South Africa - Personal

South Africa - Personal

Benchmarks - October 2016

I get it. Folk in finance spend their lives putting numbers to things. We love to measure and track and record. Whole industries are built on this and it comes with its own language. It helps us feel in control and that the quality of our decisions is more measured. And arguably, it does translate into better decisions.

The rise of the investment industry’s obsession with benchmarks and the tracking thereof is a case in point. Sure, it helps consultants and fund selectors to compare a manager’s abilities, and the importance of this goes without saying. The bigger question is whether this is really the best approach, especially in a world where the very nature of benchmarks can be quite arbitrary. Too often the accepted wisdom of the use of benchmarks goes unchallenged, and too little time is spent understanding the one thing that ultimately ends up defining a portfolio.

For Coronation, the more important question investors should ask is why they are participating in the markets they have chosen.

When it comes to frontier markets, the reason supporting their investment decision should not be because they want to outperform a benchmark. Returns in some of these markets can reach large negatives, and beating a benchmark in this instance is cold comfort. By hugging a benchmark, a manager can be accused of lacking investment conviction and, quite frankly, courage.

Generally, when we make the above argument, we get accused of wanting to be rewarded for beta performance in a portfolio. Simply put, I (the portfolio manager) am trying to take credit for a general move in equity prices, rather than outperforming an equity benchmark. Nothing could be further from the truth. We believe there is far more value in trying to make sure that we focus on generating absolute returns for our investors, rather than outperforming a poorly constructed benchmark. And this is often no easy task.

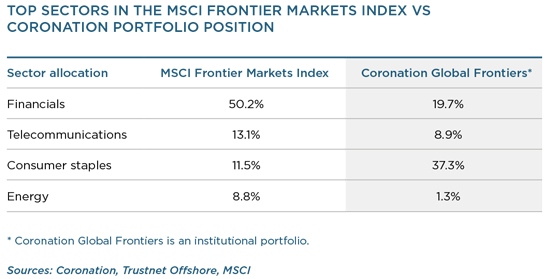

In the frontier space, the most widely used benchmark is the MSCI Frontier Markets Index, measured in US dollars. This index includes 117 constituents and covers 85% of the free float-adjusted market capitalisation in each country. Sounds like a good effort. When building benchmarks, MSCI states that a strong emphasis is on index liquidity, investability and replicability.

The key words in the above paragraph are investability and free float. These two filters have major consequences and result in a significant distortion of the index. Why does this matter? The free float refers to the percentage of ownership of stocks held by shorter-term investors. By way of example, British American Tobacco plc (BAT) owns 60% of the listed BAT Kenya. The free float is then put at 40%, and the benchmark weight of the index is downweighted accordingly.

If you do a screen of consumer stocks across frontier markets, a very common theme is that the global multinationals have beaten the investment community to the choicest consumer options. BAT, Heineken, Diageo, Nestlé, Unilever – the list goes on – all have claimed their stake in these markets. And as a result, the benchmarks receive a corresponding haircut. Banks, typically, do not have international parents. Or if they do, they have grown at a much slower rate. Banks, by their nature, issue shares as they grow. This has resulted in the free float of financial stocks being very high, and they have muscled in far greater representation in the index.

We prefer the more measured approach of investing in consumer stocks that fund growth through internal profit generation and those that come with greater comfort of an international parent. Why then would we choose to have a measurement (benchmark) that forces us to buy more of companies that display far less discipline when it comes to the use of their capital and the issuance of precious scrip? This is exactly what using the MSCI Frontier Markets Index forces one to do.

Let us take a look at how MSCI defines the space and the results thereof.

We maintain that investors who choose to put capital to work in frontier markets do so because they wish to compound their capital. They are not actively investing in what is often viewed as a risky asset class because of benchmark volatility. Accordingly, by constraining a portfolio around a benchmark such as MSCI Frontier Markets you run the inevitable risk of sizing investment positions relative to the benchmark, and not relative to the return opportunity on an absolute basis.

We are not suggesting that fund managers whose portfolios resemble the benchmark do not have a fundamental view of the position size in their respective portfolios. The only point we are trying to make is that a definite consequence of portfolios that are risk constrained against a particular benchmark is the inclusion of positions that are merely the result of benchmark referencing.

You should not own a frontier stock just because it happens to be large in a frontier markets benchmark. And constraining a frontier markets portfolio manager to a benchmark risks unintended consequences that will be in direct contradiction to the original reasons for choosing to invest in frontier markets.

As active, bottom-up stock pickers, we view this akin to zombie investing, and would rather avoid carrying dead money in our portfolios.

Coronation Global Frontiers is an institutional-only portfolio. Another institutional portfolio, Coronation Africa Frontiers, is managed by the same team and included as an underlying holding in our multi-asset funds such as Coronation Balanced Plus.