South Africa - Personal

South Africa - Personal

Harley-Davidson - October 2016

Harley-Davidson (Harley) needs no introduction. It is arguably the world’s most iconic motorcycle brand and symbolises the very ideal of freedom for its riders. The company has been in existence for more than a century and during this time has grown to become one of the most dominant motorcycle manufacturers in the world, with a singular focus on the customer.

The investment case for Harley revolves around a few key pillars: its brand power, industry-leading financial metrics, future growth prospects and a strong shareholder focus.

BRAND POWER

When you purchase a Harley, you are not simply buying a mode of transport. Rather, you are buying into the Harley lifestyle, which includes branded clothing and accessories. Most importantly, it means joining the local riding chapter (which is analogous to a club). These chapters provide a sense of community and allow riders to socialise while building phenomenal brand loyalty. Harley has approximately 1 400 riding chapters worldwide and the Harley Owners Group (H.O.G.) has over one million members.

In 2015 Harley was the only motorcycle manufacturer to feature in Interbrand’s ranking of the world’s most valuable brands. Not only does this reflect the legacy that Harley has crafted over many decades, but it also showcases existing management’s stewardship of the brand. Customers come first, even if this hurts near-term financial results, as illustrated in the following example.

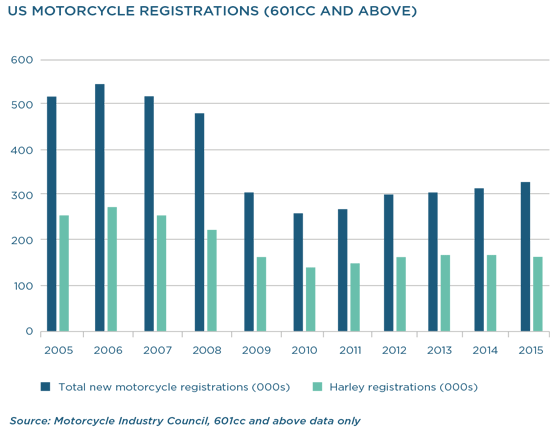

From late 2014 the Japanese motorcycle manufacturers (Honda, Suzuki, Yamaha and Kawasaki) heavily discounted their motorcycles in response to a weakening yen. This was an attempt to gain increased market share in the US. The discounting by the Japanese manufacturers encouraged other motorcycle manufacturers to do the same, and a vicious downward spiral of promotions ensued. Harley, however, remained an outlier, with a steadfast refusal to discount. To Harley, this would impair the value proposition of its new motorcycles and negatively affect the residual values of its existing bikes. As a result, Harley’s revenue declined and it lost market share in 2015. Most importantly, however, the integrity of the Harley brand remained intact, and it is not surprising to us that its market share has already started to recover. Customer loyalty, combined with Harley’s brand power, creates a very high barrier to entry and thus a significant moat around the company.

INDUSTRY-LEADING FINANCIAL METRICS

Harley’s margins are industry leading due to premium pricing on its premier product line-up and excellent operational efficiency. It has been said that a good crisis should never be wasted, and so Harley used the global financial crisis to completely restructure their manufacturing facilities and staffing levels. The company embraced ‘surge manufacturing’ − a leaner, more cost-effective and less labour-intensive process (labour intensity has been halved in some of its facilities). Surge manufacturing enables Harley to quickly adjust supply levels to meet market demand (and thus not risk oversupplying their dealer network). It also allows the business to cope with the traditional seasonality in motorcycle sales (purchases peak prior to the summer riding season). The adoption of this manufacturing approach has reduced time to market for new products by up to 30%.

Over the last five years the operating margin within Harley’s motorcycle segment has averaged 16%, significantly higher than that of its peer group. One of the benefits of a slow growth market is that Harley does not need to invest large amounts of capex in new facilities. This is one of the key reasons behind Harley’s exceptional free cash flow (FCF) generation, with FCF conversion over the last five years of 110%. This compares very favourably to the average business globally, which typically generates 70 cents to 80 cents of FCF for every one dollar of reported earnings.

FUTURE GROWTH PROSPECTS

Harley dominates the US heavyweight motorcycle market¹ with a market share of approximately 50%, more than double its nearest competitor. The US is a slow growing market and with motorcycle sales for 2015 40% below peak levels, it is clear that any pre-crisis froth has evaporated. We expect steady, but slow, growth from these levels.

Harley’s business remains domestically focused, with 64% of sales realised in the US. International expansion is, however, an underappreciated growth opportunity. In the last five years international sales have grown 1.4 times faster than those achieved in the US, and as Harley builds out distribution and expands into new territories, management aims for this to continue. By 2020, Harley envisages to add 150 to 200 new international dealerships − an increase of 20% to 30% on the current international base. In many countries, motorcycle riding is a key form of transport and leisure, and as the most iconic motorcycle brand in the world, Harley is well placed to capture an increasing share in these markets.

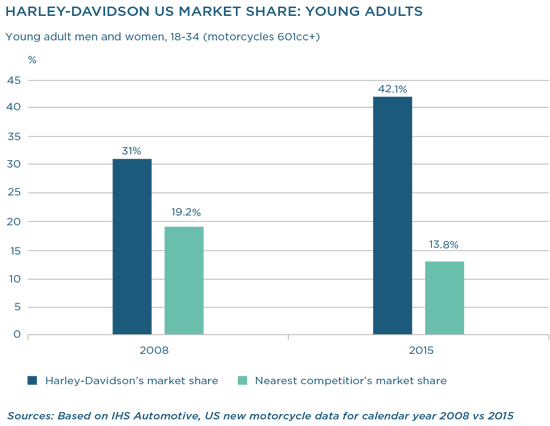

A key concern for Harley has been its ageing rider demographic, specifically the male baby boomer generation. This year the oldest baby boomers will turn 70, which means they are reaching a stage where riding a heavyweight motorcycle may no longer be feasible. Harley will need to supplement falling sales in this demographic with increased sales to a younger audience and other demographics. Management noted this issue some time ago and has since focused on broadening the appeal of motorcycling to other demographics where the company was underexposed. These strategies are beginning to show success, as indicated in the following graph which shows the gains in the key young adult demographic since 2008. In 2015, one-third of new Harley purchasers did not own a motorcycle before. In addition, 2015 was the eighth consecutive year in which Harley was the number one seller of motorcycles to young adults (aged 18 to 34). In a recent earnings call, Harley management stated that the company was now selling more motorcycles to young adults than they had sold to baby boomers at the same stage in their lives, setting Harley up for continued success in the future.

STRONG SHAREHOLDER FOCUS

For any investment, how management decides to allocate the cash generated by the business can have a meaningful impact on the company’s future prospects and returns to equity holders. In our view, management has acted astutely. Harley has a reasonable dividend yield of 3% (higher than the market), which has increased at a compound annual growth rate of 20% since the global financial crisis.

But it is the opportunistic share buybacks during the last 18 months that we view very favourably. The bulk occurred in 2015 when the business used its strong balance sheet² and the favourable financing environment to borrow $750 million at 4% for the purpose of buying back shares (at the time shares were trading at an approximate 9% FCF yield). This debt issuance, combined with cash generated by the business during the year, allowed Harley to repurchase $1.5 billion worth of shares (13% of the shares outstanding at the time) at prices well below our estimate of fair value. This management action is best described by Warren Buffett in his 1984 letter to shareholders: “By making repurchases when a company’s market value is well below its business value, management clearly demonstrates that it is given to actions that enhance the wealth of shareholders, rather than to actions that expand management’s domain but that do nothing for (or even harm) shareholders. Seeing this, shareholders and potential shareholders increase their estimates of future returns from the business. This upward revision, in turn, produces market prices more in line with intrinsic business value.”

CONCLUSION

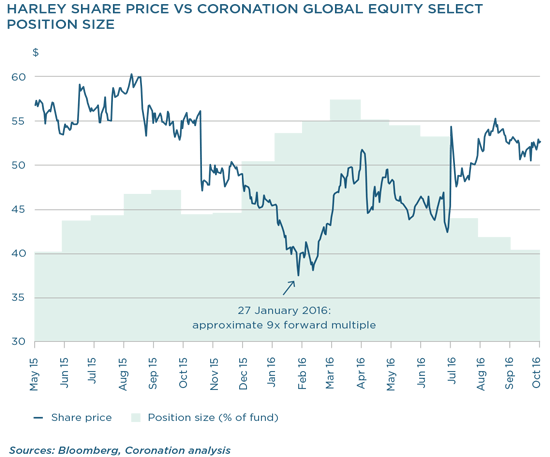

The market has recognised the value of Harley’s brand for many years. In fact, since 1990, Harley has typically traded at an approximate 15% premium to the forward earnings multiple of the Standard and Poor’s (S&P) 500 Index. There has only been one meaningful length of time in the past (2.5 years spanning the global financial crisis) when Harley traded at a discount to the market’s forward earnings multiple. But in mid-2015, when we first purchased Harley, this discount had widened to more than 20%. We naturally spent a significant amount of time researching the company’s fundamentals and determining our own view of what the business was worth. We concluded that there was significant upside to the share price at the time. This in-depth analysis gave us the conviction to add to the position as Harley continued to underperform (see graph below). At one point, Harley’s forward earnings multiple approached nine times − a 40% discount to that of the S&P 500 Index − while our view of what the business was worth remained largely unchanged.

Although the share price has since recovered (up a third from its lows), we continue to see upside and believe that Harley remains an attractive holding in our global funds.

¹ The heavyweight motorcycle segment (601cc and above) accounts for 85% of US motorcycle sales.

² Technical note: The face value of debt on Harley’s balance sheet exceeds the $750 million borrowed in 2015; however, this includes the financial services segment. The motorcycle company only has $750 million in debt, resulting in a net debt/EBITDA ratio of 0.7 times in 2015.