South Africa - Institutional

South Africa - Institutional

Investment views

The grass is not always greener

Offshore acquisitions by domestic companies

- Many South African companies have expanded offshore, but few have truly succeeded abroad.

- Deteriorating economic conditions have eroded seemingly sound investment cases.

- Since Woolworths’ acquisition of David Jones in 2014, the Australian retailer’s profit has fallen, resulting in partial impairment of the initial investment.

- Sasol’s Lake Charles Chemicals Project in the US has experienced extreme cost overruns, which are threatening economic value for shareholders.

“I’m no genius, but I’m smart in spots, and I stay around those spots.” – Tom Watson Snr, founder of IBM

WARREN BUFFETT FREQUENTLY uses the concept of the ‘circle of competence’ in his letters to Berkshire Hathaway shareholders to illustrate the importance of staying focused. This applies equally to capital allocation decisions in a business. Despite building formidable businesses and raising the barriers to entry for new entrants during years of operating in a closed, domestic economy pre-1994, there is a preoccupation among many South African management teams that the grass is greener elsewhere. This has led many domestic companies to expand offshore, usually by acquisition, the majority of which have had disastrous consequences for shareholders.

There is the odd success story, but they are the exception rather than the rule. Offshore acquisitions by domestic companies have been pervasive across sectors – as an example, virtually every major South African life insurer and commercial bank has acquired a business outside of South Africa. Of the numerous examples in our market, two of the larger transactions recently undertaken are interesting case studies.

ACQUISITION OF DAVID JONES BY WOOLWORTHS HOLDINGS

Woolworths Holdings announced in April 2014 that it would pay R21.4 billion (A$2.1 billion) for David Jones, the iconic Australian department store. David Jones services the more affluent Australian consumer through a network of 38 stores, four of which it owned, including the flagship department stores in Sydney and Melbourne. This was a sizeable transaction, comprising nearly a third of Woolworths’ market capitalisation at the time, and valued David Jones at a 21 times price earnings multiple based on its last reported earnings.

Fundamentals in place

While South African retailers have a dismal track record in acquiring businesses in Australia – most notably Pick n Pay’s failed acquisition of Franklins and Truworths International’s unsuccessful foray with Sportsgirl – investors were prepared to back Woolworths CEO Ian Moir.

Moir was appointed CEO in November 2010 after successfully turning around Country Road, another Australian retailer acquired by Woolworths in 1998. Up until the acquisition of David Jones, Moir had an enviable track record – Group revenue and profits grew strongly during his tenure, compounding at 14% and 23% per annum, respectively. Although department stores have come under threat globally, losing market share to specialist and online retailers, the rationale for acquiring David Jones sounded compelling:

- It had been undermanaged for several years and basic retail discipline had slipped, which was evident in its steadily declining trading densities. Underinvestment in IT systems and poor processes meant that it lagged its peers in online retail, lacked a compelling loyalty programme and had a poor omnichannel offering.

- Private label product was nonexistent (only 3.5% of revenue) and there was an opportunity to improve operating margins and profitability by selling more David Jones and Woolworths brands through its store network.

- There were significant scale benefits that would allow the enlarged Group to leverage its buying power and design capabilities, which would improve price efficiency. This would allow Woolworths to strengthen its southern hemisphere platform as a defence against northern hemisphere entrants such as H&M and Zara, both in South Africa and Australia.

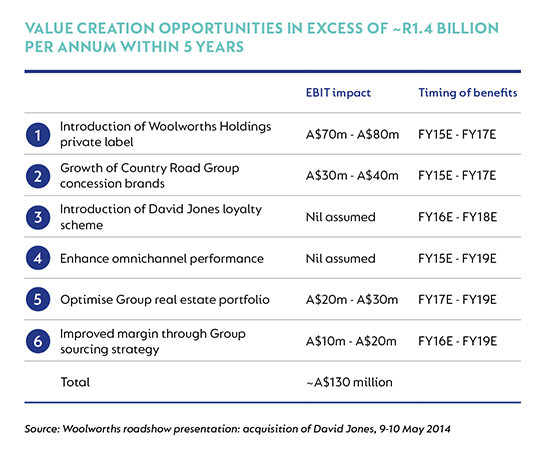

The net result of these initiatives was an expected uplift of between A$130 million and A$170 million per annum in incremental earnings within the next five years. This was significant in the context of David Jones having generated A$143 million operating profit at the time of acquisition.

This target was described as ‘conservative’ by Woolworths, indicating its confidence in extracting these synergies, thereby justifying the high price paid. Initially, this confidence was vindicated as profitability improved at David Jones. Woolworths appeared to be executing flawlessly and seemed to uncover further opportunities to enhance value, including launching a fresh and prepared foods business in Australia.

David Jones grew sales ahead of the market, gaining market share from its major competitor, Myer. Margins expanded and nearly a fifth of the purchase price was recouped when it sold its Market Street property in Sydney to the Scentre Group for A$360 million.

These proceeds would be used to fund its capital expenditure programme, including the implementation of new IT and finance systems, relocating its head office to join that of Country Road in Melbourne, refurbishing its flagship Elizabeth Street store, and trialling its food concept.

Conditions deteriorated

All appeared to be going according to plan, until trading took a turn for the worse in 2017, due to the following factors:

- The Australian retail environment deteriorated as discretionary spend came under pressure, exacerbated by high levels of consumer indebtedness. This resulted in heavy discounting as retailers competed aggressively for market share, leading to pressure on both revenue growth and gross margins.

- The introduction of private label product failed to resonate with the David Jones consumer. This was a significant setback, as it was anticipated that this move would generate around half of the synergies announced at the time of acquisition.

- The deterioration in financial performance resulted in several management changes within a short period of time. As a result, Moir and other South African managers were forced to become increasingly involved in the daily running of David Jones. This was at the expense of the South African operations, which were also experiencing a highly competitive retail environment and a declining economy.

- These setbacks occurred during a period when David Jones was implementing various transformative projects, such as the Elizabeth Street refurbishment, investment in an omnichannel and loyalty programme, new merchandising and finance systems, head office relocation, and a food concept trial. The associated implementation costs further reduced profitability.

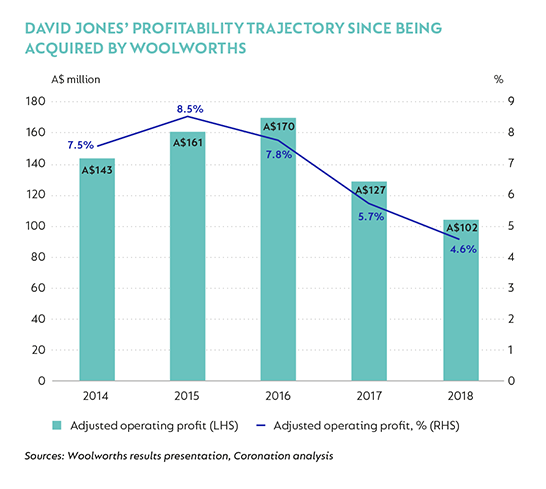

The above graph shows how profitability grew during the first two years post-acquisition, reaching a peak of A$170 million before collapsing and eventually troughing at A$102 million – a decline of 29% since acquisition and 40% from the peak.

This decline weighed heavily on Woolworths’ investment in David Jones and culminated in an impairment charge of A$712.5 million (R6.9 billion) taken in January 2018, effectively writing off a third of its initial investment.

Transformation push

Woolworths’ transformative initiatives appear sound – a similar strategy has been adopted by successful department stores elsewhere in the world such as John Lewis, Selfridges and Bon Marche – and should enable David Jones to compete more effectively against online and specialist retailers, and to address the impact of undermanagement.

While Woolworths may be able to extract some value from David Jones in the short term, there is a significant risk that it has acquired a ‘melting ice cube’ – department stores globally are increasingly under threat from online retailers and changing consumer shopping patterns. It is possible that it will continue to lose relevance over time.

This would be a disappointing outcome for shareholders, not only in terms of the potential value at risk, but also the significant management distraction away from the core South African operations. It will become evident over the next 18 months which way this investment is panning out.

SASOL’S LAKE CHARLES CHEMICALS PROJECT

In late 2012, Sasol announced that it was progressing the front-end engineering and design of the Lake Charles Chemicals Project (LCCP), an ethane cracker and gas-to-liquids (GTL) project in Lake Charles, Louisiana, on the Gulf of Mexico.

The advent of the US shale industry meant that it would have surplus natural gas, including ethane and methane gas. An ethane cracker uses ethane gas, and processes or ‘cracks’ it into ethylene and other derivative products. A GTL plant uses a refinery process to convert methane gas into longer-chain hydrocarbons, such as diesel.

The prices of these finished products are determined relative to the oil price. Effectively, the LCCP was looking to exploit the price differential between cheap feedstock (due to a surplus of natural gas caused by the booming shale industry) and a high oil price.

In October 2014, Sasol announced the final approval for the LCCP, with beneficial operation expected to begin in 2018.

The total expected cost of approximately $8.9 billion, c. 27% of Sasol’s market capitalisation at the time, was roughly $3 billion to $4 billion higher than comparable ethane cracker projects being constructed in the region by peers such as Dow Chemical Company and Chevron Phillips Chemical Company. Sasol justified this differential due to:

- Competitors already having considerable polyethylene infrastructure in place.

- Differing downstream chemical derivative configurations – Sasol would have a greater mix of higher valued finished products.

- The LCCP also included some capital expenditure in respect of the GTL plant.

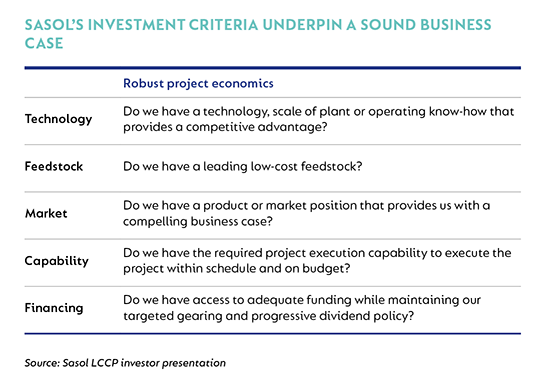

Despite the significant project cost, Sasol’s management was confident that the LCCP investment case was sound and ticked all the necessary boxes.

Stress test

The economics of the LCCP were initially based on the following key assumptions:

- A long-term real oil price of around $100 per barrel and stress tested at $90 per barrel.

- A long-term Henry Hub gas price of $3 to $4 per metric million British thermal unit.

Based on these assumptions, Sasol was confident that the case for LCCP was robust and it was expected to exceed its hurdle rate of 10.4% in US dollar terms (1.3 times Sasol’s weighted average cost of capital [WACC]).

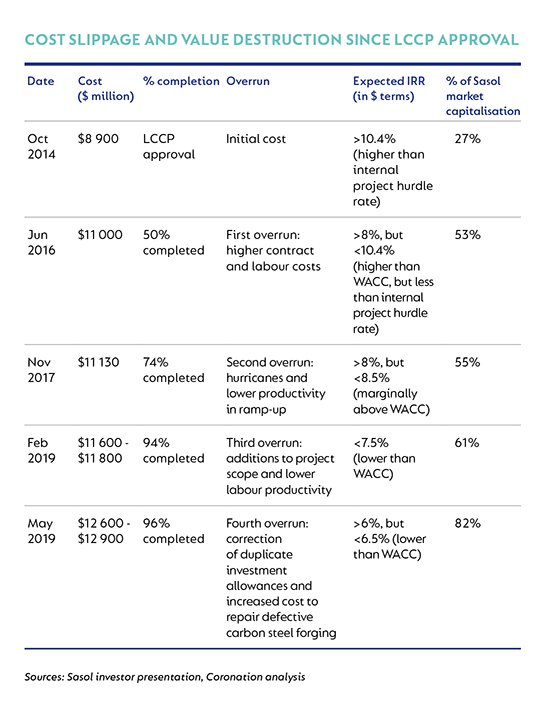

Anyone who has ever built or renovated a house knows that large projects are unlikely to be completed timeously and on budget. This well-known fact, combined with the vagaries of oil and natural gas price fluctuations, meant that the LCCP was doomed to overrun. The ‘robust’ economics of the LCCP would soon be tested by external and internal conditions:

- The oil price crashed in late 2014, causing Sasol to reduce its long-term real oil price assumption to $80 per barrel. Under this scenario, the project’s internal rate of return (IRR) would still be expected to exceed its WACC but fall short of the 10.4% project hurdle rate.

- In March 2016, Sasol announced a delay of six to 12 months, shifting the beneficial operation of the smaller derivative units out to 2019 due to the company pacing out the project in line with a lower oil price as well as ‘some initial challenges’. These challenges resulted in Sasol revising the cost of the LCCP higher, to $11 billion in June 2016, due to:

- construction delays caused by above-average rainfall and subsequent hurricanes (Harvey, Irma and Nate) off the Gulf coast;

- poor ground conditions;

- higher-than-expected labour costs;

- certain components of the lump-sum bid contract prices being higher than originally estimated; and

- required quantities of bulk materials overshooting the original estimates.

While these delays resulted in an approximate 25% increase in the cost of the LCCP to just over $11 billion, conditions deteriorated again in early 2019, as follows:

- IHS, the chemical consultancy used by Sasol on the project, reported a further potential delay of around three to five months. Sasol confirmed this delay in early February 2019, causing it to revise the LCCP cost higher, to between $11.6 billion and $11.8 billion.

- Despite reaffirming the revised cost at an investor conference in March 2019, Sasol then shocked investors in mid-May by revising the project’s cost higher, to between $12.6 billion and $12.9 billion. This latest overrun resulted in Sasol lowering the overall expected IRR to between 6% and 6.5%, which is well below its WACC. This means that even if the remainder of the project unfolds as expected and in line with Sasol’s financial assumptions, the LCCP would destroy significant economic value for shareholders.

The significant cost slippage and value destruction from the time of first approving the LCCP are apparent in the following table.

The net effect

The extent of cost overruns is truly breathtaking, and the impact on Sasol and its shareholders has been significant:

- Sasol had R10 billion in net cash just prior to greenlighting the LCCP. The significant cost of the project, coupled with overruns, has caused debt to balloon, with Sasol’s debt-to-equity ratio now sitting at approximately 49% and likely to increase further. This indebtedness has reduced balance sheet flexibility, which means that Sasol has been unable to buy back its shares to take advantage of a depressed share price. It has also meant lower dividend payments to shareholders as it looks to shore up its balance sheet.

- Sasol announced a R30 billion to R50 billion cost-response plan that includes extracting cost savings, reducing dividend payments, delaying capital expenditure on its existing business, and seeking asset disposals for value. While it’s always good practice to extract cost efficiencies, these initiatives raise concerns of plant underperformance if maintenance spend is curtailed, missed potential for value-accretive acquisitive opportunities, and the loss of key employees due to salary freezes and reduced bonuses.

Risks remain

While the value destruction suffered by shareholders is significant, the risks facing the LCCP have not abated. There is the potential for further overruns should the ramp-up transpire slower than envisaged. More importantly, the commodity cycle for the key chemicals that will be produced by the LCCP could change if global demand for these products slows. Given that these are niche products, any small changes in demand will have an outsized impact on the expected profitability of the LCCP, thereby further impacting on the project’s ability to add value.

There is a well-known aphorism that states: “The road to hell is paved with good intentions”. In a weak domestic economy, virtually every management team must feel the temptation to diversify offshore. However, these are not regions in which they have a competitive advantage and are almost certain to distract them from their local businesses.

Despite having the best intentions when looking to expand by acquiring businesses offshore, history, as demonstrated by the above examples, shows that reality can differ significantly from the attractive returns promised by a spreadsheet. What appears to be heaven can end up as hell for shareholders. With this in mind, as active investors, we continue to engage with the management teams and boards of directors of investee companies where we feel there is a risk of value being destroyed to ensure the best outcome for our clients over the long term.

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter