South Africa - Personal

South Africa - Personal

The Fund returned -21.6% in the first quarter of 2022 (Q1-22), -14.6% behind the benchmark MSCI Emerging Markets Total (Net) Return Index. This comes on top of a difficult period in 2021. Although such a large deviation from the benchmark over a short period is not totally inconsistent with our approach (the Fund has twice outperformed its benchmark by more than 16% in a calendar year), it is extremely disappointing, and we recognise that the recent performance is clearly well below client expectations. It is perhaps important to note that up until a year ago (March 2021), the Fund’s outperformance since inception was in excess of 2.4% p.a., and north of 1.5% p.a. over three, five and 10 years, so the significant underperformance has been largely concentrated in the last year.

By some way, the biggest driver of underperformance in Q1-22 was the Fund’s exposure to Russian assets. We started the year with just over 10% in Russian equities; our approximate internal maximum exposure limit (at cost) since we increased the risk premium applied to Russian assets in 2014 after the annexation of Crimea, which was also the primary driver of introducing this risk limit. The exposure comprised a mix of food retailers (over 40% of the Russian exposure), banks, the local Moscow exchange and the leading internet asset Yandex. At that point in time, Russian equities reflected valuations that were lower than levels at any point since the Global Financial Crisis. The upside to fair value of the Russian stocks in the Fund was over 100% and Magnit (second largest food retailer in Russia), for example, was trading at seven times earnings and paying a 14% dividend yield in the run-up to Russia’s invasion of Ukraine on 24 February.

During January and early February, while we did not reduce Russian exposure, we also didn’t add to the exposure, and rather went the route of changing the mix of the Russian exposure to reduce its risk profile. At the same time, we increased the Fund’s overall commodity stock exposure as a hedge against potential conflict in Ukraine, due to Russia being a large source of supply for several commodities globally. The largest change in the Russian exposure during this period was to reduce the Sberbank position (the only State-owned Russian stock held in the Fund and likely to be far more affected by potential sanctions in our view) in favour of a new position in Lukoil (an oil price hedge in the event of conflict). We also switched Sberbank to other existing positions, in particular Magnit. As a food retailer supplying essential goods in a fragmented market, we believed Magnit would likely be less affected by the broader economy and sanctions and would continue to take market share from weaker operators in a tough economic environment. This was very much the case in 2014-2015. As a result of this switching, Sberbank went from being a 3% position late last year to being a 0.85% position the day before the invasion.

Our seemingly high overall Russian exposure (8.8% of Fund the day before the invasion of Ukraine) reflected a combination of the extremely attractive valuations (over 100% upside to fair value) and a base case view that a full and violent invasion of Ukraine (as opposed to just going after the eastern Donbass region for example), while being a possibility, was low probability. With the benefit of hindsight, we were clearly wrong. In addition to this, the apparent poor performance of the Russian military (who annexed Crimea within days in 2014), combined with the courageous fightback by Ukraine’s army was not anticipated. It seems clear now that Russia’s president Vladimir Putin believed he would take Kyiv and the whole of Ukraine within a few days, a view that was shared by most geopolitical and military experts. It was, in turn, these unexpected developments (a conflict going on well beyond a few days) that created the time and opportunity for the West to cooperate with each other and put together an unprecedented sanctions package, including the sanctioning of a large part of the Russian Central Bank’s reserves. At the same time, Switzerland abandoned an almost timeless neutrality policy and Germany changed decades old policies with regards to military spend and supply of lethal weapons. In other words, it wasn’t just the full invasion of Ukraine in isolation: it was the four factors taken together (a full and brutal invasion of the whole of Ukraine, the poor military performance of Russia, the courageous fight back by Ukraine, and the resultant unprecedented sanctions package put together by Western countries in cooperation despite different vested interests) that made this an extreme event. Nonetheless, the fact is that the impact on performance has been significant, and, while this terrible event is by no means over (making it difficult to reach firm conclusions), we are carefully thinking through whether there were any flaws in our process (with a focus on the process as opposed to the outcome) in the months leading up to the invasion, and what lessons are to be learnt here.

The impact on the Fund has been a write-down to zero of all the Russian assets, costing the Fund 8.4% of relative performance in the quarter. Magnit had the biggest impact, costing 3.7%, followed by Yandex (-2.1%) and Moscow Exchange and Sberbank (-1.1% each). Other Russian holdings cost a combined -2.1%. The only material positive contributor was the zero weight in Gazprom, which provided +0.6% of relative performance. The write-down is not necessarily reflective of economic reality but is at least partly due to technical factors. On the day of the invasion and the day or two that followed before trading was halted, Russian companies with GDR listings in London were subjected to significant selling pressure in what appeared to be a ‘get out irrespective of price’ approach. The result of this is that most Russian London listings traded all the way down to less than 1 cent, with Magnit (the entire company) for example being valued at $6 million in London. Magnit, in our estimates, should generate around $500 million in free cash flow this year, which, using a market cap of $6 million, puts it on a 8,333% free cash flow yield. In Moscow, Magnit has now started trading again, and while the market price may be artificial (foreigners cannot yet participate in the market), there are willing local buyers and sellers in what is reasonable volume. The Moscow listing of Magnit is now almost back to its pre-invasion share price level and is being valued at $5 billion and a resultant 10% free cash flow yield.

All of the Fund’s Russian holdings have a Moscow listing and using Moscow’s current share prices and the current USD/RUB exchange rate of 85 (which is clearly inflated, in our view, due to capital controls and other factors) the Fund’s 8.8% pre-invasion Russian exposure is currently worth about 8% of the Fund. Adjusting for what is, in our view, a more sensible USD/RUB exchange rate, this equivalent percentage is 6% of Fund. It is too early to conclude whether the London pricing of Russian equities is correct (in effect that all Russian stocks are worth zero) or whether the Moscow pricing is correct - the answer may lie somewhere between the two: one just doesn’t know at this point. Given that we have written off all Russian holdings, there is now only upside optionality sitting in the Fund. In early March, we placed an indefinite firm-wide moratorium on the purchase of any new Russian equities, and this is now likely to remain in place unless there is regime change in Russia. At the same time, when Russian markets become accessible to foreigners again, we will manage existing Russian exposure in the best interests of clients, as opposed to a “sell at any price” approach.

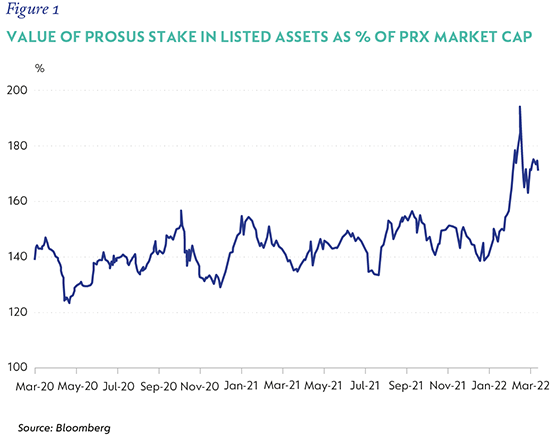

Other than Russia, it was predominantly Chinese names that hurt performance in the quarter as China continues to pursue a ‘zero-Covid’ strategy, with continuous lockdowns, most notably in Shanghai, the country’s economic capital. JD.com, Wuliangye Yibin, Tencent Music and China Literature were all small detractors as a result. Most frustratingly, Naspers/Prosus (combined 7.2% of Fund) cost 2.2% of relative performance as the discount at which they trade to the value of just their Tencent stake (valuing all other assets at zero) widened to record levels. The current market cap of Prosus is now around €95 billion – well below the €122 billion value of its Tencent stake alone. The substantial other investments excluding Tencent are worth around €60 billion in our view, with around €50 billion of this outside of China. Naspers trades at a substantial further discount to Prosus, providing even greater upside.

There were some notable positive contributors for the quarter too, the largest being Brazilian cash-and-carry retailer Sendas, which returned 45% for a 1.1% positive contribution to relative performance. The two largest commodity holdings, AngloGold and Anglo American, contributed a combined 1.5%, while Petrobras’s 34% return for the quarter contributed 0.6%. Other significant contributors amongst the Fund holdings were Brazilian education provider YDUQS, Korean convenience retailer BGF and Brazilian brokerage XP. These contributed around 0.2% each.

China internet, in total, makes up around 20% of the Fund, albeit in large part concentrated in two positions for specific reasons, with Prosus/Naspers (providing significant exposure to Tencent but at a material discount) and JD.com making up around 70% of the Chinese internet exposure. In both cases we believe the upside to fair value is in the order of 150%. After over a year of relentless new internet regulations (and resultant declining share prices) there have been a few recent developments on gaming approvals (these have resumed after an 11-month hiatus) that provide some light at the end of the tunnel.

The most notable of these was the recent (11 April) resumption of approvals of online games. There have been no new approvals of any online games since July 2021, some eight months ago. This pause was similar in duration to the 2018 regulatory-driven freeze on new game approvals in China but is also different from the point of view that it came at the same time as numerous other regulatory interventions throughout the tech sector. Gaming is a significant part of Tencent’s business, as well as being the dominant part of NetEase’s business (another Fund holding). In addition to this, concessions to US authorities with regards to on-site inspection of accounting records in China (a stumbling block with regards to the issue of ADR listings) have recently been announced by the Chinese securities regulator. Interestingly, both these recent announcements come just weeks after China’s economic czar, Liu He, came out with a strong statement on supporting capital markets, specifically including overseas listings of Chinese companies, and committing to regulatory clarity as well as an acceleration of outstanding regulations.

There were several new buys in the quarter, the largest of which was Glencore Plc (1.5%), the global diversified miner and trading house. Given the fact that Glencore has had a listing in South Africa for several years, it is a company that we have covered in detail for some time, and it has been a sizeable holding in our South African (SA) portfolios for the past few years. Additionally, commodity stocks make up 25% of the SA equity market so this is an area where the SA team spends a lot of time, which we believe is a competitive advantage in our process. Historical underinvestment in new mines around the world means that supply of many commodities is constrained, while demand continues to be sustained, leading to higher prices. The situation in Ukraine has exacerbated the supply factor. Glencore benefits from this by being a supplier low down on the cost curve for many commodities. All these factors have combined to result in significant free cash flow (FCF) generation, with Glencore converting around 120% of its earnings into FCF over the next five years on our forecasts. In previous boom times, the larger commodity houses often went on buying sprees, but today Glencore is returning most of its free cash to shareholders in the form of dividends as there is little debt to repay. From an ESG perspective, we have had meaningful interaction with the company over time and Glencore has made significant strides in this regard. Almost all of the old management team have now been replaced or have left, the compliance function has gone from being a team of five to a team of 150 today, and the company has committed to running down their coal assets over time.

In addition to this, commodity companies are now being appreciated more for the role they are playing in helping the world transition off fossil fuels. Those that produce copper, nickel and cobalt also stand to benefit from this meaningful boost to demand growth. In Glencore’s case, these three commodities make up half of our fair value. Glencore trades on less than six times this year’s earnings and almost a 10% dividend yield, albeit with elevated commodity prices in selected cases. Even with more normalised commodity prices, Glencore is attractively valued.

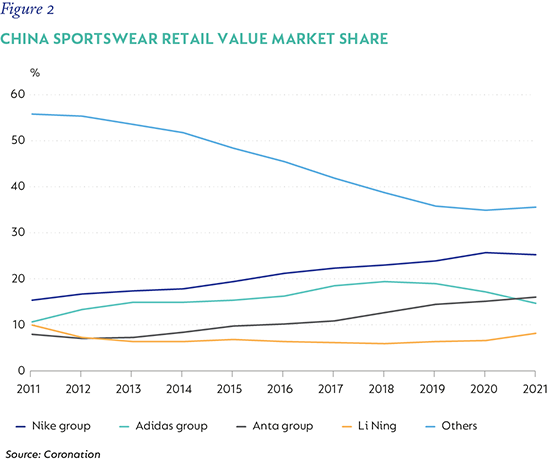

The next two most significant buys were previous holdings in the Fund that we had sold out of before. The first of these is Li Ning (1.3%), a Chinese sportswear company that we initially bought a few years ago but sold after material share price appreciation. Over the past several months, Li Ning’s share price has declined from a peak of almost HK$ 110 to as low as HK$ 50 and this provided a buying opportunity, in our view. Together with Anta, the Fund now has 2.5% in these Chinese competitors to the likes of Adidas and Nike. The strong tailwinds of rising income and a focus on health via exercise/sport (in turn strongly encouraged by the Chinese government) are positives for all the sportswear companies in China, but Anta and Li Ning have the added advantage of being the two most well-known local brands and are taking share in a fast-growing market. The steady earnings growth compounding for years ahead should provide attractive returns for shareholders, and we believe the starting valuations are very reasonable, particularly given the scarcity of such high-quality assets in China.

The other new buy that was a previous holding is Momo.com, Taiwan’s largest e-commerce retailer. We had sold out of Momo.com in the middle of last year when it reached our fair value, and it subsequently went up even further in the frenzy for internet assets last year. In recent months, the sell-off in growth assets has seen Momo.com halve to under NT$1,000 and we used the opportunity to purchase it again. The investment case has remained largely unchanged, with strong top-line growth for several years and below normal margins for what is the clear leader in an underpenetrated e-commerce market in Taiwan. Other small buys (around 0.5% positions each) for the quarter were ICICI Bank and Oil & Natural Gas Corporation in India, semiconductor wafer fabrication equipment supplier LAM Research (with 80% of sales to emerging markets) and pan-LatAm payment processor dLocal. The combined exposure to these four names was 2% at quarter end.

To fund the purchases a few sales were made. The largest of these was Midea (Chinese white goods). Although this is a very good business in our view and is still attractively valued, it is the only Chinese stock owned that has material export revenues and the risk of China being caught up in sanctions against Russia has undoubtedly increased. As such, this sale was more of a risk reduction decision more than anything else. We also sold the remaining small positions in Yum China, Aspen and Infosys, the latter having become more than fully valued in our view. Finally, we funded the Momo.com purchase through the sale of the Taiwanese convenience retailer President Chain Store. This was to keep overall Taiwan exposure largely unchanged at slightly less than 7% of Fund. We don’t know whether China will one day try to take Taiwan by force, but this is an ever-present risk given how vocal China has been about potential Taiwanese independence and the risk of armed conflict has slightly increased, in our view.

The weighted average upside to fair value in the Fund is now over 90%, which is close to an all-time high. Furthermore, this 90% upside does not include any contribution from Russia, which only has upside optionality as it has been written down to zero already. The five-year IRR (internal rate of return) is a very compelling 21% p.a.

Please note that this is for the retail version of the fund. View the Global Emerging Markets Fund page

Disclaimer

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter