South Africa - Personal

South Africa - Personal

Personal finance

Would investing be painless if you had perfect foresight?

Unfortunately not, our analysis shows

The Quick Take

- Short-term market volatility is inevitable

- Even having perfect investing foresight won’t help you to side-step portfolio drawdowns

- A hypothetical portfolio of only guaranteed winners shows that it too had to navigate meaningful drawdowns that took long to recover from

- Volatility is the price of admission for successful long-term investors

Consider a scenario in which you have perfect foresight and only invest in the shares that you know will perform well. Would it remove all the pain associated with investing? Would your portfolio deliver a smooth path to inevitable outperformance? Interestingly, the answer is no.

CREATING THE PERFECT FORESIGHT PORTFOLIO

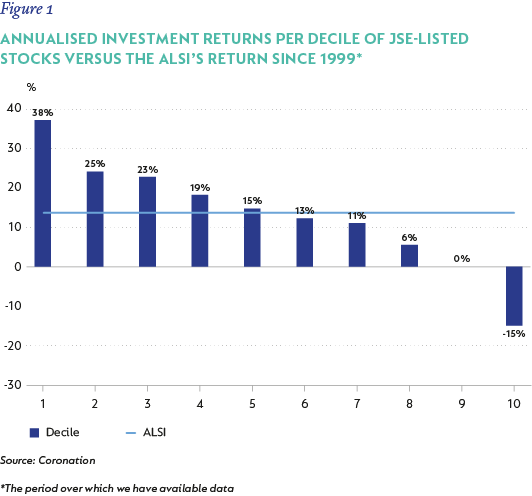

Imagine a South African equity fund that is guaranteed to only invest in the top decile of stocks listed on the JSE over a five-year period (commonly accepted as the minimum investment horizon for a long-term growth portfolio). Let’s call it the Perfect Foresight Portfolio (PFP). The PFP resets every five years and, incredibly, repeats this feat over and over again. Naturally, this is completely unrealistic, but the hypothetical outcome would be incredible returns. Since 1999, the PFP would have delivered 38% p.a. compared to an annualised return of 14% from the FTSE/JSE All Share Index (ALSI). In other words, an allocation to the ALSI would have resulted in 20 times your initial investment (whatever that amount may have been) – which is a very respectable outcome. However, the PFP would have resulted in 164 times your initial investment – clearly very impressive to even the most demanding investors among us.

THE PRICE OF ADMISSION

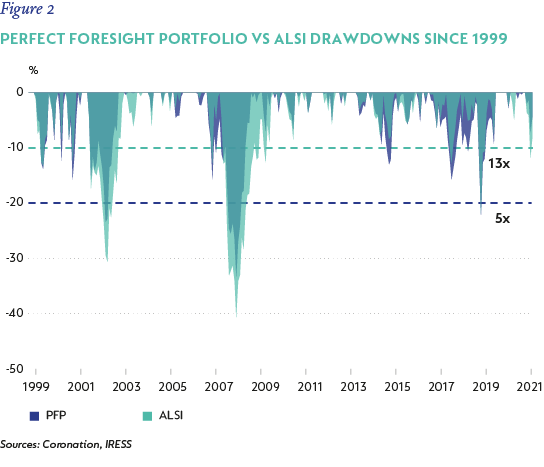

While the end result for the PFP is undeniably impressive (yet highly unachievable in reality), what’s more revealing is the journey that investors had to embark on to get there. Volatility is often viewed as something that should be avoided in investments; however, successful investors understand that it is the price of admission. The following chart compares the drawdowns of the PFP with that of the ALSI.

It is clear that the PFP’s drawdowns, over time, were not too dissimilar in magnitude than those of the local market. In fact, there were many periods where the PFP’s drawdowns were larger, with investors having to stomach portfolio value declines in excess of 10% on 13 separate occasions; five of which exceeded 20%.

EVEN GUARANTEED UPSIDE COMES WITH DOWNSIDE

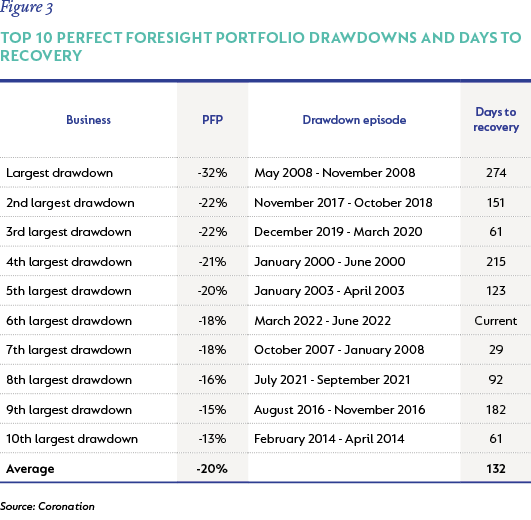

A closer look at the 10 biggest drawdown episodes for the PFP reveals both the severity and the path to recovery. Even a portfolio that invests in guaranteed winners produced no less than 10 drawdown episodes that resulted in an average drawdown of -20% and took, on average, 132 days to recover those losses from the bottom of each drawdown.

One can imagine that the portfolio manager of the PFP would have had to face regular pressure from disgruntled clients – some of whom would, in all likelihood, have withdrawn during the more severe drawdown episodes.

Although purely hypothetical, this exercise does solidify an essential maxim of investing: short-term market drawdowns are inevitable for investors pursuing long-term growth. But the ultimate reward for staying the course will be well worth the discomfort in the short term.

This article was inspired by Wesley Gray’s study first published on alphaarchitect.com in February 2016.

Disclaimer

SA retail readers

SA institutional readers

Global (ex-US) readers

US readers

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter