South Africa - Personal

South Africa - Personal

Odontoprev - October 2016

With 6.3 million members, OdontoPrev is the largest private dental insurance provider in Brazil, founded in 1987 by five dentists. From humble beginnings, it has grown exceptionally over the past 29 years, generating great shareholder returns since its listing in 2006 (a total return of 18.47% in US dollars per annum to date). This is a company that has delivered time and time again. We do not feel the story is finished, and expect compelling shareholder returns in future.

Some 11% of Brazilians have dental insurance, compared to 60% in the US. Brazil has the highest absolute number of dentists globally (277 000, or 12% of all dentists in the world), with the US in the second position (160 000). This is an important dynamic: the abundant supply of dentists ensures that OdontoPrev has access to an extensive network of dentists as the company continues to grow membership going forward. A testament to this reality is that its current network of 28 000 affiliated dentists is backed up by a waiting list of 25 000 additional dentists wanting to join the network. This allows OdontoPrev to grow its member base while maintaining high service levels, without the commensurate investment in capital expenditure.

Brazil’s public sector has traditionally not invested in the dental segment, contributing to one of the worst ratios of public to private dental spending globally. For the private sector, this has provided an attractive opportunity.

The dental insurance market has some favourable characteristics when compared to the medical insurance industry. Preventive dental measures are far more effective, even in elderly populations. Also, unlike other medical care, dental costs do not rise significantly with age. Dental issues are far more predictable, given that there are far fewer dental diseases than other medical illnesses, thereby reducing the range of outcomes and the risk of mistakes when developing actuarial models. The dental care business is also not so complex, or as influenced by exogenous events, as dental claims are not severe or random in general, and can be controlled through interventions. Accordingly, management quality becomes a decisive factor for the success of the business.

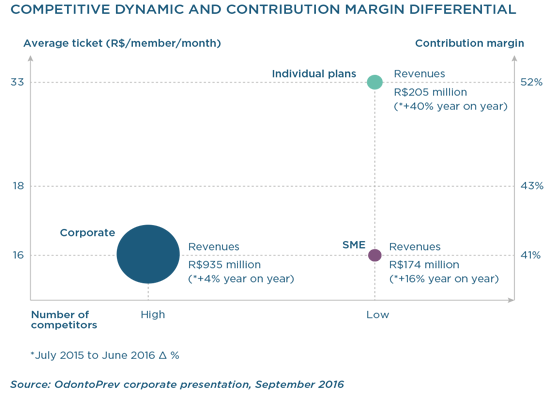

The dental insurance market in Brazil is split into three categories, namely corporate, small and medium enterprises (SMEs) and individual. Corporate members represent 76% of OdontoPrev’s current member base, followed by SMEs (14%) and individuals (10%). The large proportion of corporate members is a function of the dynamics of the Brazilian market, and also part of the company’s historic legacy. In the corporate space, you are dealing with a consolidated customer base who are pushed to take up insurance as an employee benefit. The result is a lot of competition, but with less risk of adverse selection (high-risk insurance clients), and a market whereby scale can be achieved quite quickly. This part of the market was where OdontoPrev has historically (until 2014) focused most of its attention, achieving massive success and becoming a market leader. It now has 29% of the dental insurance market share and receives 43% of the revenue (three times more than number two).

This remarkable success is testament to an excellent management team which has out-executed its peers. This was achieved through an unwavering commitment to providing value to its members, as well as nurturing relationships with dentists, ensuring both sides of the value chain were looked after.

OdontoPrev’s commitment and value offering to customers are underpinned by its proprietary IT system which has been built up over the last 29 years. It acts as a monitoring system, which links to all their dentists, thereby giving OdontoPrev oversight into each and every dental procedure carried out by its affiliated dentists. These procedures are then audited by a team of 80 dentists, who ensure consumers are not over-treated, significantly reducing waste and effectively bringing down prices for all members. OdontoPrev’s management contends that it is cheaper to have a dental plan than pay out of pocket. This is a powerful selling point that will attract future members from the estimated 78 million Brazilians currently paying out of pocket for dental care. In testament to this value offering, the company has enjoyed the highest renewal rate in the market, despite its above-average premiums.

OdontoPrev views dentists in its network as business partners rather than resources, thereby fostering long-term relationships. The specialty area of each dentist is recognised, and patients are matched with suitable dentists, thus providing great customer service and ensuring their affiliated dentists get the experience they desire. The company provides continuous education about new dentistry procedures and technologies to their affiliated dentists, providing great value to their dental network by improving their skills.

The success achieved in the corporate space has set the company up for its next wave of growth in the SME and individual market, of which only 5% has dental plans. This is a far more fragmented market with less competition owing to distribution challenges. However, this market has superior economics due to higher premiums, resulting in higher contribution margins and (notwithstanding the higher distribution costs) higher operating margins.

The distribution challenges in the individual and SME market have been identified by management and addressed through the signing of two exclusive distribution agreements with two of the largest banks in Brazil. OdontoPrev has an agreement with Bradesco (also the controlling shareholder of OdontoPrev) as well as a joint venture with Banco do Brasil (formed in 2015). Together, the agreements give OdontoPrev access to 52% of all Brazilian banking clients.

The other major sales channel is through retailers. Historically the majority of SME and individual plans were sold through retailers, which incurs commissions of 25% to 40% (while banks charge 10% to 15%), but this mix is changing. Currently 40% of all plans are sold via banks, compared to 34% a year ago, with management working actively with its banking partners to improve selling by ensuring incentives at branch level are aligned correctly. Owing to the low ticket item nature of dental plans, banks are a superior channel due to the existing sales infrastructure. This is also an attractive business for banks: no capital is required, which means it enhances its return on equity (ROE).

Within the individual and SME segment, the company offers a portfolio of more than a hundred different contracts. OdontoPrev believes greater product differentiation helps reveal preferences based on client choices and reduces the guesswork in predicting how members will access dentists. This allows the company to price according to customer needs, reducing the risk of adverse selection.

On top of all the aforementioned characteristics, the business has really delivered phenomenal accounting metrics and should continue to do so. The company generates a very healthy operating margin of 25%, which we believe is sustainable and should in fact rise owing to the increasing contribution of individual and SME plans, which have superior economics. The sustainability of an operating margin is often determined by the competitive environment, pricing power and the barriers to entry in an industry.

The pricing of dental insurance is inherently attractive: the consumer’s main goal is not achieving the cheapest dental treatment, but rather the most effective treatment administered by a trusted practitioner. This allows OdontoPrev to consistently charge more expensive rates than its competitors, and still gain market share. So while its competitors, who largely suffered from confused strategies and a lack of focus, have priced aggressively in the past, it did little to entice OdontoPrev members to move across. Moreover, an important development took place in 2009, with the merger of OdontoPrev and Bradesco Dental, which consolidated the market and added 1.3 million lives to OdontoPrev’s 2.6 million at the time.

Finally, the barriers to entry for other players are immense, especially in the individual and SME space, which represents the biggest long-term opportunity for the company. These barriers are a function of the proprietary IT system the company has built, along with the exclusive distribution agreements they have formed with major Brazilian banks.

The cash flows a business will generate in future determines its intrinsic value. The challenge is forecasting these cash flows, as the future is unknown. Accordingly, a business with a clearer outlook of its future prospects, with fewer different potential outcomes, is inherently worth more. Thanks to its annuity-type revenue from existing members, along with powerful industry tailwinds owing to the low penetration and superior distribution abilities, there is good visibility of OdontoPrev’s future revenue. Moreover, the company has put in place incentives to encourage members to pay their monthly subscriptions upfront, further enhancing visibility.

OdontoPrev’s operating margins, its limited capex requirements (less than 1% of sales) and low working capital requirements (working capital to sales of 5% on average over the last ten years), result in free cash flow generation, which is in excess of accounting earnings. Also, the reinvestment requirements of the business are limited, enabling it to pay out close to 100% of earnings each year in dividends. These qualities have resulted in the business generating an ROE of 34% in 2015, up from 18% in 2011. This should continue to rise as its incremental growth and cash generation do not require the equivalent reinvestment in the business. The biggest risk for the business is changing regulations, but we feel this risk is mitigated by OdontoPrev’s plans to provide real value to the consumer and deliver cost-effective dental care. OdontoPrev has been a holding in the Global Emerging Markets Fund for the past one-anda- half years and we believe it will remain a long-term winner, providing our clients with good returns going forward.