South Africa - Personal

South Africa - Personal

The Fund returned -12.0% during the third quarter of 2021 compared with the -8.1% return of the benchmark MSCI Emerging Markets (Net) Total Return Index. Taking the negative relative performance of the second quarter of this year into account, the Fund is 8.3% behind the benchmark year to date and by a similar amount over the last year. This has been a challenging short-term period, driven almost exclusively by China. The top five negative contributors over both the quarter and year to date were Chinese holdings. Over longer-term time periods, the Fund has comfortably outperformed the market, with 0.5% p.a. over 10 years and 1.6% p.a. since inception just over 13 years ago. The largest positive contributor was Russian food retailer Magnit, returning 16% in the quarter and contributing 82 basis points (bps) to performance. Aside from continued solid operational performance, best evidenced by 5% like-for-like sales growth in the latest reporting quarter, Magnit also announced the purchase of a smaller food retailer (Dixy) and an ecommerce cooperation agreement with Wildberries (the current leading ecommerce operator in Russia).

The latter will assist in improving Magnit’s ecommerce offering, which is essential in the larger cities in Russia and an area where the business has lagged its peers, in particular X5. The Dixy acquisition adds 10% to group selling space, and, besides the obvious cost synergies, also gives it lots of attractive sites in Moscow and St. Petersburg, the two most important metros where Magnit needs scale. This acquisition doubles its market share in both cities overnight, with Moscow market share increasing from 4% to over 8% and St. Petersburg market share from 9% to 17%.

Magnit is very attractive from a valuation standpoint, in our view, with the share trading on around 13 times forward earnings and offering a 9% dividend yield. Magnit now represents a 4.6% position in the Fund and is the third-largest holding. In terms of positive contributions, the Russian stocks generally featured prominently for the Fund, with both Yandex (fifth largest) and Sberbank (seventh largest) also being in the top 10 quarterly positive contributors, together adding 75bps of performance. The next biggest positive contributor to performance in the quarter was the zero direct weight in Tencent as it fell 21% during the period, contributing 64bps to relative performance.

This was, however, fully offset by the holdings in Prosus and Naspers, which combined are the largest effective exposure in the Fund. There was material corporate action in Prosus and Naspers that was completed during August, whereby Naspers shareholders were invited to tender part of their shares for Prosus shares. This was part of various ongoing measures to reduce the discount at which Naspers trades to Prosus and at which Prosus trades to the value of its Tencent stake. The Fund’s exposure to these three entities is now almost fully held via Prosus, as we accepted the offer from Prosus, receiving Prosus shares in return for Naspers shares.

Prosus itself had a busy quarter in terms of investments, having increased its stake in Delivery Hero (food delivery) by 2% to 27%, and acquiring BillDesk (payments) in India. The BillDesk acquisition adds to its existing PayU business and moves the combined entity into the top 10 payments providers in the world by transaction processing value (TPV), the standard metric by which these providers are compared. The ‘rump’ of Prosus, comprising all assets except its 29% stake in Tencent, is, in our view, worth almost a third of the current market capitalisation of Prosus. In contrast, Prosus trades at a discount to the value of its Tencent stake alone. This completely ignores all other assets in Prosus (a range of emerging market internet assets with a focus on food delivery, online classified ads, ecommerce, payments and online education, none of which is in China). Although there is still much that management must do to narrow this discount over time, we believe the recent moves to unlock value are a good step in the right direction, not least of which is a $5 billion share buyback scheme.

A few other notable positive contributors are worth mentioning. HDFC, the Indian mortgage loan provider and financial services holding company, returned 11% and contributed 50bps. The Fund also has a relatively smaller exposure to Alibaba (preferring to own more in JD.com), and with Alibaba falling 35%, this positioning helped to provide 45bps of positive performance.

The Fund was, on the whole, very negatively affected by the Chinese regulatory developments that unfolded during the quarter. (more details are in Suhail Suleman’s article here). The single biggest event was the action taken against the After School Tuition (AST) industry in late July. Although there is still some uncertainty over the final regulations and the companies themselves are still unable to clarify the impact to investors, the general principle is that there will be severe curbs on AST in K1 to 9 (pre-school, primary and middle school). This segment will be closed to foreign capital and become ‘not for profit’. There is some ambiguity regarding AST in high school (years 10 to 12 inclusive) and the industry may be able to continue to operate here, although the scale of the industry will shrink significantly regardless. The Fund started the quarter with a 2.3% position in New Oriental Education (EDU) and 0.9% in Youdao. During the month of July, final regulations came out with a very punitive outcome for the industry. We had sold a portion of the EDU holding before the final regulatory announcement but were still impacted by the material fall in the share price on the day of the regulatory announcements.

Despite the substantial decline in EDU’s share price, we decided to sell the remaining position to zero as the company’s long-term prospects had clearly been materially impaired. EDU cost the Fund 1.2% of performance during the quarter, while Youdao cost the Fund 0.3%. Youdao has been retained in the Fund (a 0.5% position) as its business model is very different, being exclusively online (as opposed to having a large physical learning centre presence, as is the case with EDU), and skewed more toward adult education and education hardware tools (almost 60% of the business), which is outside the purview of the regulations.

The second-largest detractor was Tencent Music Entertainment (TME), which cost the Fund 1.2%. While the bulk of TME’s revenue and profits today comes from social entertainment, it’s the music streaming part of the business (à la Spotify) that attracts us and makes up 80% of our valuation for TME. The large decline in TME’s share price during the quarter was primarily driven by regulatory moves in music streaming, as well as the significant selling of all Chinese internet stocks in general. In early August, the government announced that exclusivity on music would be banned in most circumstances. Our investment case was not primarily based on exclusivity remaining in place forever, as China was an outlier in this regard – the likes of Spotify, Apple Music and Amazon don’t have exclusivity in their various markets around the world. Factors other than exclusivity, such as the overall attractiveness of the ecosystem and user experience, the strength of curation and the range of music (and increasingly long audio, live concerts) play a significant role in success, and TME, with 75% market share in music streaming in China today, is the clear leader in this regard.

In addition to this, the music streaming industry is still in its early stages in China, in particular from a paying ratio point of view and from a pricing/average revenue per unit point of view (both still very low but increasing). While we believe that TME will lose some market share over time, in our view it will remain the clear leader in what is a growing market. Also, for independent artists (those without a record label), three years of exclusivity is still permitted, and there is a permitted 30-day exclusivity for new tracks from all non-independent artists, which act as a counter to the negative impact from an exclusivity point of view. Lastly, the market structure of music streaming in China is far more attractive than in other global markets due to the much smaller presence in China of the three dominant global labels (Universal Music Group, Warner Music and Sony Music). At the same time, the higher representation of (fragmented) local Chinese labels increases the bargaining power of the music streaming companies, leading to far higher long-term profitability.

Besides the very attractive long-term fundamentals of the company, the market value of TME’s listed investments (small stakes in Spotify, Universal Music Group and Warner Music) and net cash amount to approximately 45% of TME’s market capitalisation today. The music streaming segment is still marginally loss making, so earnings are depressed, but using our estimate of normal margins and applying them to estimated revenue would put TME on nine times free cash flow and closer to five times free cash flow if excluding the investments and net cash.

TME is a 1.4% position in the Fund. The next three largest detractors in the Fund (excluding Naspers/Prosus, EDU, and Youdao already discussed) were also all Chinese stocks, meaning that all of the seven largest detractors were Chinese stocks. Melco Resorts (gambling, Macau) cost 61bps, Baijiu spirits producer Wuliangye Yibin cost the Fund 41bps and China Literature 31bps. Having for some time been the most attractive investment destination in emerging markets in recent years, the Chinese market has now attracted commentary akin to being uninvestable.

We continue to talk to as many China experts/insiders/locals as we can on an ongoing basis, and our view at this stage is more nuanced: clearly the relationship between capital and the State has changed in a negative direction (and the risks and discount rate for China have increased) but, as a counter, the authorities have taken great pains to explain that these are targeted decisions with specific objectives and the country is still very much ‘open for business’. The extent to which this affects individual industries and names within these industries is where tough decisions need to be made. First movers in the tech industry that abused their dominant market position are likely to be the most negatively affected, while companies that were hurt by anticompetitive action will likely benefit going forward.

Regulatory clarity (as one has seen in music streaming and arguably in ecommerce as well) also assists one in getting to grips with what future earnings streams may look like, as opposed to ‘not knowing’ in other sectors where regulatory actions are still taking place. The most material changes in the Fund as a result of regulatory changes in China (AST aside) were therefore the sale of Meituan Dianping to zero and the reduction in the Alibaba position from around 4.5% to 2.0%. In the case of Meituan, aside from anticompetitive behaviour, the drive by the government to have better working conditions for so-called ‘Gig Economy’ workers will raise costs significantly, for both Meituan and its peers. Alibaba, while still cheap from a valuation perspective, in our view, is no longer attractive enough to be a top 10 position.

JD.com remains our preferred ecommerce operator and is the second-largest position (7%) in the Fund after Prosus/Naspers. Aside from a very attractive valuation – it trades on 11 times forward (below normal) earnings (and with over 100% free cash flow [FCF] conversion, the FCF multiple is lower than this) when listed subsidiaries, associates and net cash are stripped out – the company ticks all the regulatory boxes by investing in infrastructure, employing full-time workers, paying them well and providing all the benefits typically denied to workers in the ‘gig Economy’. In our view, JD.com will be the biggest beneficiary of the end of the ‘choose one of two’ rule (also unique to China) historically employed by Alibaba and ended by regulation, and we also believe its predominantly first-party (1P) business model will be the long-term winner in the eyes of the consumer.

There were a few new buys in the quarter, all under 1% positions. The first of these was the leading South Korean ecommerce retailer Coupang. In our view, Coupang is a very attractive business – we did a lot of work on it before the recent initial public offering (IPO), but the share traded well above our buying range, peaking at over $50 in the days after the IPO. Coupang has now steadily retraced down to below $30. Selling by pre-IPO shareholders (with the lock-up expiring mid-August) is very likely playing a role, as arguably are concerns over potential regulation in Korea given the China experience, and lastly, rising US long bond yields, impacting long-duration stocks in particular.

The ecommerce market in Korea, while already quite well penetrated (at 30% of retail sales) is still very fragmented. Coupang is number one, but with just a mid-teen market share. The company differentiates itself through its 1P model and best-in-class logistics, with 99% of items delivered within one day of ordering. It is also investing significantly in its marketplace offering to leverage its fulfilment infrastructure, and expanding its fresh grocery options. Other initiatives include fintech and food delivery (Coupang Eats), which is an effective duopoly with Delivery Hero (1.8% of Fund) in Korea. Coupang is currently a 1% position in the Fund.

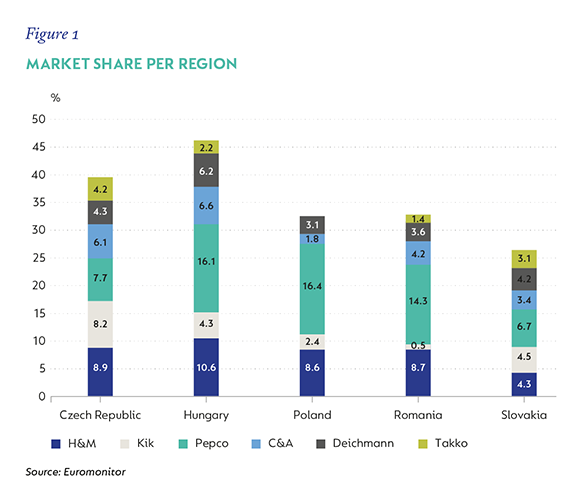

The second notable new buy was Eastern European retailer Pepco Group (PG). PG is a multi-format discount retailer with over 3 200 stores spread across the continent. The largest format is PEPCO, which sells clothing and general merchandise in Poland and other countries in Central and Eastern Europe and Italy. PG also owns Poundland in the UK and Dealz (the Poundland equivalent in Poland and Spain). Poundland’s product range is similar to the PEPCO format but also includes the fast-moving consumer goods category. Most of the group’s profits come from the PEPCO format, which makes up around two thirds of the total store base. The customer proposition is a wide variety of basic products at very low prices for cost conscious ‘mums on a budget’ looking to shop for the full family’s clothing and merchandise needs under one roof. The very low price points and small basket size make this segment more difficult for ecommerce to compete with. The data from price surveys suggests that in almost all categories, PEPCO prices are in line with or lower than the opening price point, and is between 30% and 45% cheaper than mainstream retailers like H&M and IKEA in their respective categories. PG has great financial metrics, with high returns on capital and full conversion of earnings into free cash flow.

We acknowledge that ecommerce is a potential longer-term threat to the business model and continue to evaluate developments here. In the meantime, the ongoing store rollout and market share gains should continue to enhance PG’s lead over competitors, as shown by market shares in Figure 1 – it’s the largest player in all countries in the region, bar the Czech Republic. PEPCO is currently a 0.9% position in the Fund.

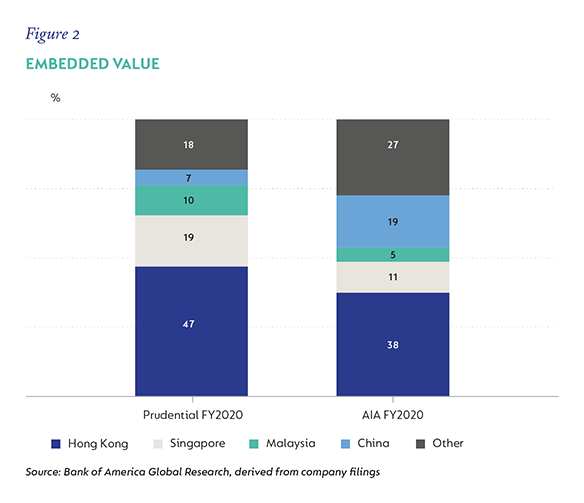

The final notable new buy was Prudential which has now sold/spun out its UK and US businesses, leaving it as a pure Asian/emerging market life insurer (much like AIA). Prudential has a slightly different geographical exposure to AIA, not least because its China exposure is much smaller due to being part of a joint venture, as opposed to AIA which owns 100% of its Chinese business. As a counter, a large part of the Hong Kong exposure for both insurers comes from sales to China mainlanders. The difference in embedded value makeup between the two insurers is shown in Figure 2.

Adjusting for differences in accounting practices and assumptions to compare the two insurers like for like, Prudential trades at a one-third discount to AIA, despite delivering higher renewal premium growth over the last 10 years. We think both insurers are attractive and 2% of the Fund is collectively invested in AIA (1.25% position) and Prudential (0.75% position). The new buy was fully funded by the sale of Ping An to zero. Besides a poor response to increased online competition, we have become concerned that Ping An’s exposure to the Chinese property market and its subsidiary Ping An Bank undermine the investment case and, given the risk of a high impact event on Ping An, felt the risk/reward equation was not in favour of retaining the position. There were a few other sales of smaller positions during the quarter.

We sold the small remaining positions in Stone (Brazilian payments provider) on valuation, Walmart de Mexico (retailer) due to more attractive risk-adjusted opportunities being available, Momo.com (Taiwanese ecommerce) on valuation (exceeded fair value) and lastly B3, the Brazilian stock and derivatives exchange on a change in the investment case in the form of new, potentially material, legal liabilities. We sold the remaining exposure as the share price converged to the new buyout price. +

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter