United States - Institutional

United States - Institutional

Economic views

South Africa’s inflation outlook remains challenging

The Quick Take

- Global inflation is cooling fast, yet central bankers are keeping a hawkish eye, as macro variables and region-specific factors continue to weigh, and core remains sticky

- SA’s inflation was more muted than elsewhere, but is proving stickier in an almost no growth environment

- We don’t expect any relief for borrowers in the near term, as the SARB will likely keep a tight rein on prices for longer

We expect domestic headline inflation to slow in coming months, but that a range of factors will limit the rate of disinflation, leading to higher inflation than markets expect and the need for restrictive policy settings, for longer. After some resilience at the start of this year, global inflation has fallen fast off its peak in the third quarter of 2022. The sharp moderation has comforted policymakers, while raising expectations that sticky core inflation will follow suit. However, concerns remain as to whether core inflation will soon return sustainably to target from currently elevated levels. This reflects the unusual nature of the post-pandemic inflation shock and will keep central banks vigilant and biased to more tightening. South Africa’s (SA) inflation has also turned, but has declined more slowly than global peers. Core inflation has been sticky, despite the weak economy. We believe there is a risk that changes in the post-pandemic economy and shifting inflation drivers will slow the pace of domestic inflation’s moderation.

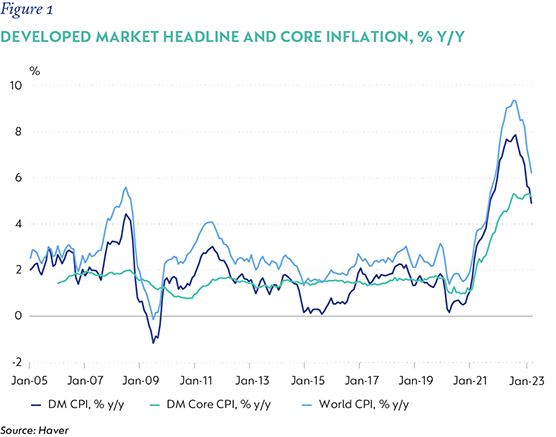

GLOBALLY, INFLATION IS SLOWING

Global headline consumer inflation – including volatile food and consumer fuel markers – slowed to 4.3% year on year (y/y) in May, with a monthly gain of just 0.1%. This is broadly in line with pre-pandemic monthly growth, and annual rates are a full three percentage points (ppt) lower than it did a year ago. Consumer energy prices have been an important driver of the moderation. The two ppt drop in this component of the inflation basket between April and May was broad-based across countries, with the US seeing fuel prices down -3.6% y/y, Japan -3.7% and the UK -1.6%. In Europe, household fuel is concentrated in residential energy prices, and here too declines and base effects are building momentum, with more to come into year end.

Global food prices have also started to ease, as sharply lower agricultural commodity prices feed through into food products. Monthly gains have slowed from 0.7% month on month (m/m) to 0.4%, helping annualised inflation slow to 3.8% from 7.6% at the start of the year.

Looking ahead, inflation is expected to continue slowing, although some of the disinflationary momentum may moderate in the second half of 2023 (H2-23), especially if international oil prices recover, and as base effects fade. Food inflation is expected to ease further, although risks are building from a recent rise in key commodity prices, a drier planting season (El Niño, notably in Latin America) and the war in Ukraine’s threat to the Black Sea grain deal. Nonetheless, that headline inflation is heading meaningfully lower is positive for real incomes and provides some support for consumption and growth and offers some relief to policymakers.

Core inflation has been much less cooperative. May core inflation growth slowed to 0.4% m/m, but the annual gain remains close to 5%, and the monthly annualised rate is also close to this level – which is a long way from convincing central banks that their job is done. Within this, services inflation is still running at a 6% annualised rate. This is where most of the policy-setting focus is, because it is the cleanest inflation indicator of monetary policy transmission (i.e., is policy tightening having the desired effect). While trends by region vary, indicators linked to wages suggest that in some areas – like the UK – price pressures are still alarmingly high. Core goods inflation, which had moderated sharply with the normalisation of supply bottlenecks is now rising again in the US.

Most forecasters expect core inflation to follow headline CPI lower with a lag, as it did on the way up. Certainly, past rate hikes will take time to offset the tailwinds of previous policy accommodation and bed down price- and wage-setting behaviour. Slowing wage growth and industry surveys indicating that inflation pass through has peaked suggest this is already underway, and June core inflation data offers a mixed bag of evidence of easing. That said, a sustainable return to target levels is expected only by the end of 2024, or later in developed markets, and this forecast is usually predicated on a combination of additional rate hikes, and an anticipated mild recession in the US.

SOUTH AFRICA – SIMILAR, BUT WITH DISTINCT DIFFERENCES

While that pace may be slower, SA’s inflation trajectory shares similar features to its global peers, but also has distinct differences. Headline inflation peaked at 7.8% y/y in July 2022 – on average lower than both developed and emerging market peers. Since then, moderating transport costs and a recent peak in food inflation – coupled with a building drag from base effects in these two components – has seen inflation ease to 6.3% y/y in May 2023. In June, CPI slowed to 5.4% y/y somewhat lower than expected.

Core inflation slowed to 5.0%, supported by weaker core goods inflation, coupled with weak hotel- and domestic-wage pressures. However, after a long period of very weak growth, rental inflation has picked up.

While we expect headline inflation to slow further in coming months, we expect core inflation to accelerate from current levels into 2024, and to remain elevated at about 5% in the longer term. This contrasts to the South African Reserve Bank (SARB)’s and market expectations for core prices to moderate roughly in line with headline inflation to the mid-point of the target.

- Economic forecasting is fraught with challenges and, in the wake of the pandemic, the forecast errors for inflation for much of the world were significant. In part, this reflected the dramatic changes the pandemic imposed on countries and, in particular, the profound mismatches between demand and supply, the unprecedented and extended stimulus, and the changed shape of economies in its aftermath. But the experience provides some lessons for our thinking about inflation and underpins our more cautious view. Inflationary episodes tend to have their own dynamics. Attempts to make strong historic comparisons with the post-Covid inflation shock showed some similarities, but also strong differences.

- ‘Common components’ can have a meaningful influence on aggregate inflation. This happens when a single or a few price drivers affect a range of goods and services. The pandemic-related supply chain shocks on goods inflation are a salient example.

- The pandemic reminded us that relative price changes can still ignite broader price pressures. In an environment of low inflation, individual price changes percolate less, limiting the overall price impact. But the opposite is true when the inflation environment has shifted and there are fewer low-inflation alternatives.

- New inflation dynamics can also emerge. Of particular concern are price influences along all points of the supply chain, for which there are no substitutes. These dynamics can make price increases reinforcing, either amplifying or adding to the durability of price pressure in the system.

- Persistence seems to be rising. Persistence measures the proportion of past inflation that is carried over into the next period. In periods of high global inflation – notably in the 1970s and early 1980s – price persistence was very high. This fell visibly from the mid-1980s through the post-Global Financial Crisis, but picked up in the post-pandemic surge.

- Pass-through from core to non-core inflation has also increased.

- While inflation expectations have remained relatively well anchored, history suggests that inflation expectations of people who have lived through a high-inflation episode tend to be higher than those who haven’t.

- The pandemic left many economies shaped differently. In many developed markets (but especially the US), the labour market was most affected. In SA, parts of the economic infrastructure have been damaged, and economic growth has been unable to recover. The economy is less productive and more uncompetitive.

RISKS TO SOUTH AFRICAN INFLATION OUTLOOK

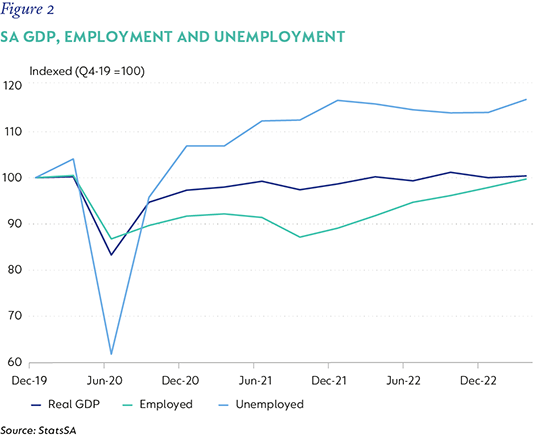

SA also emerged from the pandemic with an economy that looks different to how it did before. Unemployment is considerably higher; employment has almost recovered, but only just and to weak levels overall. Real GDP is hovering at about pre-pandemic levels (give or take), but some sectors have not recovered, in part because network industries, which are really like the vascular system of the economy, are on life support. Government debt is much higher, and the fiscal position more vulnerable, which has raised risk premia and discouraged capital flows contributing to a weaker currency. Taken together these dynamics pose a range of home-grown risks to the outlook for inflation.

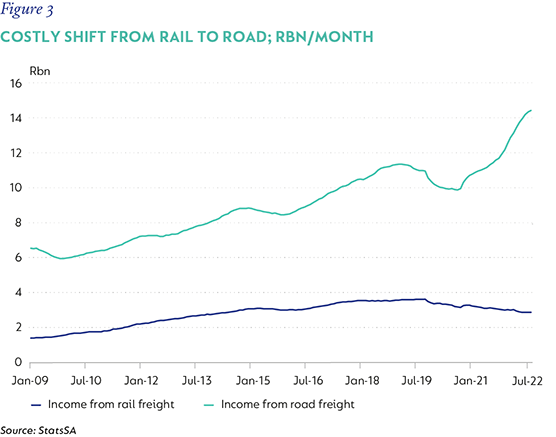

Even though SA’s inflation shock was milder than that of other countries, the pace at which inflation has slowed has also been stickier – despite the very weak economy. Part of the explanation lies in the emergence of a range of inflation drivers that have given rise to new inflation dynamics. The most obvious is the cost pressure that intensified loadshedding has imposed on companies that have been forced to install costly energy backups or run existing expensive diesel generators harder. Sectors most affected include agriculture, transport and logistics, and the broader retail sector, although mining, manufacturing and business services have also been affected. In addition, the cost of logistics has risen. Rail networks are no longer efficient, with freight seeing a dramatic decline in volume y/y, and road transport by payload is more expensive.

This means that literally everything produced, cooled, reticulated, inputted, and transported, on balance, costs more than it did a year ago. While some of this cost has been passed on – certainly, part of the rise in food inflation over the past year reflects these pressures – the weak consumer environment has prohibited full compensation. This means both producers and retailers are more likely, incrementally, to pass through increases where possible, for longer, than not.

As the general price level has risen, reinforcing price pressures are emerging. NERSA’s electricity tariff increase, which adds directly to the CPI, but indirectly to the cost of doing business. Currency weakness is also becoming more evident in some imported goods prices. New vehicle inflation is 7.6% y/y, the highest it’s been since 2017, while book and stationary prices have risen 12.6% y/y. Appliances and furniture prices eased in June, but have shown steady increases in recent months, despite their discretionary nature.

Persistence is an issue. In SA, price persistence has always been relatively high. A 2010 research paper by the SARB and Logan Rangasamy* on SA food inflation and its implications for economic policy, found that persistence in food inflation between 2000 and 2008 was as high as 85%. This means that 85% of past food inflation lingered in the price, while non-food inflation was lower, at 78% and for overall headline inflation it was 81%.

We have carried this analysis forward and find that persistence in food inflation has remained high, and that persistence in non-food inflation has increased materially. In addition, a more granular approach to this analysis suggests that persistence over the longer term is even higher when inflation is accelerating, rather than decelerating. While persistence can be present in both low- and high-inflation environments, the absence of the compound effect of combined common factors in the past decade, coupled with low food inflation, helped inflation ‘self-correct.’ Today, the confluence of combined factors in a higher inflation environment materially raises the risk of them being reinforcing.

In addition to high persistence, we also find – again replicating the research in the cited paper – that pass-through from food to non-food, as well as from non-food to food inflation, is positive. This means that food inflation positively influences non-food inflation, but non-food inflation also influences food inflation, with even stronger statistical ties. This is particularly visible with a 12- to 18-month lag.

The bottom line is that recent inflation may have a significant impact on future inflation, and that there is a positive bi-directional relationship between food and non-food inflation, which is strongest over the longer term – and this relationship has strengthened in the recent past.

Inputting these findings into an inflation model suggests high food inflation will continue to feed into non-food prices into the first half of 2024, while non-food (such as electricity and energy costs, and other administered and regulated prices) inflation will also remain supportive of food inflation over the same period.

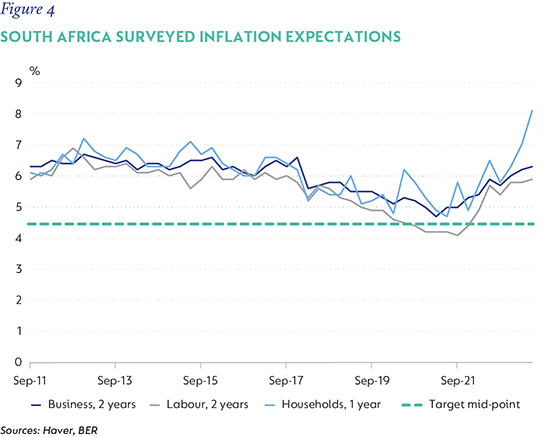

Lastly, inflation expectations – which were well anchored when inflation started to rise – have started to move higher, notably over the medium and longer term. Here, the expectations of businesses and households have not only risen, but took another leg up in the second quarter of this year, suggesting the recent anchoring may have loosened a little.

WHAT DOES THIS MEAN FOR SOUTH AFRICAN MONETARY POLICY?

The MPC has remained a vigilant policy setter and started raising the repo rate in November 2021. Cumulative tightening has been 475bps to date, and the repo rate is currently 8.25%. Despite a decision to hold the repo rate steady in July, the Committee judged inflation risk to be ‘to the upside.’

In late June, the SARB published the details of its revision to the Bank’s Quarterly Projection Model, the MPC’s ‘workhorse’ forecasting model since 2017. The changes are material, and are primarily focused on better formalising how fiscal policy affects both prices and monetary policy. The product is a more comprehensive, granular evolution of its predecessor.

However, several assumptions that are implicit in the model are of some concern to us, not in the mechanics, but in light of the risks highlighted here:

1) The model assumes that inflation expectations are anchored over the long-term at 4.5%. The new model, encouragingly, specifically models the spillovers to more general inflation from fuel and electricity shocks, but these then fade relatively quickly, as low expectations limit the duration of the spillover. This biases the inflation forecast produced by the model towards the anchor, when the anchor may move above the assumed level.

2) Persistence has been modelled to be less than before. Again, this carries the risk that the impact of higher inflation will fade more quickly in the model’s estimates than may be the case.

3) Pass-through from the exchange rate is modelled to be lower than previously assumed. A sustained 10% change in the exchange rate adds 0.9ppt to headline inflation, from 1.3ppt before. This change reflects the assumption that lower economic potential limits the economic stimulus of a weaker currency, therefore also limiting its inflationary impact. This was the case in the lead up to Covid, but recent data suggests pass-through has increased.

There are other changes to the model that are likely to increase its accuracy in other areas, notably the modeling of wages, and, importantly, the inclusion of a fiscal bloc in the model. The former will also likely give a downward bias to the forecasts, but is undoubtedly a better methodology to the previous iteration. Fiscal changes aren’t detailed here, but, suffice to say, that the inclusion is an important formalisation of policy influences which have become increasingly significant in their influence of both inflation, and monetary policy. Notably, the inaugural publication of new inflation forecasts at the July MPC meeting showed a modestly lower inflation trajectory than before.

A LONG WAY BEFORE EASING

With these concerns in mind, we think that stubborn price pressures will see the central bank hold real interest rates in restrictive territory and make cutting difficult to initiate or sustain. We see little scope for easing before mid-2024, and expect the SARB’s assessment of its neutral real rate to drift upwards over time from 2.5% to 3% - suggesting a terminal repo rate of 7.0%-7.5%.

*Rangasamy, Logan “Food inflation in South Africa: Some implications for economic policy” South African Reserve Bank Working Paper 197, November 2010

Disclaimer

SA retail readers

SA institutional readers

Global (ex-US) readers

US readers

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter