United States - Institutional

United States - Institutional

Investment views

US Home improvement retailers

A growth opportunity in the lacklustre retail space

- Lockdown boosted already-strong home retailers despite ailing retail sector

- Scale, product breadth and accessibility favour big-box DIY retailers

- Service and operational efficiency key to keeping physical retailers ahead of online competition

- We see further momentum in the home improvement space

THE BIG-BOX HOME improvement retailers, Home Depot and Lowe’s Companies, have been a bright spot in the otherwise moribund US retailing industry. While the broader sector has been littered with high-profile bankruptcies and store closures, the shares of Home Depot and Lowe’s have returned 52% and 83%, respectively, over the past three years. This performance has been a function of an advantaged competitive position, favourable macroeconomic trends and good execution.

This strong performance has been amplified during the Covid-19 crisis. Lockdowns and work-from-home mandates around the country forced people to spend more time in their homes in 2020. In many cases, this led consumers to place greater value on their homes, and prompted a flurry of do-it-yourself activity. As a result, while many retailers were reporting sales declines, Home Depot and Lowe’s saw sales grow 18% and 23%, respectively, for the first nine months of the year.

FAVOURABLE MARKET DYNAMICS AND HARD-TO-REPLICATE BUSINESS MODEL

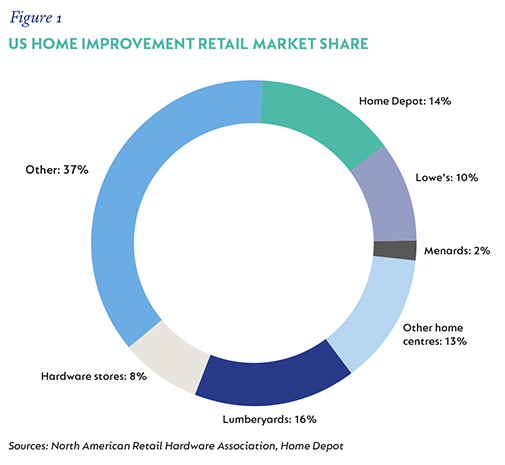

The US home improvement market is worth roughly $650 billion annually. Home Depot (with a 14% market share) and Lowe’s (10% market share) dominate the industry; outside of the top two, the market is highly fragmented, with a long and diverse tail of smaller competitors such as regional lumberyards, electrical and plumbing distributors, smaller hardware stores and garden centres.

The value proposition for the big-box retailers is premised on lowest price (scale), breadth of assortment and ubiquity (particularly relevant for professional contractors). Smaller and specialist competitors, on the other hand, often compete on the basis of service levels, reliability of delivery (within the local catchment area) and depth of assortment within category. Given ongoing investment in in-store execution levels, delivery infrastructure and e-commerce (allowing for significantly higher stock-keeping unit [SKU] count online than the retail box), the value proposition of many independents is steadily being eroded by Home Depot and Lowe’s. The vast majority of the competitor set lacks the scale and resources to match Home Depot and Lowe’s on pricing and capital investment. As a result, big box (Home Depot in particular) has taken market share, and is likely to continue doing so, from the fragmented tail.

Compared to other categories of retail, Home Depot and Lowe’s enjoy strong positions relative to Amazon and other pure-play online retailers (e.g. Wayfair and Build.com). The risk of online disintermediation varies by product category – disposable, consumable categories such as light bulbs, paper towels or detergents can readily be sold competitively by Amazon; however, these categories comprise <5% of sales and are typically not drivers of traffic.

On the other end of the spectrum, big-ticket project-based purchases (where purchases from multiple product categories are coordinated across the scope of a remodelling project) lend themselves to the store (where sales associates help coordinate the project). Amazon can conceivably compete for categories such as power tools, but consumers appear to value the product expertise and in-store trial offered by the big-box retailers (e.g. Lowe’s has a wall that customers can drill into to test new drills).

In addition, home improvement typically requires a more specialised supply chain. For instance, Home Depot believes that while c.80% of Amazon’s sales could theoretically be delivered by drone, only c.30% of Home Depot’s sales would be small enough. The average Home Depot delivery weighs 9kg. Both Home Depot and Lowe’s are investing heavily in their supply chains to allow for fast and efficient delivery of big and bulky orders. While Amazon, of course, has the resources to replicate, the delivery infrastructure required to get timber and cement to a job site is quite different from Amazon’s current configuration.

RISING MAINTENANCE NEEDS SUPPORT DEMAND GROWTH

The backdrop for home improvement retail is structurally attractive. For much of the past decade, Americans have underinvested in residential real estate compared to historical norms. This has led to an ageing of the housing stock – the median home is now over 40 years old, an age where maintenance requirements typically accelerate. In addition, homes have steadily increased in size over time, which naturally also leads to higher maintenance requirements.

House prices have consistently grown by 5% over the past decade, which has resulted in a complete replacement of homeowners’ equity that was eroded in the 2008/2009 Global Financial Crisis. When consumers see appreciation in the value of what is, for most households, their largest asset, their willingness to reinvest in maintenance increases.

HOME DEPOT HISTORICALLY THE LEADER, BUT LOWE’S IS CLOSING THE GAP

The investment case for both Home Depot and Lowe’s remains very compelling. Home Depot is the market share leader, has more productive stores, a greater following among professional customers and higher margins. Nevertheless, despite historically living somewhat in the shadow of Home Depot, Lowe’s is our preferred stock in the sector currently.

A new management team, under the leadership of CEO Marvin Ellison, has been in place for the better part of two years now, and has demonstrated a very credible path to narrow the performance gap to Home Depot. For instance, in the past year, non-core businesses have been sold or shut, IT infrastructure has been modernised, merchandising functions have been overhauled and significant investments have been made in logistics.

Many of the changes are simple in nature, but highly impactful. For instance, implementing a task-based labour scheduling system has led to a nearly 50% increase in the amount of time spent serving customers, as opposed to doing administrative tasks. Similarly, carrying higher levels of inventory in key items such as lumber has made Lowe’s more appealing for professionals. These operational changes are translating into meaningful financial gains. Over the past 12 months, Lowe’s has grown revenue by 19% (versus 13% for Home Depot) and operating margins from 9% to 11%. Margins are expected to reach 12% in the next year or so, and 13% soon thereafter (versus Home Depot’s current 14%).

SUSTAINABILITY MATTERS

Both Lowe’s and Home Depot are responsible corporate citizens – for instance, during the early stages of the pandemic, both companies donated their entire stock of N95 respirator masks to the healthcare system, along with other critical items in short supply.

No investment is without risk, and the fortunes of Lowe’s and Home Depot cannot be completely divorced from the broader economy and the housing market in particular. Should fiscal stimulus measures fail to adequately compensate for the economic damage wrought by Covid-19, or if interest rates aggressively start rising, the housing economy may be negatively impacted.

Nevertheless, in a retail sector that’s been under fire from multiple angles, the big-box home improvement players have been standouts, and are, in our view, likely to continue to outperform. +

Disclaimer

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter