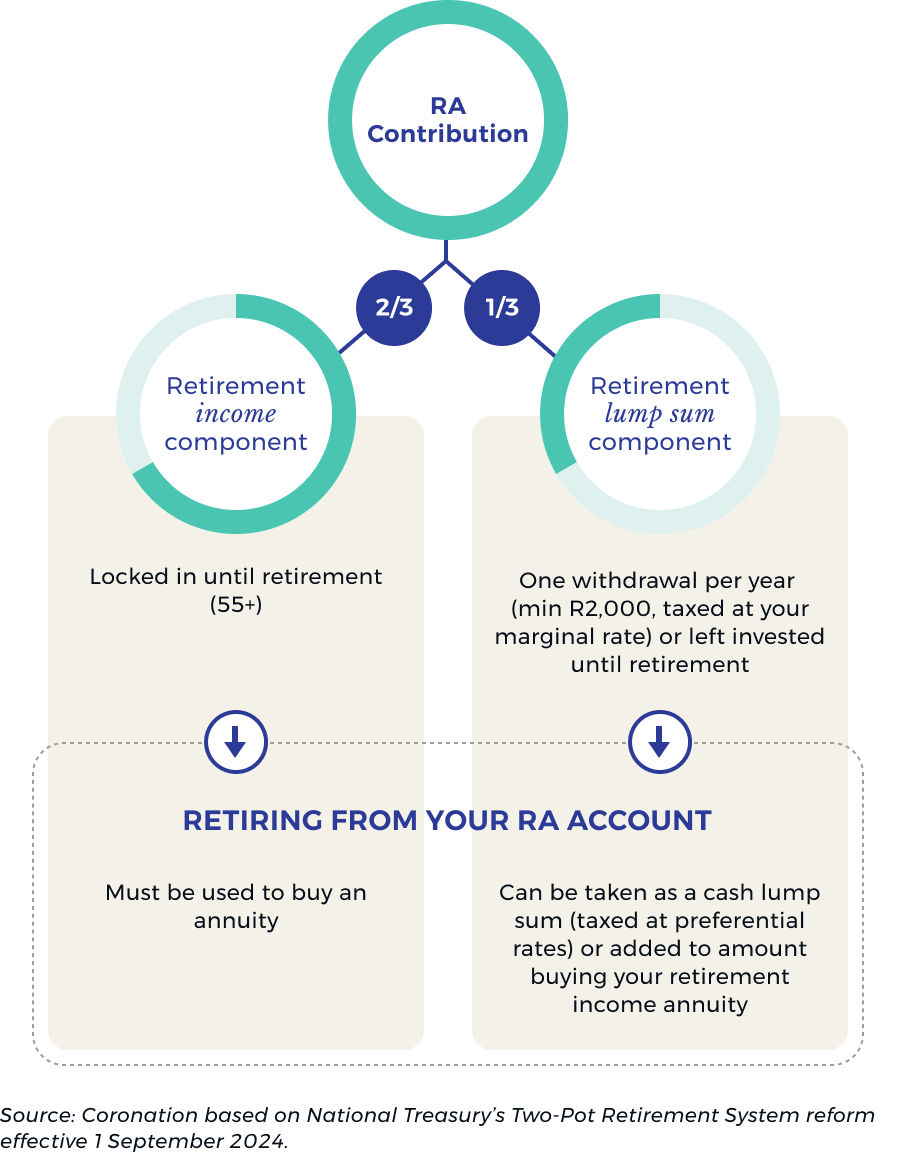

You can open a Coronation RA online. During the process, you select a suitable fund to power your retirement savings and decide how you want to contribute (lump sums, a regular debit order, or both). Once you start contributing, your money is split into two components, both invested in the same underlying fund/s:

- Two-thirds of each contribution is allocated to your Retirement Income Component (commonly referred to as your retirement pot).

- One-third is allocated to your Retirement Lump Sum Component (commonly referred to as your savings pot). This is the component you can access once per tax year before retirement, subject to a minimum withdrawal of R2,000.

Regulation 28 limits apply to the underlying investments

The underlying investments must comply with Regulation 28, currently limiting equity exposure to 75% and international exposure to 45% of the value of the investment.

Regulation 28 doesn’t stop you investing offshore in an RA — it simply places limits on how much of the portfolio can be invested in equities and internationally. This means your RA can still have offshore exposure, but within the prescribed caps. Read our Regulation 28 guide for more detail on how these limits work in practice.

WHEN YOU CAN ACCESS YOUR RA

- You can only access most of your savings at the age of 55, or earlier if you are permanently unable to work due to injury/illness.

- You may retire from the fund any time after age 55, or earlier if you are permanently disabled.

- You may make one withdrawal per tax year (minimum R2,000) from the Retirement Lump Sum Component, and you cannot access the Retirement Income Component before retirement.

What happens at retirement

At retirement, the rules differ by component: the full value of your Retirement Income Component must be used to purchase a post-retirement income, such as a Coronation Living Annuity. From your Retirement Lump Sum Component (savings pot), you may take the balance as a cash lump sum. If you have a vested component (contributions made before 1 September 2024), up to one-third of that value may be taken as a lump sum and the remainder must be annuitised. Note that if your total retirement interest does not exceed R360,000 (from 1 March 2026; previously R247,500), you may take the full proceeds as a lump sum instead of purchasing an annuity.

WHY CHOOSE CORONATION FOR YOUR RA?

Coronation's Retirement Annuity is a straightforward way to save for retirement through unit trusts with tax benefits.

- Flexible contributions

You can invest from as little as R500 per month, or make a lump sum deposit of R5,000 or more (R10,000 for the initial investment). You can also stop or restart contributions as your circumstances change.

- Transparent fees

Coronation doesn’t charge any initial, account, or administration fees, and your full investment goes into buying units in your chosen fund. Each fund has an annual management fee, and all fees are fully disclosed on each fund’s fact sheet and on Coronation’s website.

- A proven retirement-defining outcome

Coronation Balanced Plus gives retirement savers one simple, all-in-one solution. By combining different types of asset classes in a single portfolio, it’s designed to grow your money steadily over time.

GET THE MOST FROM YOUR RA WITH PROFESSIONAL ADVICE

An RA is a powerful long-term savings vehicle, but choosing the right fund, contribution level, and strategy depends on your individual circumstances. A qualified financial adviser can help you understand how an RA fits into your broader retirement plan, how to make the most of the available tax deductions, and how to structure your contributions as your life changes. Find out more about the importance of advice.

SEE WHAT YOUR CORONATION RA COULD HAVE DONE HISTORICALLY

An RA is built for long-term retirement saving: it offers tax benefits, tax-free growth while invested, and access rules that help keep your plan on track. If you want to see how consistent contributions could translate into a retirement outcome, use our calculator to explore historical results using the Coronation Balanced Plus Fund inside a Coronation RA.

*Effective from 1 March 2026

Frequently asked questions (FAQ)

- What is a Retirement Annuity (RA)?

A retirement annuity (RA) is a simple way for South African investors to save for retirement in their personal capacty. It is a designed to help you grow your nest egg for retirement, with specific tax benefits and limited access that helps keep savings focused on retirement. - Who is an RA suitable for?

If you’re self-employed, an RA can be used as a single solution to save for retirement. It can also be used to supplement your existing employer fund contributions. In short, it works both as a primary retirement savings vehicle and as an additional layer alongside other retirement funding. - How does a Retirement Annuity work?

You can open a Coronation RA online. When you contribute, your contribution is split into two components, both invested in the same underlying fund/s: two-thirds is allocated to your Retirement Income Component (retirement pot), preserved until retirement; and one-third is allocated to your Retirement Lump Sum Component (savings pot), which can be accessed once per tax year before retirement. - What is Regulation 28 and how does it affect an RA?

The underlying investments in an RA must comply with Regulation 28. These limits cap equity exposure at 75% and international exposure at 45% of the value of the investment. In practice, this means your RA’s underlying investments must stay within these regulatory limits. - When can I access money in my RA?

You can only access most of your savings at age 55, or earlier if you are permanently unable to work due to injury/illness. You may retire from the fund any time after age 55, or earlier if you are permanently disabled. - Can I withdraw from my RA before retirement?

Access before retirement is very limited and is subject to the two-pot rules and guidelines. You may make one withdrawal per tax year (minimum R2,000) from the Retirement Lump Sum Component (savings pot), but you cannot access the Retirement Income Component before retirement. - What happens to my RA at retirement?

At retirement, the rules differ by component. The full value of your Retirement Income Component (retirement pot) must be used to purchase an annuity — either a living annuity or a guaranteed life annuity from a registered insurer. Your Retirement Lump Sum Component (savings pot) may be taken as a cash lump sum. If you have a vested component, up to one-third may be taken as a lump sum. If your total retirement interest is below the de minimis threshold (R360,000 from 1 March 2026; previously R247,500), you may take the full amount as a lump sum.

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter