South Africa - Institutional

South Africa - Institutional

Investment views

South Africa’s power conundrum

- What is needed to reverse South Africa’s power crisis is focused and united action by all stakeholders.

- Rather than being the solution, Medupi and Kusile power stations are a damp squib.

- Crippling municipal debt has resulted in a 10-year bailout plan by National Treasury.

- South Africans will eventually decrease their dependency on the SOE, but after how much pain is unclear.

Eskom is always a contentious topic to discuss, with the very mention of its name causing anguish and frustration for most South Africans. Since 2007, Eskom’s 10 different CEOs have been unable to successfully address the issue of load shedding. And despite the appointment of various task teams, clarity about the problems facing Eskom and the steps required to solve them remains elusive. This is further inflamed by the alleged corruption highlighted through the likes of the Zondo Commission (as well as the R20.7 billion of reported irregular expenditure) and the failure, as yet, to hold anyone legally accountable. However, it is important that we do not let the facts be clouded by emotion and politics. The problems facing Eskom are complex and it is important that all stakeholders remain focused on finding a solution.

Prior to 2007, when load shedding became a ubiquitous term in South African households, government had already been warned of the impending energy crisis. They chose not to act, and this led to former President Thabo Mbeki apologising in December 2007, with the admission that “Eskom was right, and the government was wrong”. This put into motion the construction of mega power stations Medupi and Kusile, which together were to contribute an additional 9 600 megawatt (MW) of generation capacity to the national grid. However, what was to be Eskom’s saviour has become its biggest liability, as the complexity and challenges of these projects have proved to be vast. Time delays, cost overruns and poor contractor performance, as well as allegations of high levels of corruption, resulted in the cost estimates for Medupi alone ballooning from a reported R69.1 billion in 2007 to current incurred costs of R145 billion – double the budgeted amount. The final cost to completion is still unknown and recent reports of design flaws mean that substantial further expenditure is likely required to make the plant viable.

SUPPLY CONSTRAINTS

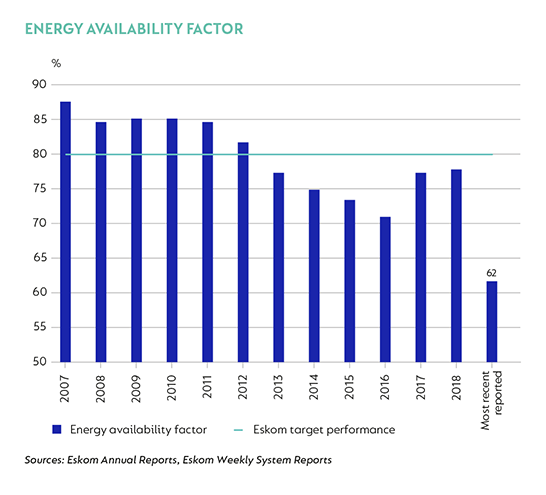

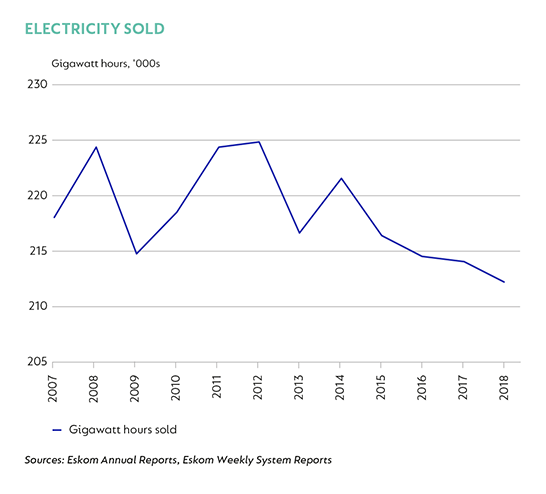

Ironically, growth in electricity demand is no longer an issue for Eskom, as electricity sales have fallen over the last 10 years due to consumption having become more efficient. The problem today is different – Eskom has the capacity to meet demand but is unable to do so because of units that are either being maintained or have stopped working after years of lack of maintenance. Eskom currently has 46 000 MW of installed capacity, but with the energy availability factor[1] hovering around 62%, only 28 000 MW seem to be available. Unfortunately, trying to estimate when the situation will improve is a challenge, and Eskom needs time to perform the required maintenance. On this basis, our view is that load shedding will remain a reality for the foreseeable future. In fact, one could say that load shedding is needed to remedy the situation, providing it is efficiently scheduled and properly communicated.

FINANCIAL WOES

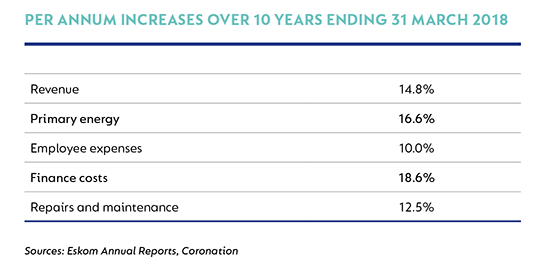

Unfortunately, Eskom’s generation challenges are not being helped by its precarious finances. The Eskom revenue model should be straightforward: it sells electricity for a price regulated by NERSA[2], and this should be enough to cover the costs required to generate that electricity, together with a modest return. But the tariffs are granted on assumed levels of expenditure, and this is where the model has failed. Costs, particularly on energy and interest, have grown significantly faster than revenue, capital expenditure on Medupi and Kusile continues to increase above budget and a culture of non-payment has started to develop among some of Eskom’s larger customers. To complicate matters further, the financial pressures have meant that Eskom has reduced expenditure on repairs and maintenance, a decision which has had a significant impact on the performance of its fleet of power stations. The extent to which this underinvestment extends to Eskom’s other divisions, such as Transmission, is another concern which could lead to further financial stress in the future.

FUELLING THE FIRE

Eskom relies on coal as its primary fuel source. This was traditionally obtained from Eskom mines located adjacent to coal power stations in Mpumalanga. Over the years, Eskom has not invested in these mines, resulting in their productivity falling and additional coal having to be procured and transported from independent coal suppliers at a significantly higher cost. In times of crisis, Eskom has also resorted to using its open cycle gas turbines (OCGTs), which are exceptionally expensive due to their high consumption of diesel. During the 2014 financial year, Eskom spent R10.5 billion on diesel, and it is likely that diesel costs will be elevated while the system remains under pressure. It also bears remembering that the OCGTs were designed to be used as a temporary backup, not to run 24/7, and this is likely to result in significant wear and tear on these generators as well.

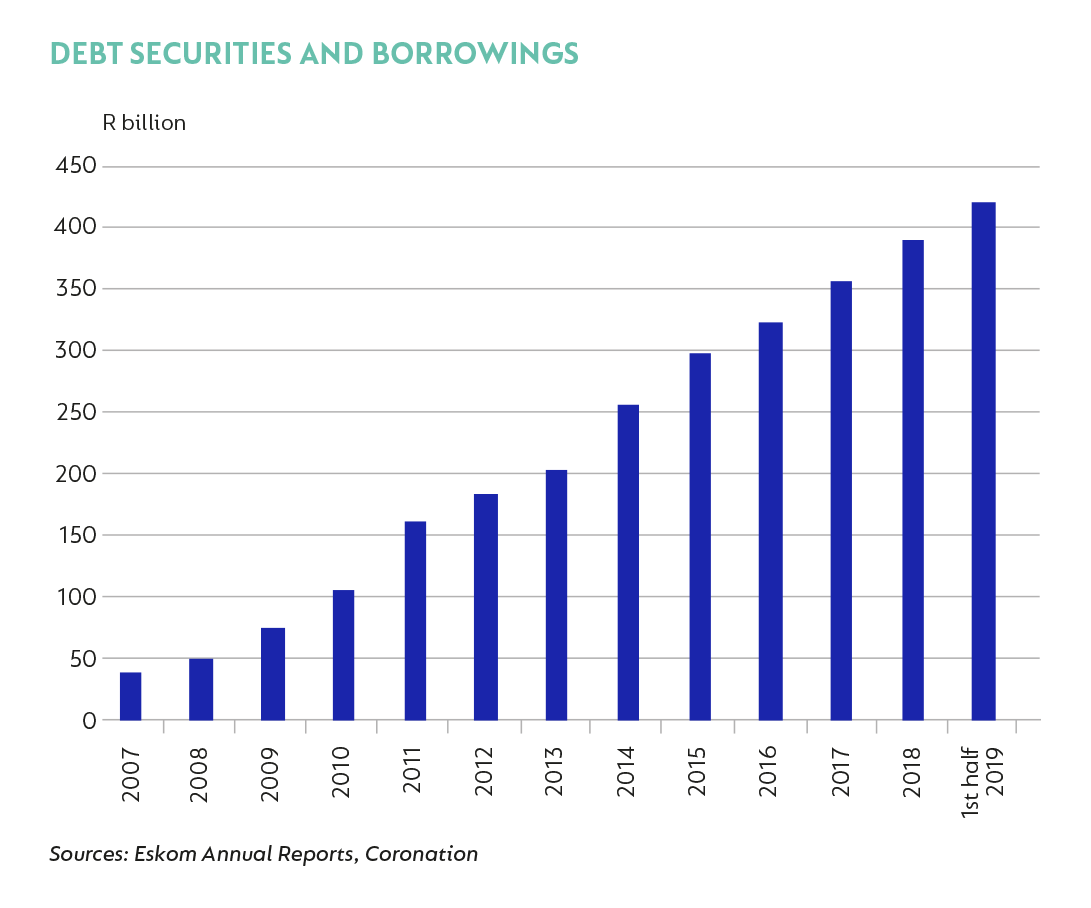

In addition, Eskom’s debt burden has increased to R419 billion, of which R336 billion is under government guarantee. To put this into context, this full debt balance equates to around 9% of South African GDP. The interest required to service this debt is significant, and in Eskom’s most recent half-year report, the R26.6 billion of operating cash flow that it generated was quickly absorbed by interest costs of R17.7 billion and capital investments of R17 billion. The deficit was, of course, financed by more debt, and so the vicious cycle continues. Lower levels of revenue collectability are also pressuring cash flows. As at 30 September 2018, Eskom had invoiced municipal arrears debt of R17 billion, which excludes Soweto’s arrears debt – which, at R12.6 billion is worth a separate mention. This issue is unlikely to be resolved without government support and commitment to ensure consumers pay for the electricity they use.

BAILOUT

To assist Eskom with its financial predicament, government has committed to injecting R23 billion annually into the entity for the next 10 years. In addition, NERSA recently granted the entity a 13.8%[3] tariff increase for its 2020 financial year, with 8.1% and 5.2% increases stipulated for the subsequent two years. In our view, this is unlikely to be enough, and Eskom together with its stakeholders will need make difficult decisions to reduce costs going forward. The recently appointed Eskom CEO Phakami Hadebe and the Chairman of the Board Jabu Mabuza have both been shown capable of turning around struggling entities in their previous roles at the Land Bank and Telkom, respectively. However, Eskom is a political minefield with many vested interests at play, complicating any potential restructuring and turnaround plan.

SO WHERE TO FROM HERE?

As a first step, government has proposed to unbundle Eskom into three separate units – generation, transmission and distribution. This concept is not new and has been proposed several times over the last two decades. More importantly, however, this model is more in line with international standards and has also been followed by other African countries. The benefits are simple: each division can focus on its own revenue and costs, thereby driving efficiencies and improving accountability and governance. But perhaps the most important benefit for the public will be the associated improvement in price transparency and competition. While not an immediate solution to load shedding, allowing multiple participants to be involved in the broader energy market should, over time, improve the integrity and resilience of the electricity system. In our view, unbundling is certainly a step in the right direction, but achieving it will not be easy.

Creating new legal entities and transferring existing assets to them will take time, and additional costs will have to be incurred. Furthermore, there is the question of what Eskom does with its enormous debt burden and how, if at all, this is allocated to the newly separated entities. Government and NERSA also need to move quickly to ensure that the legislative and regulatory frameworks are in place to allow reform to happen.

One way or another, the market will solve the electricity crisis, and the role of Eskom as the sole provider of electricity will diminish. How much more discomfort South Africans will endure before this happens, however, is a question that ultimately only government can answer.

[1] A measure of the amount of time that a plant is available to produce electricity.

[2] National Energy Regulator of South Africa

[3] A 9.41% tariff increase together with a 4.4% regulatory clawback.

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter