United States - Institutional

United States - Institutional

Investment views

Share buybacks

A low-risk, value-creating allocation of capital

The Quick Take

- Share buybacks are a smart capital allocation decision that enhance shareholder value

- They offer a significantly lower risk alternative to other capital allocation choices

- They do not fundamentally alter the business; rather, they increase value per share and return cash that investors can allocate elsewhere

There is no corporate action more misunderstood and maligned than the idea of share buybacks. It is a hotly debated topic that elicits conflicting views. This is not just limited to discussions between asset managers and the boards of listed companies, but also generates plenty of media commentary and public debate. It is debated globally as well as locally, and, given the recently announced ‘tax’ on share buybacks in the US, is misunderstood by politicians as well as the average citizen. It is seen by those who are not in favour as a malign practice that it is intended to boost the value of managements’ share options or undermine the strength of a business to boost shareholder returns; or it reflects that a board with growth ambitions is conceding that the company is ex-growth and has run out of ideas. The reality is that, once you strip the emotion out of the debate, it is simply a form of capital allocation; and one that is most often overlooked, yet it is probably the most successful in terms of generating a return on investors’ capital at exceptionally low risk.

As a long-term investor, we fully appreciate the value that share buybacks bring through permanently reducing the number of shares in issue, and, ultimately, increasing the percentage holding of the company for remaining shareholders. By allocating capital to buy back shares in the existing business, the management team and the board are making an investment in an entity that they know and understand better than any external capital allocation opportunity. As an active manager, we are especially in favour of companies that we own in our clients’ portfolios implementing buybacks. This is because we inherently believe these shares to be undervalued due to mispricing by the market. Said plainly, we are supportive of investee companies implementing share buybacks at a discount to intrinsic value.

PRICE AND VALUE

There are several misconceptions about share buybacks, which I will endeavour to address. First off, there is a view that a company buying back shares is used as a signal to the market. While this might be a side benefit, the underlying premise is always that buying back one’s own shares at a discount to intrinsic value immediately results in permanent value accretion to the remaining shareholders. Simply put, you’ll be buying R1 of value for 80c or 50c, depending on the discount implicit in the market price.

A standard argument raised by boards against buybacks is: ‘What happens if we buy back our shares and next month the share price trades lower. The market will say we destroyed value.’ The fallacy here, of course, is that the market price at any one time is an accurate indicator of the true underlying value of the business. Anyone who has lived through the last few years of violent share price swings will know that the efficient market hypothesis is a wonderful theory that does not exist in the short term. Market prices continuously move away from the underlying long-term value of a business, this is what enables a manager like Coronation to deliver the alpha that we have over the years (2.5% alpha since inception). The whole concept underlying active asset management is taking advantage of market mispricing to build long-term value. When we identify mispricings in the market, we will buy a share that is trading below what we think its intrinsic value is. The next day, the market may take the price lower, but, if we are correct on what the value of the business is, the price will reflect this valuation in the long term. Markets are inefficient in the short term, but, ultimately, efficient in the long term. So, it is irrelevant that the price may move lower at some point, so long as the share was bought back at a discount to its intrinsic value, then value has been created for shareholders.

It’s also fallacious thinking because this same benchmark is seldom held against other capital allocation decisions. The Harvard Business Review quotes research that 70% to 80% of merger and acquisition (M&A) deals fail. This is an astounding statistic. The fact that anyone undertakes M&A with this level of failed outcomes is testimony to the marketing abilities of investment banks! Yet boards happily proceed with these transactions with far less circumspection than they apply to undertaking buybacks.

The outcomes for large capital projects are not as poor as that of M&A, but an equally scary 50% of large capital expenditure (capex) programmes fail to achieve their cost of capital. Once again, boards are happy to sign off on large capex projects based on spreadsheet forecasts, without the same rigour of testing that appears to be the hurdle before pronouncing on share buybacks.

What is not given enough attention is the fact that a capital investment in share buybacks is a permanent investment, the benefit of which will last forever, without any further capital required. Shares bought back and cancelled is a dividend saved and value per share is enhanced into perpetuity.

ALLOCATING CAPITAL

The next argument, much loved by social commentators, is that buying back one’s shares is somehow ‘shrinking the business’ and bad for the economy. This is usually followed up with the argument that the capital should rather be used to invest in something new. The flaw in this argument is that a share buyback is not shrinking the actual operating business. The company and its ongoing operating assets do not change, it merely reduces the number of outstanding shares and concentrates the holdings of those who wish to remain invested.

Clicks is the poster-child example of a company that has bought back a significant number of shares and grown its business at one of the fastest rates in corporate South Africa (SA). In the early 2000s, Clicks went through a period of weak operating performance, resulting in its share underperforming. As its operations recovered, the company used part of its surplus cash flows to consistently buyback shares as long as they felt the market was undervaluing it. From when it started recovering in 2006 to today, the company has bought back 29% of its shares in issue, turning a strong recovery in operating performance (earnings growth of 700% over the intervening 15 years) into spectacular performance for the remaining shareholders, demonstrated by earnings per share growth of 1018%.

Buybacks enable companies that are generating surplus cash but lack new potential investment opportunities that can generate equally good returns, to return surplus capital to shareholders. Investors can then deploy that capital into other attractive opportunities. It is positive for capital to move back to investors that can allocate to a range of potential opportunities, instead of just being used by one company because it was available. In fact, companies that succumb to the pressure to invest into new projects to ‘show growth’ will more than likely end up making poor investments that destroy that capital and prevent it from being redirected to shareholders who have a much wider opportunity set. In the recent past, we have had the experience of Sasol that invested heavily in a major offshore chemicals plant, a move that ultimately put the entire business at risk. Similarly, Woolworths’ expensive foray into department stores in Australia placed its balance sheet under immense stress. In both cases, misadventures through allocating capital offshore to risky new projects ended up threatening the cash producing local operation.

WHAT’S SPECIAL ABOUT BUYBACKS OVER DIVIDENDS?

Some companies will argue that returning cash to shareholders via a special dividend is a preferred method of returning surplus capital. It avoids the board being exposed to debate around the price they paid for the shares, and it ensures that all shareholders participate equally in the return of capital. While we certainly prefer a special dividend over capital being employed in value destructive expansion, the nature of a dividend versus a share buyback is often an opportunity lost. The frictional costs attached to a special dividend are often higher than that of share buybacks, but the real difference in value lies in the permanent value creation of a buyback. The accretion delivered by share buybacks is ultimately very helpful in growing the per-share value of future distributions to remaining shareholders, as alluded to above. The purchase of a share today results in a permanent value accretion to the remaining shareholders, whereas a special dividend results in a once-off bump in the return and then it’s gone and forgotten.

A UNIQUE OPPORTUNITY

There has been significant selling pressure on the JSE this past year. Appetite for emerging markets in general is low, and SA, with its own unique set of challenges, benchmarks poorly against some of its peers, resulting in most global emerging market managers being actively underweight SA. This has been compounded this year by the relaxation of Regulation 28 of the Pension Funds Act, which has allowed local pension funds to increase their foreign holdings from 30% to 45%. Many funds have taken advantage of this relaxation to increase their offshore equity holdings at the expense of their domestic holdings. Hence, despite solid earnings growth by many JSE-listed companies, we have seen constant selling - even at these low multiples. This is a unique situation in which SA-listed companies, despite seeing limited growth locally, are producing significant free cash flow. Some companies will try to manufacture growth by attempting to expand offshore, with all the attendant risks; while those that take advantage of the unique opportunity to buy back shares at these accretive levels will have a defining, once-in-a-generation opportunity to add significant value at extremely low risk. The future returns from those companies that take advantage of this will be significantly ahead of those that don’t.

SETTING THE EXAMPLE

There have been many successful examples of companies in SA that have added significant value through buying back their shares. I referenced Clicks earlier in the article, but, recently, a number of companies have started buying back their shares as their underlying operations have generated significant cash and the market has provided them with the opportunity to buy at attractive levels.

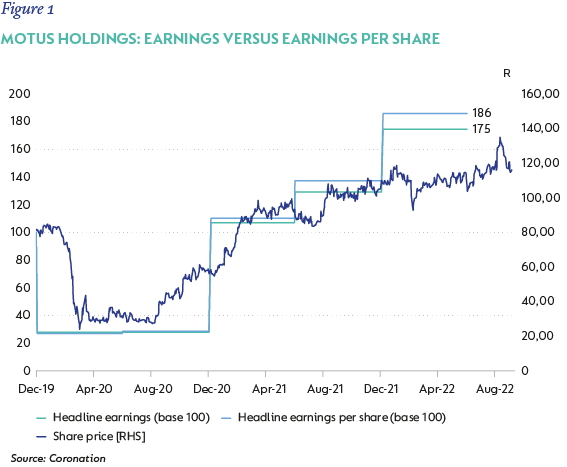

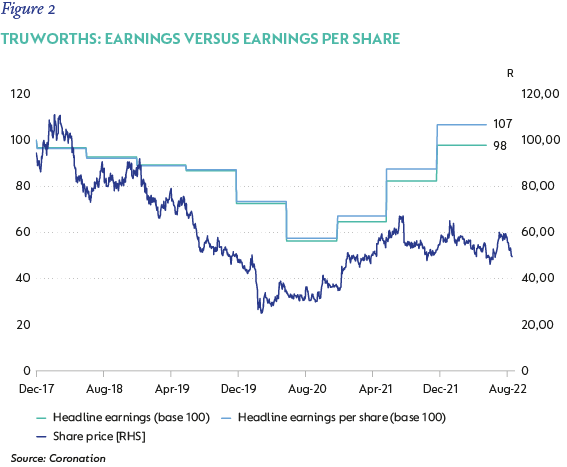

Motus and Truworths (figures 1 and 2) have recently started buying back shares, and the improvement in headline earnings per share against headline earnings is already visible, and this gap will grow over time due to the compounding effect.

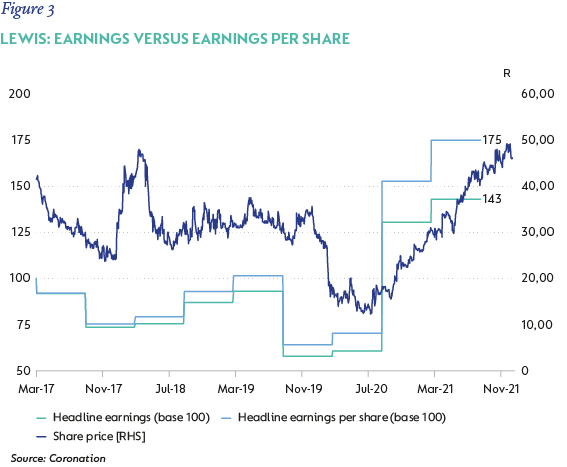

This positive benefit over time is very visible in the example of Lewis (Figure 3), which has been buying back shares for a number of years now. It vividly demonstrates the value that can be added through the aggressive repurchasing of shares when market sellers are happy to sell shares to the company at low valuations.

These three companies have signaled that they are buying back shares in the market, so there is no asymmetry of information, it is merely the difference in time horizons and possible asset allocation views that result in the opportunity to buy back shares at big discounts to intrinsic value. In a wonderful change of focus, Woolworths, which has now stabilized its Australian operations and is once again generating excess cash, has recently announced a share buyback. A welcome turn of events.

ALL THINGS BEING EQUAL

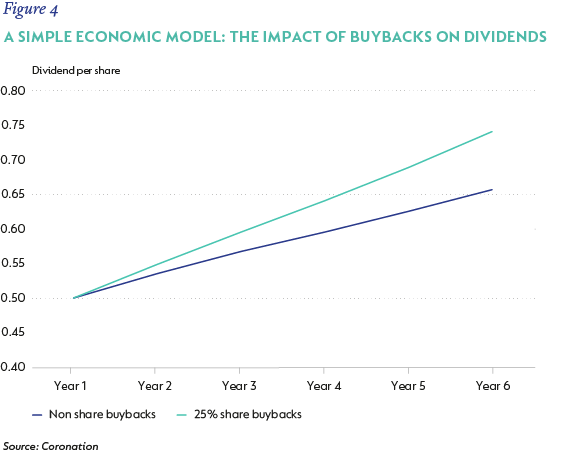

In order to show the true impact of what we are trying to achieve with share buybacks but without the volatility of real-world situations, it is best to show the impact on distributions paid to shareholders (ultimately, the reason why we invest in listed companies is for the returns paid back to shareholders).

The simple example illustrated by Figure 4 assumes a company that is stagnant in real terms. It is growing its earnings in line with inflation, a fairly reasonable assumption for a company in SA given the low economic growth. It also assumes that the company is trading at seven times earnings, again reasonable given where a lot of shares are trading in the market today. Finally, the assumption is that this company pays out 50% of its earnings as a cash dividend annually. The two diverging lines then contrast the impact if the company had merely retained those extra cash earnings (and earn a cash yield on that) against the decision to use half its retained earnings (25% of each year’s profits) to buy back shares annually (on a seven times price earnings ratio). The impact over the five-year period is staggering, with the dividend in the final year being 15% higher than it would have been if no share buybacks had been undertaken. Also consider that total return is higher again (even assuming the market keeps the share on a seven-times earnings rating), as the share price will be higher, resulting in a total return 24% higher over this period than if the company did not buy back shares.

CONCLUSION

Capital allocation is one of the biggest value drivers in running a business. The most successful businesses over time have shown that capital is a scarce resource, and it should be applied where the risk-adjusted return will be the highest. Share buybacks are often not considered against the more traditional uses of allocation, such as M&As and project finance, despite it being the lowest risk in terms of expected outcome. With markets today presenting a unique opportunity with exceptionally low valuations, share buybacks should be the hurdle applied to all capital allocation decisions, and pursued actively by most companies in this low-growth environment.

Disclaimer

SA retail readers

SA institutional readers

Global (ex-US) readers

US readers

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter