South Africa - Personal

South Africa - Personal

Market review - January 2017

2016 was certainly a year full of surprises! Given the backdrop of Brexit and the election of Donald Trump as the next US president, not many would have anticipated the resilient performance of global markets last year.

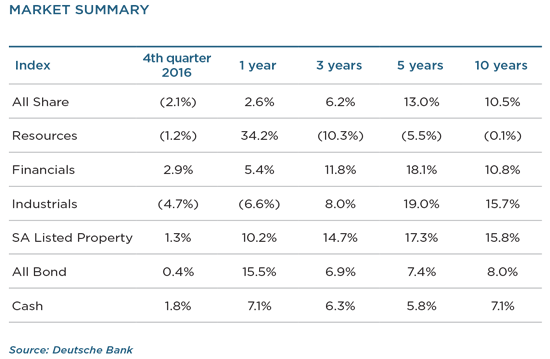

In US dollars, the MSCI All Country World Index returned 1.2% for the quarter and 7.9% for the calendar year, while the MSCI Emerging Markets Index returned -4.2% for the quarter and 11.2% for the calendar year. Locally, the FTSE/ JSE All Share Index (ALSI) returned -1.9% for the quarter and 15.9% for the calendar year in US dollars. Given the significant strengthening of the rand over the period, this translated into a rand return of 2.6% for the index for the calendar year.

The strong recovery in commodity prices in 2016 provided the tailwind for resource shares, which returned 34.2% in local currency terms for the calendar year, comfortably outperforming industrials and financials, which returned -6.6% and 5.4% respectively. Some of the notable moves in commodity prices (in US dollars) for the year include coking coal (+189%), thermal coal (+86%) and iron ore (+85%).

As expected, the US Federal Reserve raised interest rates by 25 basis points in December. Our base case remains that the pace of interest rate normalisation will be gradual and that interest rates will remain at historically low levels for longer. Despite the increased geopolitical uncertainty, the prospects for continued accommodative monetary policies, and the expected fiscal stimulus (lower taxes and increased state spending on infrastructure) in the US under the Trump presidency, this will most likely continue to be supportive of risk assets in the year ahead.

Locally, the political backdrop remains volatile; however, with the progress made since Nenegate, we have seen some improvement in investor sentiment since the end of 2015. Despite the weak base set in 2016, the SA economic growth outlook remains anaemic.

While the resource sector delivered a very strong performance in 2016, the longer-term underperformance relative to industrials and financials remains stark. Based on our assessment of fair value, resources are attractive enough to warrant a reasonable weighting in our equity and balanced portfolios. We have, however, trimmed some positions, given the reduced margin of safety.

Our preferred holdings remain Anglo American, Mondi, Exxaro and the platinum producers. We continue to favour platinum over gold producers and our preference remains the low-cost platinum producers Northam and Impala Platinum.

We believe the global businesses listed in SA are attractively valued and, as such, our portfolios have healthy weightings in stocks such as Naspers, Steinhoff International Holdings, British American Tobacco and Anheuser-Busch InBev. These businesses are exceptionally well managed and are diversified across numerous geographies and currencies, which make for robust business models and protect the companies from an earnings shock in any single market.

We continue to hold reasonable positions in food retailers and producers, as well as selected consumer-facing businesses (Woolworths and Foschini). These businesses are extremely well run and trade below our assessment of fair value.

Banks returned 11% for the quarter, outperforming the broader financial index. Valuations remain reasonable on both a price-to-earnings and price-to-book basis. These businesses are well capitalised, well provided for and trade on attractive dividend yields. Our preferred holdings are Standard Bank, Nedbank and FirstRand. Life insurers returned -2.2% for the quarter. We prefer Old Mutual and MMI Holdings, both of which trade on attractive dividend yields and below our assessment of their intrinsic value.

In terms of asset allocation, equities remain our preferred asset class for producing inflation-beating returns. We prefer global to domestic equities on the basis of valuation, and remain at the maximum 25% offshore limit in our global balanced funds. The rand strengthened by 11.5% against the US dollar during the year, which negatively impacted the rand returns of global assets.

The bond market returned 0.4% for the quarter, underperforming cash, which yielded 1.9%. We believe that yields on global government bonds are currently too low and do not offer value. We do, however, believe that the yields on local bonds are attractive, especially given a more favourable outlook for inflation in SA over the medium term. The risk premium implied when comparing the yields of local bonds to other developed and emerging market bonds suggests that the market has largely priced in most of SA’s political uncertainties.

Listed property returned 1.3% for the quarter. We expect domestic properties to show reasonable nominal growth in distributions over the medium term. Combined with a fair initial yield, this offers an attractive holding period return. We continue to hold higher-quality property names that we believe will produce better returns than bonds and cash over the long term.

As we start a new year, we are bombarded with predictions from numerous financial experts about what lies ahead in 2017. History has taught us that our ability to forecast the immediate future is limited.

We will remain focused on long-term valuations and will seek to take advantage of whatever attractive opportunities the market will present to generate long-term rewards for our investors. In an incredibly uncertain world, we continue to strive to build diversified portfolios that can absorb the many surprises that are likely to come our way in 2017.