South Africa - Personal

South Africa - Personal

Economic views

No antidote for the uncertainty

“We demand rigidly defined areas of doubt and uncertainty!” – Douglas Adams, The Hitchhiker’s Guide to the Galaxy

- An increasingly complex and uneven economic landscape is emerging from the recovery.

- New variants, variable policy extension and withdrawal, rising inflation and a looming energy crisis challenge policy settings and market pricing.

- Wide-ranging political uncertainty has increased and may have long-term economic implications.

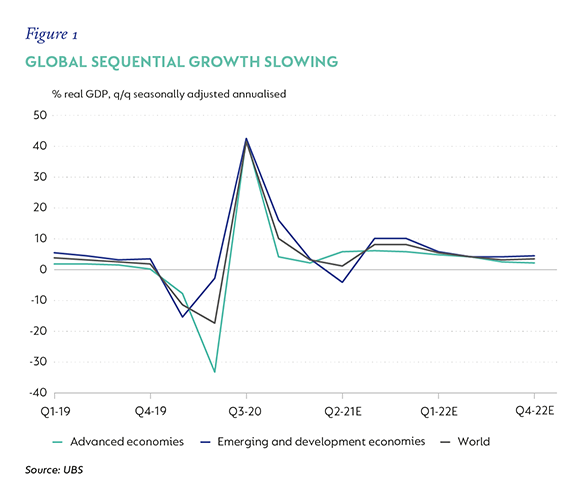

GLOBAL GROWTH HAS peaked (see Figure 1). This is not unexpected after the initial strong recovery from China late last year, followed by developed economies with superior vaccination strategies. After China, the US saw growth accelerate to 1.5% quarter on quarter (q/q) in the first quarter of 2021 (Q1-21) and 1.6% in the second quarter (Q2-21), then the UK staggered open and output surged 5.5% in Q2-21, after a lockdown-induced contraction in Q1-21. A laggard, Europe opened steadily from Q2-21, and growth momentum has gathered. Yet, into year-end, activity data has slowed, and the growth outlook has become uneven and increasingly complex. Different strategies related to Covid-19 variant emergence are in part to blame, but the uncertain withdrawal of policy support and related risks to inflation are now growing headwinds.

In the emerging markets, growth recoveries have been more mixed. These countries were slower to reopen because vaccine strategies were more challenging, and generally their policy support was more limited. Here too, though, recent data (excluding China) has seen sequential growth that was stronger than expected, implying upside risk to current expectations for 2021, and possibly 2022, but that overall momentum is also likely to slow.

THE SLOWDOWN WAS INEVITABLE

In contrast to the protracted and weak recovery that followed the Global Financial Crisis (GFC), by nature, the pandemic was a different kind of crisis.

Not only is the ‘V’-shaped recovery testament to the impact of the large, coordinated monetary and fiscal support, which protected economies from more enduring economic damage; what also helped was a much stronger starting position. Balance sheets were healthy, private sector leverage was much lower and the world had enjoyed a long period of growth. Importantly, financial systems are solid, much better provisioned and protected by policy interventions.

Despite this, the recovery has been accompanied by shortages, bottlenecks and a sharp rise in inflation. With the withdrawal of policy support moving closer, the question has shifted from what the recovery will look like, to how smooth the slowdown can be.

IMPACT OF INCREASED COMPLEXITY ON GROWTH PROSPECTS

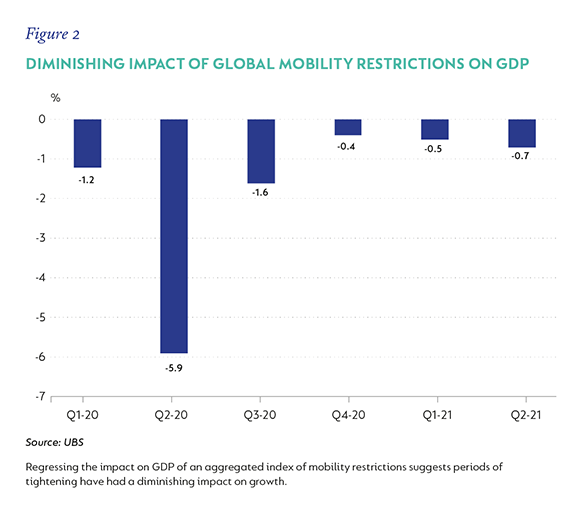

The first, of course, is that the scourge of the novel coronavirus is still with us. New variants may again derail the recovery, although the news here seems encouraging. The Delta variant now accounts for more than 90% of the new cases in most countries but, on aggregate, mobility restrictions continue to ease. There are, of course, still regional differences, notably in Asia where governments still have a zero-tolerance approach to new infections, but much of the West, and many emerging markets, have continued to open their economies. Regression analysis shows that the successive impact of lockdown since early 2020 on GDP has diminished as workplaces and productivity have adjusted (Figure 2). Death rates are also, mercifully, well below previous peaks. As vaccinations continue, the associated economic risk should continue to diminish.

In many countries, the critical fiscal support extended during the crisis is now rolling off. Some countries/regions – such as the US and Europe – have passed long-term stimulus plans, but the recovery risk of a ‘global’ fiscal cliff as emergency policies are taken away is a key uncertainty.

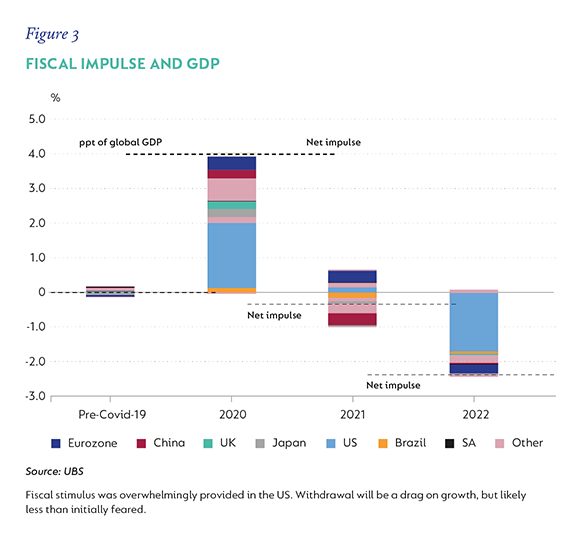

The IMF estimates that pandemic fiscal support amounted to about 5% of global GDP. Withdrawal will inevitably create a drag. But about 70% of this came from the US – which makes this predominantly a US story – and, at the time of writing, the possibility of a government shutdown in the US cannot be discounted and markets have become more jittery (Figure 3). It’s worth noting, though, that even in the US, the issue is a near-term one. Under current policy configuration, fiscal support will moderate from 7% of GDP in 2020 to 3% in 2023, with the bulk of the negative impulse happening now and into early 2022. As growth continues to recover, the drag should fade. While a clear and present risk, this should still be a meaningful underpin to the global recovery.

RISE IN INFLATION

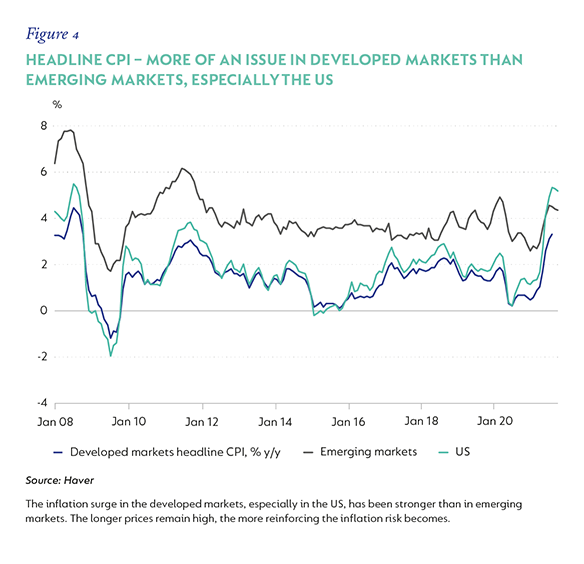

The rise in inflation that has accompanied the recovery is potentially a more enduring problem. Not only has the rise in prices been much stronger than expected, but it’s also been broader. A close look at US inflation data shows that the big surprises have come from ‘tail’ items affected either by lockdown or reopening, like cars, but increasingly, prices of non-core items such as housing and other domestic services are starting to rise. Bottlenecks have also lasted longer than expected, extending high goods prices. Some price drivers – namely shutdowns, bottlenecks, shortages and, more recently, the rise in house prices and the emerging energy crisis – may become reinforcing as they drive expectations and wage demands higher.

Central banks are still broadly of the view that the rise in inflation will be ‘transitory’, but the longer temporary pressures persist, the more enduring the effects may become – and this is becoming a clear concern. The likely policy response to higher inflation is also not straightforward. Central banks are wary of tightening too fast and choking growth, and both the Federal Reserve Board (the Fed) and the European Central Bank (ECB) have mandates that now emphasise growth considerations.

In countries where government debt is very high and debt costs are anchored to very low rates, fiscal and financial stability constraints hamper the implementation of rate hiking cycles. For now, the Fed has signaled it may be getting close to withdrawing some of the liquidity support it directed at financial markets during the crisis, but has been at pains to decouple this tapering from the prospect of higher policy rates. The Bank of England has started to signal that it is closer to raising rates than markets have previously anticipated, but the ECB has largely pushed the debate out.

The emerging energy crisis has both inflation and growth implications, notably for Europe and the UK. Oil prices are up significantly on a year ago. But natural gas prices have surged 354% year on year (y/y) in Europe and 284% in the UK year to date due to a strong demand for greener energy and tight supply, as both European and Russian gas production has been disrupted, resulting in low late-summer stock levels. Energy has a relatively large weight in European CPI (9.5%), with liquid fuels being the largest component and electricity somewhat smaller.

A similar pattern is visible in the UK, although the total weight is somewhat lower (6%). But there are also indirect price implications as energy works through supply chains and producer prices. Several governments have announced caps or tariffs to limit pass-through, but an initial limited direct impact on both Eurozone and UK inflation is likely, but will build as prices continue to rise. The impact of higher inflation – even unavoidable energy prices – on growth via lower consumption is historically quite small and, for now, seems likely to be cushioned by high levels of saving. Nonetheless, this may become a growing headwind should prices remain high for an extended period.

UNCERTAINTY ABOUT CONTINUED GOVERNMENT SUPPORT

The prospect of a withdrawal of developed economy monetary support has both liquidity and sentiment implications for emerging markets, especially those that are now considerably more indebted than before. The repricing of inflation risk in developed economies could see yields in riskier emerging markets adjust meaningfully upwards.

Many of these countries, such as South Africa, have struggled to return to pre-pandemic growth levels and their economies are not yet fully open. Most of these governments increased spending on health and social relief during the pandemic, and the withdrawal of this support now may have meaningful social consequences, while higher borrowing costs may become a challenge to fiscal sustainability.

Support for the banking and corporate sectors also helped guarantee liquidity through forbearance measures, coupled with accommodative policies. While the number of non-performing loans has risen, a massive surge in bankruptcies has, so far, been averted.

As supportive policies end and policy rates start to rise, the debt sustainability metrics for these companies may become much more challenging, especially if growth can’t catch up. Further, concerns about asset quality may emerge as companies face pressure on cash flows and debt service returns to normal.

RISKS ABOUND

In China, a series of announcements aligned to objectives related to ‘common prosperity’ and aimed at cracking down on corruption, corporate excesses and property speculation roiled markets in September, and may have long-term implications for both Chinese and emerging market growth. These events were accompanied by a step-up in military presence in Taiwan’s defence zone. It seems unlikely that the US will not respond, and tensions may continue to simmer. The threat of some tactical error is a persistent risk.

The EU is at loggerheads with the UK over Brexit and its new nuclear alliance with the US and Australia, all exacerbated by fuel shortages and rising prices. The Middle East may again challenge Western limitations on nuclear capacity, with Iran stalling talks to rejoin the Joint Comprehensive Plan of Action, the abandoned 2015 nuclear pact. The return of ISIS to Afghanistan complicates this situation, with the US reluctant to make further concessions in the region.

THE HARD PART MAY JUST BE BEGINNING, BUT THERE SHOULD BE SOME TIME

While we don’t want to downplay the potential risks associated with these complex and, in some cases, interconnected risks, it’s important to acknowledge some positive developments:

- Latest data suggests that the Delta variant’s infection rates have peaked in the US and elsewhere. With rising vaccination rates, the threats to economic reopening seem to be receding, for now.

- While the risk of a US government shutdown is down to the wire, we believe a crisis is in no one’s interest and that the Democrats are more likely to unite around revised infrastructure plans than hand the Republicans a victory.

- While political uncertainty in China is likely to persist, the economy should get a fillip from easier policy settings into year-end. Both these factors should support global growth and risk sentiment.

- The coming months will shed more light on inflation dynamics. Central banks have started to signal their preparedness to act should price growth not moderate, suggesting, for now, that runaway inflation will not be tolerated.

Across the globe, policymakers are facing the prospect of tough decisions in a very uncertain world, with little visibility. The risk of error is materially higher than it has previously been. That said, positive – albeit slower – growth momentum looks set to continue, with more accommodative policies in place for longer than we saw in the post-GFC period. In particular, the fiscal support deployed in the pandemic should normalise slowly, with some tolerance for larger deficits to ensure a stable recovery. In the US and Europe, the focus on using fiscal policy to promote longer-term growth is an additional stabiliser and may have the added support of both Germany and Japan, keeping more accommodative fiscal stances in play for longer.

In short, tough policy decisions will need to be made, but the message is still that policy priorities remain focused on supporting global growth. +

Disclaimer

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter