South Africa - Institutional

South Africa - Institutional

Factfile: Coronation Global Houseview - July 2016

INCEPTION DATE: 1 October 1993

PORTFOLIO MANAGER: Karl Leinberger is the chief investment officer of Coronation. He has been the manager of the Global Houseview portfolio for almost a decade.

Overview

The Coronation Global Houseview Fund represents our best investment view for a balanced portfolio in all major asset classes – equities, property, bonds and cash, both in SA and abroad. It is an actively managed balanced portfolio with a medium-risk profile. Global Houseview is managed in accordance with Regulation 28 of the Pension Funds Act and many retirement funds use the product as a core holding or trustee default option.

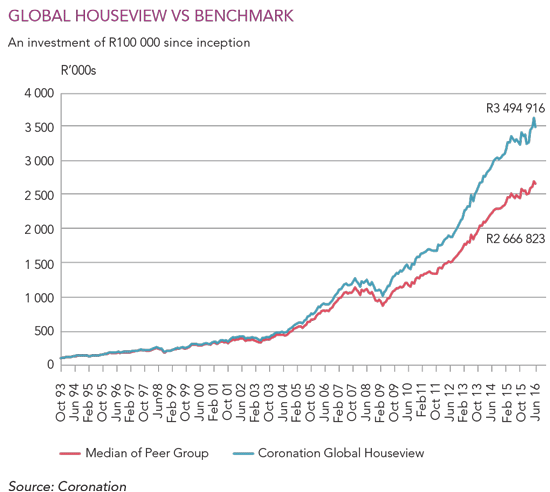

The fund has delivered compelling returns, outperforming its benchmark by 1.37% per annum since inception more than two decades ago.

Strategy

Global Houseview is managed according to the Coronation investment philosophy, which is underpinned by an unwavering commitment to the long term. The market is fixated on short-term newsflow, resulting in the mispricing of the long-term prospects of investments. Most investors are forced into buying companies where the news is good and getting better, but with a time horizon of more than five years, the Global Houseview portfolio can invest in undervalued assets where the news may not be as good.

These mispriced assets, which are trading at discounts to their long-term business value (fair value), are identified through extensive proprietary research. In calculating fair values, we focus on through-the-cycle normalised earnings and/or free cash flows using a long-term time horizon. The portfolio is constructed on a clean-slate basis based on the relative risk-adjusted upside to fair value of each underlying security. We do not equate risk with tracking error, or divergence from a benchmark, but rather with a permanent loss of capital.

Asset allocation is key and the Global Houseview Fund benefits from Coronation’s other competitive advantage: a single, integrated investment team. Investments are not researched in silos. All our analysts and fund managers sit in an open-plan environment where the merits of different asset classes and investments are debated and measured up against one another. We believe this perspective results in better investment decisions across asset classes, which are particularly evident in a balanced fund like Global Houseview. We can sift through the entire spectrum of assets and identify those that can offer the best risk-adjusted returns for the fund.

Currently, equities remain our preferred asset class for producing inflation-beating returns. We prefer global to domestic equities on the basis of valuation. The fund has the maximum allowable exposure offshore and most of this is in equities (around 70% in developed market equities and the balance in emerging markets). The well-understood challenges in emerging markets have resulted in many high-quality companies with great management teams and excellent long-term prospects trading at very undemanding levels.

In SA we remain heavily invested in the high-quality, global businesses that happen to be listed on the JSE (such as Naspers, Steinhoff, British American Tobacco and Anheuser-Busch InBev). These companies have robust business models, are diversified across numerous geographies and currencies, and remain attractive based on our assessment of their intrinsic value.

A high weighting in property stocks continues to be a major differentiator for the fund. We expect domestic properties to grow distributions at reasonable levels over the medium term. This growth, combined with a fair initial yield, suggests an attractive return over the holding period.

Outlook

We believe that interest rates worldwide will remain abnormally low for a prolonged period of time. The real returns from cash and government bonds are therefore likely to be poor over the long term, both from a local and global perspective. Accordingly, we continue to favour high equity weightings in the fund.

However, volatility remains heightened and markets continue to overreact to the news of the day. This has resulted in the opening up of gaping valuation differentials – particularly in quality cyclical companies. These have been sold off as investors fled to more predictable defensive stocks.

Recently, some of these holdings in the fund have delivered strong returns as valuations started to normalise. Even in the absence of a near-term cyclical upturn, we believe our contrarian positions will continue to serve the fund well over time.

This includes resource stocks, which have significantly underperformed the rest of the market – even after the recent recovery. The resources index has delivered negative returns over one, three and five years, and has underperformed cash over a ten-year period. While most commodities are in oversupply in response to projects approved eight years ago at the top of the cycle, we believe that valuations are compelling and sufficiently discount these risks.

In a world of constant change, our investment philosophy remains unchanged – we are valuation-driven and committed to the long term.