South Africa - Personal

South Africa - Personal

Investment views

South African bonds attractive in a low-return world

But depressed growth and further Eskom support weigh heavily on government

- We’re still far from seeing a restart of the US QE programme, given the room to move lower on policy rates

- SAGBs have a very limited margin of safety against a turn in global sentiment

- SA will likely be downgraded to subinvestment grade territory by Q3-20

- SA bonds look fantastically attractive and relatively cheap to dollar-based investors

AN ASTONISHING $15 trillion worth of global government bonds now trade at a negative yield. That’s approximately 25% of the market that is trading with a yield to maturity of less than zero. This phenomenon, for now, has been confined to Europe and Japan, and in extreme cases like Switzerland, Germany and the Netherlands, the entire yield curve trades in negative territory (negative yields all the way out to 2050!).

Any intelligent person would ask the question, who in their right mind would be investing in an asset that is guaranteed to lose them money? In a world where the alternatives are overpriced risky assets, where one can suffer permanent loss of capital, or negative cash/deposit rates, suddenly assets at less negative yields and that have consistent buyers in the form of central banks (which makes short-term capital gain possible), look a whole lot better.

In a world of no yield, one would expect relatively high-yielding assets to be well supported. Since the beginning of the year, emerging market (EM) bonds, returned 12.1% in US dollars. This is despite many EM currencies being down considerably (3%-7%) over the last quarter.

South African bonds scraped in with a positive return of 0.74% this last quarter, but over the last 12 months the All Bond Index has delivered an impressive return of 11.4% in rand, which, despite the 6.5% depreciation in the currency over the same period, still produced a positive return of approximately 5% in dollars. Over the last quarter, the South African 10-year bond has traded in the 8.50%-9% range, with the further rally in global bond yields acting as a strong anchor for local yields.

The US 10-year bond has rallied from levels of just above 2% to 1.67% over the course of the quarter, for several reasons. The escalation of tension in the US-China trade relationship has dented global confidence, which has led to a material slowdown in the global capex cycle. This has coincided with a slowing in US and global growth. Central banks have been quick to step in and engineer a softer growth landing, with the US reducing interest rates 0.5% this year and the European Central Bank moving deposit rates further into negative territory, accompanied with a restart of its bond purchase programme.

Current data emerging from Europe point to growth slowing to 1% with inflation of 1.5%, which suggests, at a bare minimum, a continuation of accommodative monetary policy in the EU. US data, more specifically the US labour market, have proved more resilient, despite recent cracks starting to appear.

The reaction of the US Federal Reserve Board has not been as frantic as market pricing of interest rate cuts and has instead adopted a wait-and-see approach to further rate easing. We are still quite far away from seeing a restart of the US quantitative easing programme, given the room to move lower on policy rates. The hope is that recent measures implemented by global central banks are enough to mitigate an aggressive growth slowdown in the months to come.

On the local front, we remain in limbo as we await the Medium-Term Budget Policy Statement at the end of October and further details on the turnaround for Eskom. Inflation continues to be well behaved and expectations are for it to average 5% over the next two to three years.

Growth expectations have been continually revised down, with current expectations for a marginal pick-up to 1.5% over the next two to three years. Structural reforms have been much talked about, especially in the new National Treasury economic strategy plan released by Finance Minister Tito Mboweni towards the end of the third quarter. Unfortunately, time is running out, and what’s needed now is an accelerated implementation of these initiatives to bring back confidence and investment into the local economy.

Government finances continue to weigh heavily on the local outlook, with the fiscal deficit expected to breach -6% this year and debt/GDP to push above 60%. The major culprit of this deterioration has been the continued support needed by ailing state-owned entities (SOEs), most specifically Eskom. Without a credible plan to turn around the entity, more money will need to be poured in to allow it to meet its obligations. Herein lies the major risk for the local economy, and while there has been an acknowledgement of the problems by government, there has been a lack of urgency in putting a credible plan in place to halt Eskom’s deterioration, let alone turn the entity around.

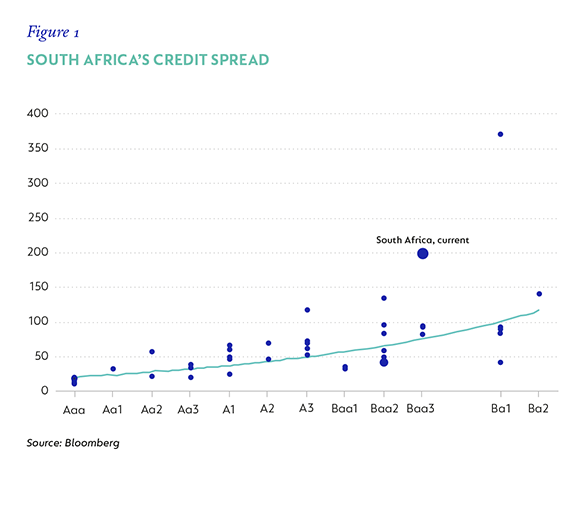

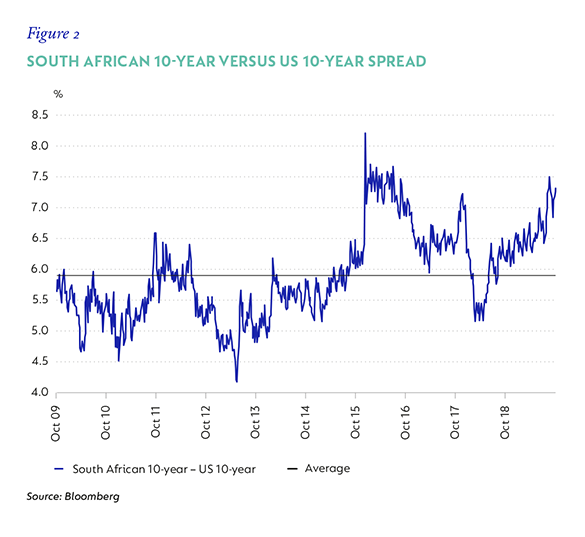

Moody’s is still the only rating agency that rates South Africa as an investment-grade country and has provided the country with a tremendous amount of leeway over the last 12 months. Its recent statements suggest that it will continue to do so, given the reform intent of government. However, given what is currently known about the trajectory of further deterioration, if there are no substantial efforts to fix the problems the country faces, it is very likely that South Africa would be assigned a negative outlook on our investment grade rating by November 2019 and downgraded to subinvestment grade territory by Q3-20. The deterioration in South Africa’s fundamentals has been well flagged, which has allowed a risk premium to be built into South African government bonds (SAGBs), both in terms of absolute yields and the steepness of the yield curve. South Africa’s credit spread (represented in Figure 1 by South Africa’s credit default spread) already trades at levels that are consistent with a subinvestment peer group. In addition, 10-year SAGBs trade at a spread of 7.25% over US 10-year yields, which is well above the long-term average and close to the widest levels they have been in 10 years (refer to Figure 2). These measures suggest a decent amount of the bad news is already being priced in by markets.

Furthermore, SAGBs look quite cheap when compared to the EM universe. In Table 1 we show the nominal yields of various EM bond markets and their implied real yields (the return one would get if we stripped out the effects of inflation over the next year). South Africa not only sits well above the EM average but also at the top of the ranking table when it comes to the relative cheapness of nominal and real yields. In a world of very low to zero yields, South African bonds look fantastically attractive and relatively cheap to dollar-based investors.

As a dollar-based investor, when one invests into a local currency bond market, there are two major risks that one takes. First, you take the risk that the yield at which you are investing does not offer a sufficient margin of safety in the event of further local fundamental deterioration, and secondly you are taking the risk that the currency depreciates to such an extent that it wipes all the yield from the bonds.

The first risk is something that we have discussed at length in the past. We construct a fair value for 10-year SAGBs, using the expected global risk-free rate (US 10-year), expected US/South African inflation differentials and the South African credit spread. We use values of 2% (normal US 10-year rate), 3.8% (5.3%-1.5%; South African 10-year breakeven minus US 10-year breakeven) and 3.16% (South African EMBI plus sovereign spread) to arrive at a fair value of 9.03%, which is not far from current levels of 8.92%. This suggests that SAGBs trade pretty much at fair value, implying not much room in the case of further fundamental deterioration.

Dollar-based investors have the option of buying 10-year South African bonds issued in dollars, currently trading at 4.88% with no currency risk, or buying a 10-year SAGB issued in rand trading at 8.92%. If you do not expect the currency to move, then it’s a no-brainer to buy the bond issued in rand due to the higher yield on offer. Over the last 20 years, the rand has depreciated by an annualised rate of 4.4%. The annual depreciation would comprise inflation differentials and a risk premium. Since South Africa runs a higher inflation rate than the US, the rand has to deteriorate by a minimum of the inflation differential for purchasing power between the two countries to remain unchanged. The more unpredictable part is the risk premium that needs to be priced due to the risk of deterioration in other local factors. Over the last 20 years, the inflation differential between South Africa and the US has been 3.4% (5.6%-2.2%: actual inflation outcomes), suggesting the risk premium should be 1% (4.4%-3.4%).

Current inflation differentials sit at 3.8%, which makes the 20-year annualised depreciation of 4.4% look reasonable, as we assume a reduced risk premium going forward. This implies that a dollar-based investor can expect a return in dollars of 4.52% (8.92%-4.4%). Compared to the actual South African 10-year dollar bond, this is not that attractive, unless one has a materially positive view on the currency. It would also explain why the local South African bond market has experienced outflows this last year of approximately R8 billion. This is a big turnaround from the R20 billion of inflows we were sitting with at the end of the first quarter of this year.

South Africa inflation will remain benign and growth subdued, which would, at worse, allow policy rates to remain on hold. However, persistent low growth and the need for further support of

SOEs will weigh heavily on government finances, resulting in wider budget deficits and a significant increase in the debt burden. The global environment remains supportive for EM and South Africa, especially given the renewed monetary policy easing embarked on by global central banks. However, SAGBs trade at fair value at best and have a very limited margin of safety against a turn in global sentiment or a worsening in local economic conditions. Therefore, it is prudent to maintain a neutral to slightly underweight allocation to SAGBs at current levels.

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter