South Africa - Institutional

South Africa - Institutional

Investment strategies

South African Bond Outlook - Getting ahead of the curve

South African government bonds remain attractive despite global shocks

- SA’s already poor fiscal position was hit hard by the decline caused by Covid-19; the Moody’s downgrade was mostly already priced

- While the SARB has gone some way to increasing liquidity, we expect more rate cuts going forward

- There is value to be found in South African bonds and we are poised to maximise opportunities on behalf of our clients

From mid-February 2020, the world experienced what can only be described as a near cataclysmic shock. The double crisis of a global oil price war and the rapid spread of Covid-19 across continents has seen shockwaves of fear and panic penetrating geographical and generational boundaries. Governments across the globe have reacted by enforcing either social distancing or more severe isolation through nationwide lockdowns. This is done in order to flatten the curve of infections in a bid to prevent healthcare systems from being overwhelmed and, hopefully, allow the pandemic to be better managed. The risk, they fear, is that it escalates into a global catastrophe.

The key unknowns in this global pandemic are how quickly the virus burns out (if at all), whether herd immunity will develop, what the most effective treatment for Covid-19 is and when (if at all) a vaccine will be ready. Financial markets have reacted fiercely to the economic uncertainty created by the required lockdowns. Over the last quarter, global stock markets are down 20%, most emerging market currencies are down between 15% and 20%, global credit markets are down at least 7%, and global listed property is down 30%. The magnitude of these moves has not been seen since the Global Financial Crisis (GFC) of 2008/2009, and, importantly, these moves have all occurred in a much shorter time period.

THE EFFECT ON SOUTH AFRICAN FIXED INTEREST ASSETS

No country has been insulated from this crisis and the concurrent slowing in growth and economic uncertainty. The South African Reserve Bank (SARB) reacted by cutting interest rates by 100 basis points (bps) in March, and in subsequent days also unveiled an unprecedented number of measures to keep liquidity in the banking sector. These included offering long-term repurchase agreements (repos) of up to one year on government bonds; buying government bonds in the secondary market so as to support market liquidity; lowering certain regulatory bank capital ratios to support the economy; and temporarily adjusting the funding mix in weekly government auctions towards shorter-dated government bonds. These measures helped calm the fixed income markets somewhat, but the downward adjustment in asset prices was already quite severe. Year to date, the All Bond Index (ALBI), the Inflation-linked Bond Index and the All Property Index were all down (8.7%, 6.6% and 48.1%, respectively), bringing their respective one-year returns to -3%, -5% and -49%. Cash has been the only asset class to deliver positive returns over both the last quarter and one year, yielding 1.6% and 6.8%, respectively.

FRAMING OUR ACTIONS

Former US President John F. Kennedy once reflected, “When written in Chinese, the word ‘crisis’ is composed of two characters. One represents danger and the other represents opportunity.” We believe this observation holds true for this crisis as well. In assessing it, we need to both ascertain the short-term economic consequences that will manifest over the coming months and identify those investment opportunities that could benefit our client portfolios over the next five to 10 years. Coronation’s bottom-up, valuation-driven research process aims to identify those assets that are mispriced for the underlying risks and that have a sufficient margin of safety. In the context of South African fixed income assets, we have reassessed our fundamental assumptions coming into this crisis in terms of what the unfolding situation means for these assumptions, how thisfilters into our asset valuations, and finally, how we position the portfolios in response to these changes.

OUR PORTFOLIO POSITIONING COMING INTO THE CRISIS

Pre-Covid-19, our key assumptions were that inflation in South Africa would remain under control (5% average), growth would remain subdued (0.2% for 2020 and 1.1% for 2021), and that government finances would remain constrained, but that the problems were being adequately addressed. We had expected interest rates to move lower by 50bps-75bps in order to provide some offset to fiscal tightening and to lend support to growth.

Against this backdrop, we viewed nominal government bonds as attractive, specifically in the longer end of the curve; inflation-linked bonds (ILB)s in the two- to five-year area were offering good value relative to nominals and cash; and certain counters within the listed property space seemed reasonably attractive. We were very cautious on corporate credit, as we did not believe that valuations accurately reflected the higher risks associated with slowing growth. This was evident in the increased restructuring and probability of default on loans (credit loss ratios increased in the most recent bank results). Credit spreads compressed aggressively over the past 18 months due to a reduction in supply and a reach for yield by non-traditional credit investors. In our view, this made the asset class very expensive and, hence, unattractive. Our portfolios therefore had a neutral allocation to government bonds with duration focused in the longer end of the curve, a moderate allocation to ILBs, a historically low allocation to selected listed property stocks and a low allocation to select corporate credit.

UNDERSTANDING THE IMPACT OF COVID-19

The Covid-19 crisis has been likened to the Great Depression of the 1930s, due to the expected effects on global growth. Global GDP declined by 27% during the course of the Great Depression, which lasted just under four years. Global growth is expected to decline by a similar magnitude in the second quarter of 2020 alone. It is the containment measures taken by governments around the world to mitigate the impact of the virus that have caused turmoil in financial markets, as they try to assess the economic consequences of such actions. During March, the ALBI was down 9.7%, ILBs were down 7.1%, listed property was down 36.6%, and the rand was down 12.3% against the US dollar.

One of the big learnings for authorities from the Great Depression and the GFC is the need to act quickly, lest markets lose confidence and the crisis blows up. Global authorities have responded very quickly by dropping interest rates back to zero and committing to large quantitative easing (QE) measures (much greater than those seen in the GFC). In addition, many developed markets have already committed to fiscal spending ranging anywhere from 2% to 10% of GDP, in order to soften the growth slowdown and foster a stronger subsequent recovery.

SOUTH AFRICAN GOVERNMENT BOND MARKET LIQUIDITY DRIES UP

South African assets reacted in lock step with the global risk aversion sell-off. However, South African government bonds (SAGBs) have been exceptionally volatile during this period and sold off materially. Next to cash, government bonds are the most liquid part of a portfolio. In times of crises, when cash is often required to meet margin calls on less liquid assets and to satisfy redemptions, government bonds are used as the natural funding source. The aggressiveness of the sell-off in global risk markets and the outflows globally from emerging market bond funds have meant that foreign investors into the local bond market have had to sell their holdings for this exact purpose. This created the first leg of the sell-off in our bond market. In addition, we saw the liquidity in the interbank market evaporate, as local banks (the sole intermediaries of SAGBs) pulled back on risk-taking due to reduced liquidity conditions. In times like these, banks prefer to limit the cash lent in the interbank market and utilised in trading activities in financial markets, primarily to support their corporate and individual customers who may have funding and operational needs. This propagated the irrational market behaviour we have witnessed over the past few weeks. The SARB played a crucial role by stepping in and injecting liquidity into the market, restoring some calm. This included offering term repos on SAGBs and buying SAGBs in the secondary market.

MOODY’S DOWNGRADE TO SUBINVESTMENT GRADE

Moody’s Investor Service downgraded South Africa to subinvestment grade on 27 March 2020, a day after we went into lockdown. This is not a new development and has been well flagged by the market for a few years. As suggested in previous articles, offshore investors have been decreasing their holdings of SAGBs for some time now, and the South African sovereign spread already trades at levels consistent with subinvestment-grade debt. Additionally, we have seen the South African risk premium steadily increase, suggesting that even before the onset of Covid-19, the downgrade was already significantly priced in. The one thing that has changed is that market volatility has increased and liquidity in the secondary bond market has decreased. This suggests that the mandated selling of SAGBs might result in a more significant move than initially anticipated. However, the FTSE, which administers the World Government Bond Index (WGBI), has allowed up to the end of April for funds to rebalance, which won’t stop the selling but will allow it to be more gradual (previously, funds would have had to rebalance by the end of March).

In addition, with the SARB announcing its willingness to purchase SAGBs in the secondary market, the effect of this will be dampened. The more important question is whether this weakness represents a great buying opportunity, or whether fundamentals have shifted to such an extent that a more significant risk premium for SAGBs is justified.

CHANGES TO FUNDAMENTALS

The Covid-19 crisis is still evolving, with many unknowns. Key is the length of time that nations will remain in lockdown and the subsequent economic disruption. This uncertainty is clear in market volatility and the decline in risk appetite. However, there are a few key conclusions that we can draw at this point. First, inflation and growth will be lower than our previous expectations. We expect inflation to average below 4% in South Africa over the next two years. This is due to the slowdown impact from Covid-19 and the lower oil price. Growth in 2020 is likely to be anywhere from -4% to -7%, rebounding to just over 3% in 2021. The initial response of the SARB was to cut rates by 125bps in March. We said then that they had room to move policy rates another 100bps lower to 4.25%, which they subsequently did in an emergency Monetary Policy Committee meeting on 14 April. This will reduce the real yield materially but still keep it in positive territory, which would still compare favourably to the negative policy rates prevalent in most of the global developed economies. Unfortunately, given South Africa’s poor fiscal starting point and now negative growth expectations, it is very likely that the debt-to-GDP ratio will increase towards 80% and the fiscal deficit will widen to between -8% and -10% of GDP.

Compounding this problem further will be the need for government to provide more fiscal support to aid the economy through these trying times and any additional support for ailing State-owned enterprises such as Eskom. On the positive side, however, lower growth implies lower energy intensity, giving Eskom time to deal with much-needed maintenance. We are hopeful that this situation allows for more drastic measures to be taken at Eskom in order to rectify its financial and operational position.

In many historical instances, crises are what necessitate change. South Africa has been plagued with a slow policy response to its many structural issues. However, the pragmatic approach to the current crisis will hold leadership in high esteem when we finally emerge from it. In an uncertain world, in an economy that has lost all hope, if the leader-ship used this crisis to make the necessary hard decisions, the country could very likely emerge stronger post-Covid-19. However, as investors, we cannot bank on hope and must instead ensure that we position our clients’ portfolios for the risks and opportunities that are arising.

THE VALUATION OF SOUTH AFRICAN GOVERNMENT BONDS REMAINS ATTRACTIVE

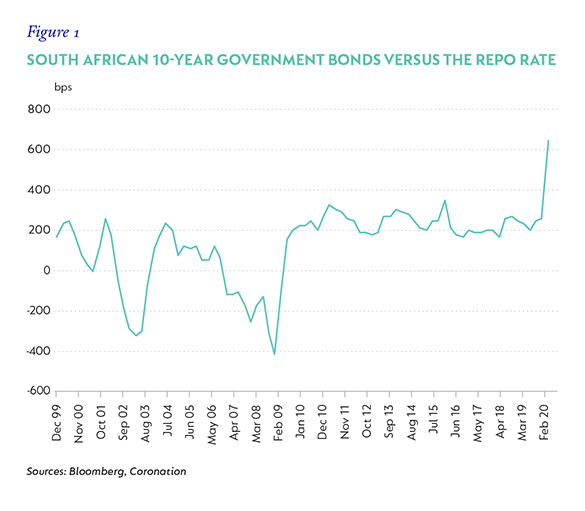

10-year SAGBs currently trade at a yield of 11% compared to cash, which we expect to be around 4.25% by the end of this year. The spread between SAGBs and cash is at the widest it has been since the start of inflation targeting (2001) and implies that 10-year SAGBs can sell off 125bps over the next year before they start to underperform cash (refer to Figure 1). In addition, with inflation expected to average close to 4% over the next two years, the implied real yield on the 10-year SAGB is close to 7%.

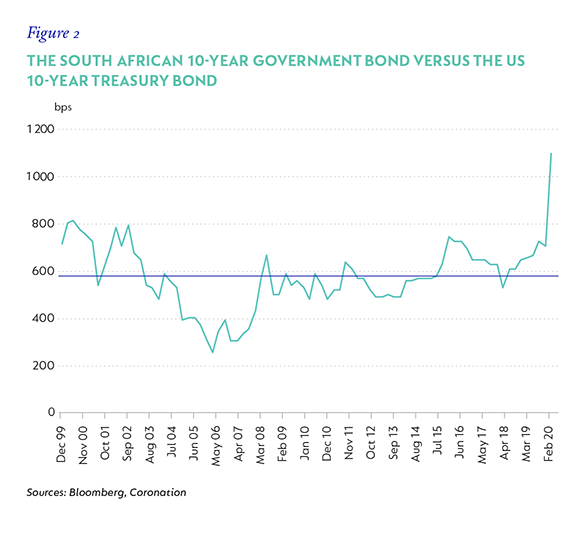

Global policy rates have moved to zero and are expected to remain there for some time to come. Several developed market central banks have restarted their QE programmes on a scale larger than those implemented during the GFC. The level of monetary policy accommodation and support that has been pushed into the global economy is unprecedented. Global developed market bonds either trade in deeply negative territory or very close to zero. 10-year SAGBs now trade in excess of 10% above developed market bonds (Figure 2).

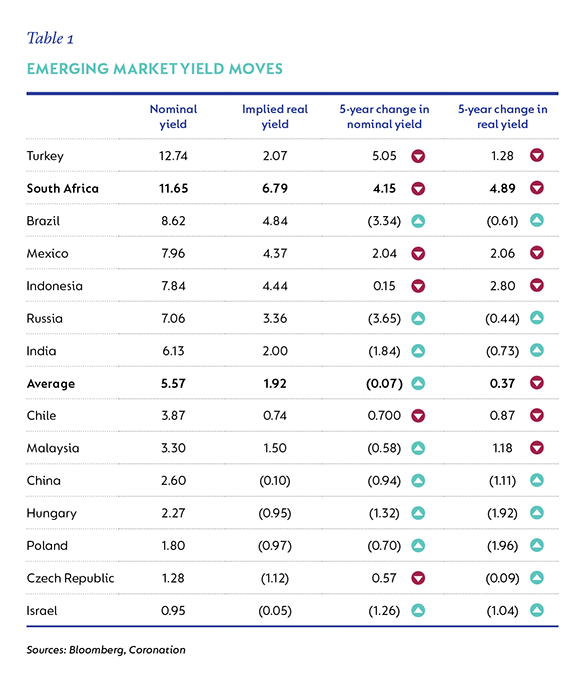

Emerging market local currency bonds have all moved weaker during the crisis, but South Africa remains the cheapest real yield and cheapest tradeable nominal yield among its peers (Table 1).

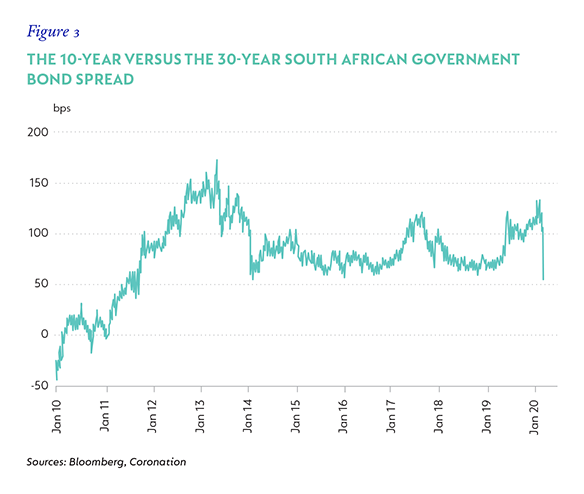

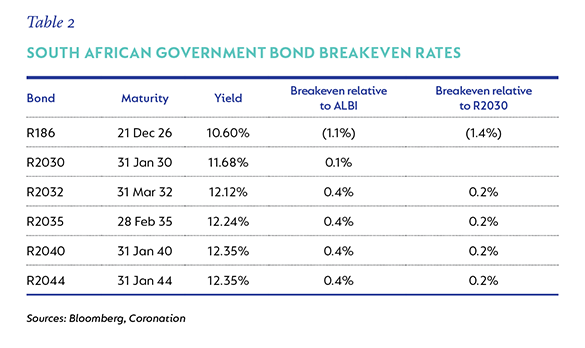

The SARB’s commitment to keep liquidity in the system and the National Treasury’s adjustment to the funding profile over this period have seen the yield curve flatten quite aggressively past 20-year maturity (see Figure 3). In running our total return calculations, we believe that bonds in the 10- to 12-year bucket offer the most value. Table 2 shows how much bonds can sell off before their return equals that of the ALBI, and how much they can sell off before they can match the return of 10-year SAGBs.

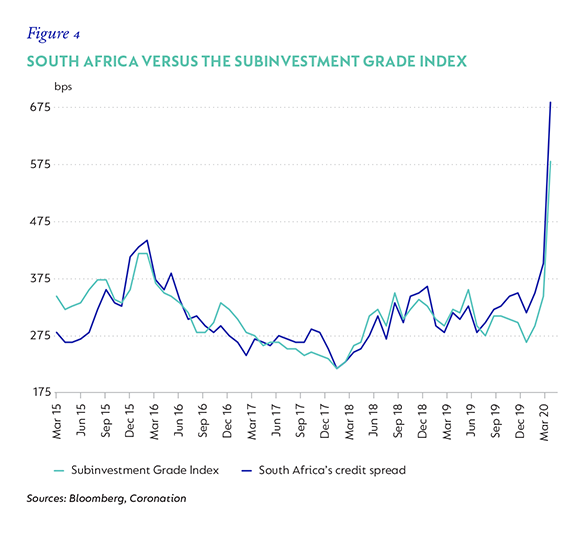

Globally, credit spreads have blown out. South Africa’s sovereign credit spread was already trading at a level consistent with other subinvestment grade countries, but is now trading 100bps wider than even the Subinvestment Grade Index (see Figure 4). Even if one assumes this is correct, the absolute level of sovereign credit spreads is very much elevated, suggesting potential room for compression.

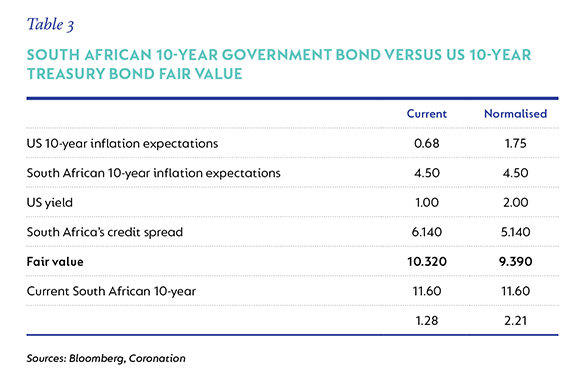

In constructing a fair value estimate for 10-year SAGBs, we use the global risk-free rate (the US 10-year Treasury Bond), the inflation differential between South Africa and the US, and the South African sovereign credit spread. In Table 3, both based off current market variables and expected values for those variables, we believe 10-year SAGBs are trading at levels 120bps-220bps above fair value. This is just one of the many models we use to determine the fair value for the 10-year SAGB, but it is the simplest and easiest to understand.

In the ‘current’ column, we have extracted all variable inputs based on current market levels, except for the 10-year SAGB inflation expectation, which we have adjusted to our expectations. In the normalised column, we assume a normalised value for the US 10-year Treasury Bond of 1.75% (down from 2.25% previously), normal US inflation of 2% (which the Federal Reserve Board targets), and a credit spread that is 100bps tighter than the current South African credit spread, in order to reflect a normalised global credit environment.

FIVE- AND 10-YEAR INFLATION-LINKED BONDS ARE ATTRACTIVE

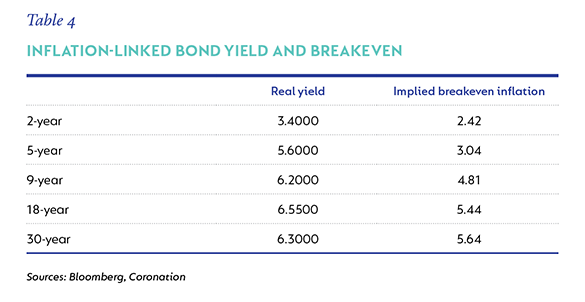

ILBs have sold off, both in sympathy with nominal bonds and due to lower inflation expectations. However, given the higher modified duration of most of these bonds, they have underperformed their nominal counterparts. In Table 4, we list a few key ILBs, their current real yield, and their implied breakeven (where inflation has to average in order for their return to equal that of the nominal bond equivalent). In five- and 10-year ILBs, real yields are close to 6%, with breakeven inflation well below 5%. We consider these to be very attractive and they warrant a healthy allocation in our portfolios.

OUR BIGGEST CONCERN IS THE LOCAL CREDIT MARKET

Fundamentally, we believe that South African corporate credit spreads should already have been under pressure, given the poor economic fundamentals of the country and the clear evidence that the probability of default for most borrowers is on the rise. A clear indication of this was shown in the rising credit loss ratios reported by all our local banks during their last updates. However, there has been a drop in corporate issuance due to the poor growth backdrop and the lack of the funding needed by banks and corporates (due to the lack of investment in the country). Leading into the crisis, with issuance lower and a reach for yield in the local market spurred by the reduction in the return expectations of many other asset classes, local credit spreads compressed aggressively.

The economic fallout of the Covid-19 crisis will add further stress to the balance sheets of all South African companies, hence lowering their credit quality. As such, it is reasonable to expect a widening of credit spreads just based on the fundamental deterioration. Add to this the repricing we are seeing in global credit markets, the drop in risk appetite, an acceleration of redemptions from fixed income funds in lieu of cash and a tightening of credit spreads over the last 12 months, and one can easily see that this is a market that needs sobering.

Coronation’s bottom-up, valuation-driven credit research process takes both fundamentals and liquidity into consideration in its assessment of risk and return. This ensures that we build a level of conservatism into our pricing expectations to deal with the illiquid nature of certain assets. In addition, liquidity plays a vital role in our portfolio construction process.

Over the last 18 months, we have endeavoured to reduce our exposure to listed credit by reducing our exposure to new style bank subordinate debt (AT1 and AT2), certain bank senior issues and not actively purchasing new issues in the primary market. Our current holdings of credit instruments are shorter dated in nature, predominantly issued by the big four banks and are listed on the JSE, making them tradeable in some part.

Credit spreads globally have widened tremendously. The credit spreads of South African companies that issue offshore debt have widened. The Sasol two-year bond trades at a yield of 22% in US dollars, and Standard Bank and First Rand Limited Tier 2 sub-debt bonds now trade at yields of 10% in US dollars. In the local market, however, these bonds have not re-marked at all, with Sasol two-year debt still marked at 134bps over Jibar (6.8% all-in yield) and the banks’ four-year sub-debt still marked at 250bps over Jibar (8.1% all-in yield).

These bonds are generally illiquid and are held by local institutions. We expect them to only re-mark in the secondary market when they are sold. We view it as just a matter of time before we see a significant re-mark in these debt instruments as redemptions intensify and forced selling pushes spreads to levels like those seen in the offshore market.

LISTED PROPERTY LOOKS CHEAP AT FACE VALUE, BUT YOU NEED TO LOOK UNDER THE HOOD

The South African listed-property sector has grown tremendously over the last 10 years into a meaningful part of financial markets, with a market capitalisation of almost R300 billion. However, not all listed property companies are equal. Each one has varying exposure to different sectors (retail, office and industrial), varying underlying asset quality and varying financial constraints. In the last five years, many have chosen to diversify away from South Africa and enter highly leveraged plays on offshore property. This has resulted in a general rise in balance sheet risk across the sector.

The current crisis will reduce rental income, put pressure on asset values, increase the cost of borrowing for lower quality businesses and test inexperienced management teams. It is entirely possible that most of the companies will require additional capital and that dividends are suspended to preserve capital. Currently dividend yields are eye-watering, touching close to 30% in some of the large-cap names.

However, one must be cautious not to take these at face value and understand how the key issues mentioned above affect that yield. We believe there are a few select large-cap counters that satisfy our stringent conditionality. These include Growthpoint, Liberty Two Degrees and Redefine. These are all counters in which we currently have holdings across our multi-asset portfolios and in which we would take more meaningful stakes in time to come.

POSITIONING OF PORTFOLIOS

We view 10-year SAGBs as the most attractive asset in the fixed income suite, with five- to 10-year ILBs coming in a close second. Listed property looks attractive, but allocations need to be made on a stock-specific basis, with careful consideration paid to the issues outlined above. Credit markets are very unattractive, and we would wait for a significant widening in credit spreads before allocating more capital.

Given the compression in the 20- to 25-year area of the curve relative to the 10- to 12-year area and risks from further fiscal deterioration, we are switching our longer end bond (20- to 25-year area) exposure into the 12-year area of the curve. We would look to increase duration into weakness but are tempered by current volatility and pending outflows as a result of WGBI expulsion. Therefore, we would be more measured in our approach to adding duration.

ILBs are attractive, and we would look to further increase our holdings in the five- to 10-year area into weakness. These instruments carry a higher modified duration and are more illiquid than nominal government bonds. As such, we will be even more cautious in our approach to adding exposure.

We will not be adding any credit to our portfolios until we view spreads as cheap relative to our fundamental assessment, and would instead use the little credit that we have, given that it is shorter dated, as a funding source for the other more attractive asset classes.

The key lesson from 2019 was not to underestimate the degree to which lower economic growth hurts property companies. This time, the problems are more severe, dividends could be suspended and a 30% yield could be zero. For now, we are not actively looking to add to our property holdings and are comfortable with our historically low allocation. There are very few counters that offer value and we will add to these at levels that we believe offer a large margin of safety, especially given the attractiveness of SAGBs and ILBs.

We remain committed to only adding assets to our clients’ portfolios that we believe offer a sufficient margin of safety and are adequately priced for the underlying risk. We are constantly on the lookout for valuation dislocations relative to fundamentals, which we believe will benefit our client portfolios over the longer term. In this volatile period, asset price behaviour tends to be irrational, which will adversely affect short-term performance. It is during times like these that once-in-a-lifetime opportunities present themselves, and one has to stand ready to act with conviction to take advantage of these opportunities.

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter