United States - Institutional

United States - Institutional

Economic views

South Africa

Passing breeze or real winds of change?

- The global recovery has materially improved SA’s near-term growth prospects through significant gains in terms of trade

- The enduring impact depends on how long the tailwinds last and how the reform agenda enables domestic investment

- Recent unrest is a setback. Lost activity, incomes and profitability may carry short- and long-term repercussions

- The fiscal position has improved relative to expectations, but we cannot afford to be careless; the SARB is likely to gradually normalise policy rates as the economy and inflation recover

THE GLOBAL RECOVERY is providing a significant tailwind to South Africa’s (SA’s) growth recovery. Specifically, the rise in the commodity prices of key exports has boosted domestic terms of trade (the amount we earn on our exports relative to what we pay for imports). The way in which this windfall reverberates through the economy, and how durable these gains can become, will depend on the duration of the boost and the economy’s ability to reinvest the gains. Once the terms of trade influences start to fade, it will be critical for the domestic reform agenda to have established an enabling environment for investment by easing regulatory constraints and boosting confidence.

The SA economy typically lags global cycles and usually needs a global trade tailwind to help kickstart a domestic recovery:

- An improvement in the terms of trade boosts domestic incomes through higher export earnings.

- The trade and current account improvement lifts growth and is usually accompanied by a stronger currency (and lower inflation).

- Higher nominal growth improves macro balances.

- The trade boost provides an opportunity to build on external momentum and reinforce domestic growth dynamics.

- Negatively, these dynamics tend to be temporary, and capacity constraints may limit the economy’s ability to capitalise. Ultimately, as the domestic economy recovers, domestic import demand pushes the current account back into deficit.

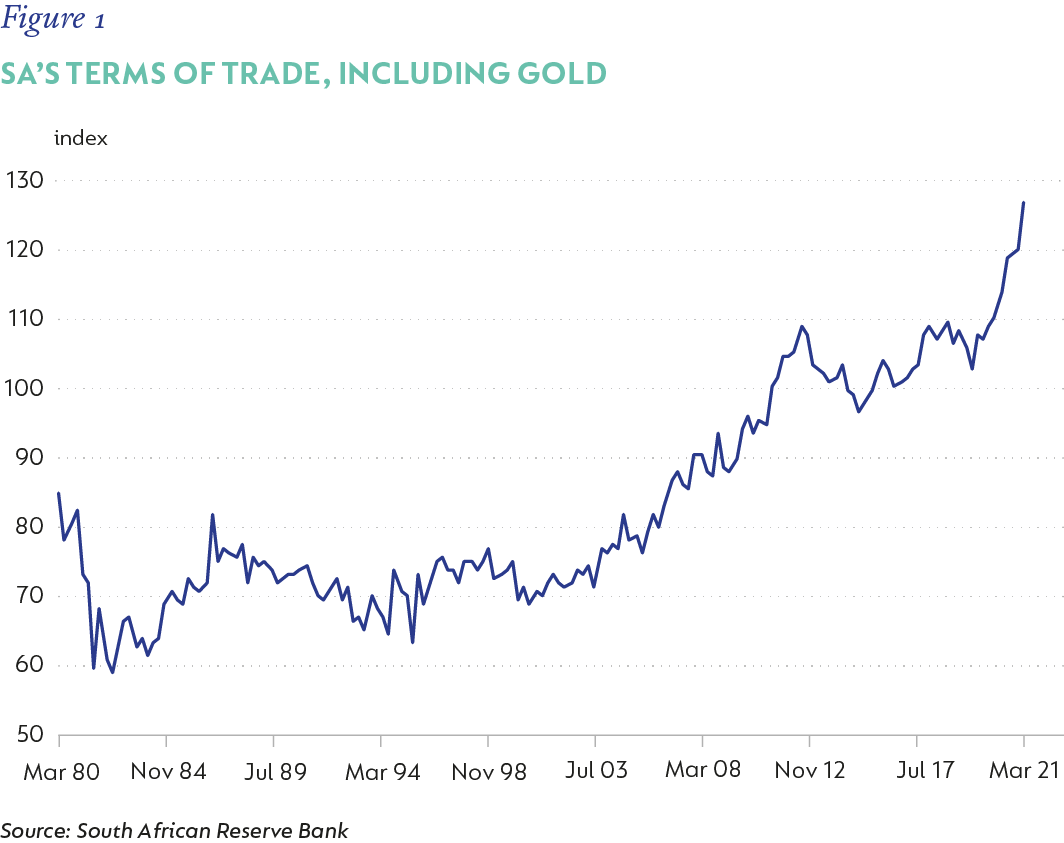

We are already seeing aspects of this sequence emerging. The current terms of trade shock is the biggest we’ve seen in over 40 years. Measured by the South African Reserve Bank (SARB), Figure 1 shows SA’s terms of trade index, including gold being up 10.4% over the past four quarters and 20% over the past two years. It is unlikely that such momentum will continue. Indeed, most forecasters expect commodity prices to retreat from here, but even accounting for the impact of the recent gain, we will see better economic outcomes.

First, the external balance has improved dramatically. In the first quarter (Q1-21), SA’s trade balance reached 8.1% of GDP – the largest since 1988 – and the overall current account posted a surplus of 5.0%. Available trade data for the second quarter (Q2-21) have seen two consecutive monthly record surpluses in April and May, suggesting that the positive tailwinds should blow into the second half of this year. We expect the current account to hold a surplus of about 2% through 2021, and to register a small deficit in 2022, as domestic growth and demand for imports improve.

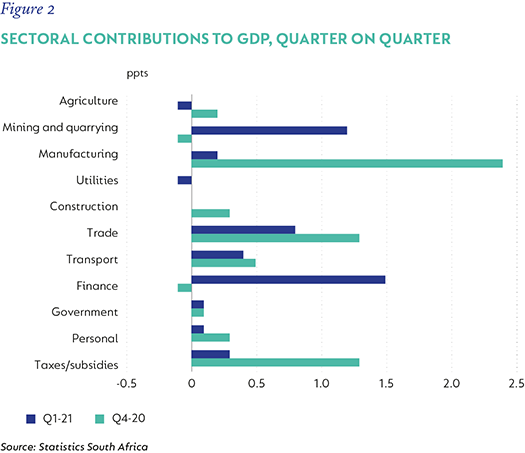

A closer look at the drivers of GDP shows that the trade influence on the supply side of the economy is also becoming clear. While most sectors saw growth ease a little compared to the fourth quarter of last year (Q4-20), it became better balanced – GDP growth slowed from 5.8% quarter on quarter (q/q), seasonally adjusted annualised (saa) to 4.6% q/q saa, but mining and quarrying output increased at a rate of 18.1% q/q saa in Q1-21 and contributed 1.2 percentage points (ppts) to headline GDP growth. Financial and business services benefited from the overall improvement in broader economic activity, and added 1.5ppts to growth. Transport, manufacturing and trade combined added the remaining 1.4ppts (see Figure 2 for more detail).

In addition to the impact on GDP growth, improving terms of trade have helped support both compensation and gross operating surplus. While the impact across sectors is lumpy – with parts of the services economy still constrained by the pandemic – there is a modest aggregate recovery in both key metrics, which should gain momentum. Both are important drivers of consumer spending and investment in the longer term.

The impact of recent unrest will disrupt some of these gains. Concentrated in the populous economic heartlands of KwaZulu-Natal and Gauteng, trade lost to looting, the destruction of infrastructure and frozen supply chains will have an impact on incomes, consumption and profitability. At the time of writing, efforts are being made to restore supply and to assess the overall costs. It is unclear how long the disruptions will continue; but the longer it continues, the greater the cost will be.

CYCLICAL OR STRUCTURAL?

We do not expect commodity prices to gain from here, but we also don’t expect a material rerating over the coming year or two. Global growth momentum is shifting from China and the US to Europe, and lagging emerging markets should see the recovery build over the next year as vaccine strategies mature. This means that terms of trade could remain elevated, presenting the opportunity for elements of this cyclical swing to become more permanent than transitory.

Importantly for GDP growth, we expect some recovery in household incomes, supported by normalising rates of compensation and boosted by non-salary and dividend contributions in the near term. Available data suggests a very uneven income recovery by income group, but initial gains should sustain households’ ability to spend.

Secondly, we think investment may start to contribute positively to growth. It is fair to argue that the economy’s ability to ‘catch’ the terms of trade tailwind is considerably less now than in the early 2000s, at the start of the last big commodity boom. At that time, SA’s currency entered the period very undervalued after the 2001/2002 crisis, and the economy was coming out of recession with ample electricity to accelerate growth in productive capacity, as well as well-functioning port and rail infrastructure – none of which is present now.

In contrast, we have suffered a prolonged period of weak growth, characterised by slowing investment, reluctant employers, depressed confidence and falling productivity. July’s unrest may materially undermine investment in affected areas specifically, and more generally, as confidence in the State’s ability to protect infrastructure and assets is shaken. Re-establishing authority to restore confidence is now even more critical.

History shows us that elevated terms of trade tend to have a lagged, but positive, impact on investment, which in turn has a positive impact on employment and productivity gains.

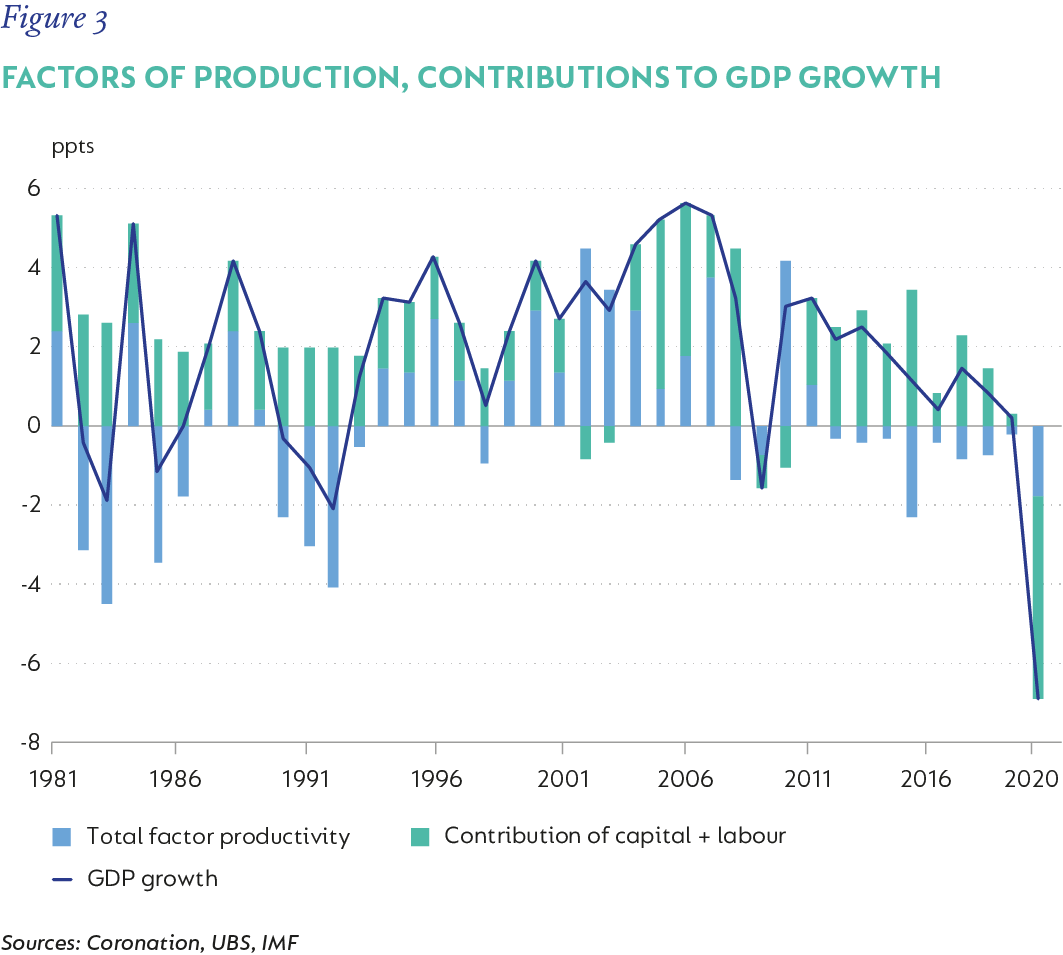

Figure 3 disaggregates GDP growth into the factors of production, namely labour accumulation relative to the inherent stock of labour, capital accumulation (investment) relative to existing capital stock and a residual, total factor productivity, which is the bit of GDP not explained by these other two dynamics. This is ‘magic sauce’ that enables economies to grow in excess of their factor endowment.

What is interesting and informative about this chart is that it shows that during the last commodity boom through the 2000s, the domestic economy enjoyed a protracted period of strong investment, job creation and a significant positive contribution to growth potential from associated productivity gains. It is also clear that in the intervening period, this has not been the case. For a range of reasons, as investment fell from 26.3% of GDP in 2008 to 15.0% in Q4-20, so too did employment and productivity.

Two critical issues in driving this deterioration were regulatory constraints on energy and other infrastructure, and the impact of politics and economics on business sentiment.

POLICY REFORM – ENERGISED AT LAST?

Reform progress is important and should still have a reinforcing impact on both. The most significant is the lifting of the embedded generation limit for private companies to 100 megawatts (MW), from 10MW.

This limit adjustment well exceeded the 50MW hoped for, and has been greeted very positively by industry and business alike. The change is still subject to the Minister of Mineral Resources and Energy, Gwede Mantashe, actually amending the enabling regulation, and uncertainty about what it means for companies with geographically separated entities that will need to ‘wheel’ electricity across the Eskom grid from one place to another.

The long period of energy insecurity means many companies have already invested in power generation capacity, which can be expanded quickly. In the mining sector, incremental investment is expected over 12 to 18 months. The change will not materially reduce the risk of loadshedding for an economy still broadly reliant on Eskom and its dickey fleet, but it will increasingly secure energy to the industrial sector, boosting both output and investment.

The other recent change is the ‘corporatisation’ of the Transnet National Ports Authority (TNPA). While this isn’t a new ‘regulatory’ change – it was embedded in the Ports Act in 2005 – the announcement that it is to be actioned is also significant.

It will allow the TNPA to have its own independent board, and for the entity to better allocate revenue to capital expenditure in a way it has been unable to do to date because of complex cross-subsidising within the entity. This should vastly improve transparency and port and transport efficiency, and enhance the capacity to upgrade infrastructure.

Taken together (but not limited to these two changes), actioning these reforms create the capacity for the economy to again see an incremental increase in investment and, with it, employment and productivity gains.

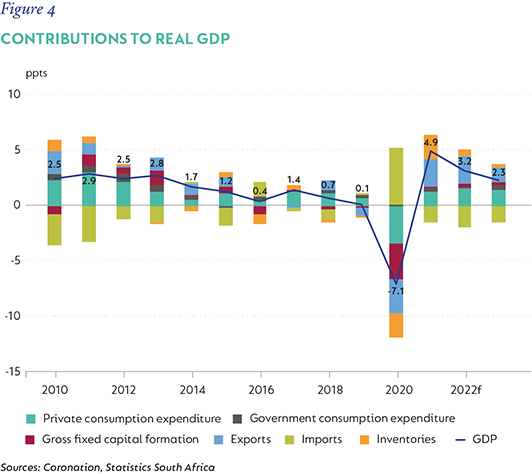

We forecast GDP growth of 4.9% in 2021 and a solid 3.2% in 2022, but acknowledge there is now some downside risk to these numbers. Nonetheless, we still think a larger contribution to growth from some areas of investment – albeit more a feature of next year’s growth outlook and into 2023 – will help buoy real GDP and assist better productivity outcomes than has been the case in the recent past. Figure 4 shows a history and our forecast of GDP contributors out to 2022.

NOMINAL MATTERS

Another important aspect of this recovery is what it means for nominal growth. Nominal growth is what drives revenues, and it has a meaningful impact on macro balances. The improved terms of trade and better growth prospects should see a material acceleration in nominal GDP growth, because changes in terms of trade reflect changes in the global prices for domestic goods, and they affect GDP inflation.

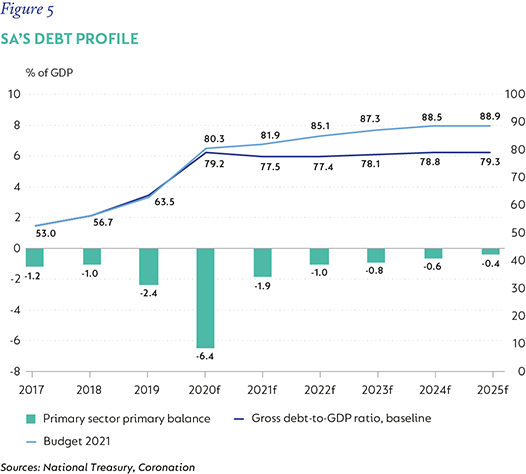

The first macro balance boost we have discussed already – the current account. However, SA’s critical macroeconomic vulnerability lies in its fragile fiscal balance. Following a long period of low growth and expenditure expansion, persistent deficits have led to a massive accumulation of debt, even before the pandemic hit. The rise in nominal GDP, coupled with improved corporate profitability, notably, but not only, from mining, materially improves the revenue outlook. We estimate that relative to the Budget 2021 baseline, the tax windfall should help to raise tax revenue almost 20% year on year (y/y) and reduce the deficit from -11.1% of GDP in 2020/2021 to -6.9% in 2021/2022 (Budget estimate: -9.0%).

Importantly for the debt dynamics, a combined improvement in nominal GDP growth relative to prevailing funding costs (the ‘r-g’ component of the debt equation), a reduction in the primary deficit from -6.4% of GDP to -2% in our forecast and the valuation effects of the stronger currency on foreign currency-denominated debt stock should help reduce the stock of debt from 79.2% in 2020/2021 to 77.5% in the current fiscal year. Thereafter, the moderation of these debt-stabilising factors in our baseline will see debt rise slowly towards 79.3% in 2025 (Figure 5).

While these fiscal improvements are welcome and, we believe, have aspects of permanence, it is critical to emphasise that they only make SA’s fiscal position ‘less weak’ than expected. Civil unrest has highlighted yet again the desperate economic circumstances of many and the need for ongoing social support. It has also cast the weak position of State security structures into stark relief. Additional funding for both seems likely. The unrest will also have an ultimate impact on taxpayers. This will be a difficult balance for the National Treasury.

The stock of debt, and debt accumulation dynamics, remain precarious and there is limited room to ease the planned consolidation or allocate expenditure carelessly. We believe that government can do more to enforce this improving dynamic, but acknowledge significant political challenges to the implementation of ongoing expenditure cuts. We are also worried that State-owned enterprises and municipalities will need additional financial support in the near term, too. We have made some allocation to this end in the baseline (which is why the debt dynamics remain adverse in the forecast), but this could prove to be too small.

WHAT DOES THIS MEAN FOR INFLATION AND POLICY RATES?

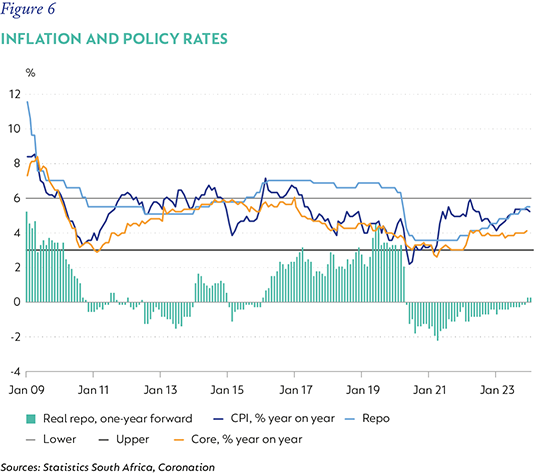

Here, SA is in a relatively strong position. Inflation, which has ticked up mostly on normalising base effects, has not seen uncontained increases in core components or large currency-related price increases as seen elsewhere. Headline inflation accelerated to 5.2% y/y in May as the peak base effect from the collapse in fuel prices in 2020 normalised, and is expected to rise again to 5.4% in July, as Eskom’s municipal tariff compounds a rise in food and fuel inflation. Excluding these components, core inflation remains well anchored at 3.1% – just above the bottom limit of the SARB’s headline inflation target band.

The SARB has been able to monitor domestic inflation with little consideration for global factors for some years now, but this may not always be the case. A key risk remains rising commodity prices – notably food – where global increases are already putting some pressure on domestic prices. Transport costs, broader input price pressure in the supply chain and the risk that similar ‘reopening’ bottlenecks emerge in the price of various services are possible here too. Unrest-related price increases are also likely to emerge, even if temporarily, over time. Rentals are a large component of the basket, and remain low for now, but pressure is more likely to build with time than moderate. Positively, the terms of trade boost and a large trade surplus have not only helped strengthen the rand, but should help mitigate some of the currency risk of changing global rate expectations and investor sentiment. The strong rand will also help keep goods price inflation low.

Figure 6 shows headline inflation’s ‘double peak’ in 2021 as prices respond to last year’s base and the implementation of fuel and electricity price hikes in July push inflation higher. Inflation crosscurrents, in our view, will see inflation drift higher over the next two years, but we see few visible risks of a large or persistent threat to the target at this time. Wage and currency pressure are contained by labour market slack and the current account surplus for now, and we think the central bank will start to slowly normalise interest rates in line with the recovering economy, rather than hiking aggressively in response to rising inflation risk.

IN CONCLUSION

The global tailwinds still provide a welcome boost to the domestic cyclical recovery. To make the lift more durable, the present time also offers a unique opportunity in which to capitalise on these circumstances after a prolonged period of weak growth, deteriorating macro balances and depressed sentiment. The pandemic has materially weakened the base off which this recovery needs to build, and it was weak to start with. July's unrest undoubtedly holds short- and long-term challenges for the domestic recovery, and came at a time when much needed momentum was just emerging. This means that policymakers need to act decisively and pragmatically so as not to waste the opportunity to help the economy grow and its people recover. +

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter