South Africa - Personal

South Africa - Personal

Optimum Growth declined 0.7% in rands in the fourth quarter of 2020 (Q4-20), compared with a 3.4% benchmark return. As the Fund is rand denominated and most of the underlying exposure is in foreign currency, the strengthening of the rand (14% stronger) this quarter was the primary contributor towards the negative absolute return in rands. After strong alpha generation in the first nine months of the year, it is disappointing to underperform this quarter, but it is still pleasing to note that the Fund delivered a rand return for the year of 21.6%, resulting in 6.8% alpha. It can be expected that, in the short term, the Fund may underperform the benchmark, but we remain focused and excited that it is well positioned to achieve long-term outperformance. Over the last five years, Optimum Growth has generated a positive return of 10.8% p.a.; over 10 years, a return of 16.9% p.a.; and since inception over 20 years ago, 14.5% p.a. (3.1% annualised outperformance).

The Coronation Global Emerging Markets (GEM) Fund returned 20.0% in US dollars during Q4-20, 0.3% ahead of the 19.7% return of the benchmark. For the year, the Fund returned 23.1%, outperforming the market by 4.8%. It is pleasing for us that the Fund has followed up its best-ever year of relative returns (outperformance of the market was 19.8% in 2019) with another year of strong outperformance. Over more meaningful long-term periods, the Fund has also outperformed materially – by 1.7% p.a. over five years, 1.9% p.a. over 10 years and by 2.5% p.a. since inception just over 12 years ago.

MARKET RETURNS ROBUST DESPITE VOLATILITY

Given how tumultuous 2020 was, it seems scarcely conceivable that the market return was so positive for the year. The scale of disruption to human life was unprecedented in modern times outside of periods of war. Despite the emergence of more highly transmissible variants of Covid-19, we enter 2021 with hope on the horizon for a return to something akin to normal by year-end – if the world is able to roll out vaccines and cover the bulk of the vulnerable population (the elderly and those with conditions that increase their risk of severe outcomes if infected).

PERFORMANCE IMPACTS

In Optimum Growth, the largest positive contributors in the quarter were Disney (+28%, 0.5% positive impact), Mercado Libre (+38%, 0.5% positive impact) and the Housing Development Finance Corporation (HDFC) (+30%, 0.5% positive impact). The Fund incurred unrealised losses on a collection of put options and short-index positions, which provided valuable protection historically, but detracted from performance this quarter due to a buoyant market. Collectively, these put options and short-index positions had a 1.6% negative impact during the quarter, but having them in place continues to provide the Fund with protection should there be a market selloff. Outside of this, the other notable negative detractors were our foreign currency cash holding (-10%, 1.0% negative impact) Alibaba (-28%, 0.8% negative impact) and our physical gold position (-12%, 0.5% negative impact).

Optimum Growth ended the quarter with 73.1% net equity exposure, slightly higher than at the end of September. Our negative view on global bonds remained unchanged, as a large portion of developed market sovereign bonds offer negative yields to maturity, with the follow-on effect that most corporate bonds also offer yields that do not compensate for the risk taken. Only 1.2% of the Fund is invested in bonds, which is largely made up of a 0.5% position in L Brands (owner of Victoria’s Secret) corporate bonds.

The Fund also has c.2.2% invested in global property, largely Vonovia (German residential). Lastly, it has a physical gold position of 4%, a 0.9% holding in AngloGold Ashanti and a 0.8% holding in Barrick Gold Corporation, the world’s largest gold miner. The physical gold position was added to during the quarter for its diversifying properties, while the AngloGold Ashanti position was a new buy, acting as a more leveraged exposure to gold, after falling c.35% from its high in July versus a roughly flat gold price move. The balance of the Fund is invested in cash, largely offshore. As has been the case for many years, the bulk of the Fund (over 90%) is invested offshore, with very little exposure to South Africa.

BUYING ACTIVITY

Notable buys/increases in position sizes during the quarter were Deutsche Boerse, Netflix and Tencent Music Entertainment.

Deutsche Boerse

Deutsche Boerse is the fifth-largest (by market capitalisation) exchange operator in the world. The business has many attractive attributes, such as exposure to dominant liquidity pools that utilise its proprietary hard-to-replicate products, and a large and growing exposure to recurring revenue streams (48% of group revenue currently). This is further supported by many of its business segments being exposed to secular growth drivers, such as the continued rise of passive investing. This is also a business that enjoys high incremental margins as it grows due to limited incremental costs being associated to this growth. The business currently trades on just over 20 times earnings (which are 100% converted into free cash flow [FCF]), with our expectation that it should be able to grow earnings at high single digits. This, combined with a 2.5% dividend yield, should provide a double-digit hard currency return.

Netflix

Netflix is a business most consumers will be familiar with, as it operates the largest (from a subscriber perspective) video streaming service globally. It is led by a visionary management team, which has disrupted the legacy TV entertainment space. Netflix currently has just under 200 million subscribers globally, which should continue to grow by more than 20 million p.a. over the next few years, as household penetration is still low outside the US. This subscriber growth is further supported by large content investments (dwarfing everyone except Disney) that should enable the continuation of the ‘flywheel’ of more content driving more subscribers.

Netflix should also exhibit very strong pricing power over the longer term from what we deem to be a low base, and there is some early evidence of this in price increases in the US that have had limited impact on churn levels. Longer term, the economics of the business should improve drastically as the large content investments begin to leverage across its ever-growing subscriber base, resulting in a significant expansion in margins along with a dramatic improvement in FCF generation, which has turned positive this year after many years of cash consumption. Based on our assessment of the normalised earnings power of this business, we feel it is an attractive investment.

Tencent Music Entertainment

Tencent Music Entertainment is the largest music streaming business in China, with more than 600 million users. The business also has a successful live streaming service with a music focus, along with the dominant online karaoke platform. This positions Tencent Music Entertainment as the key player in the music space in China, with significant long-term monetisation opportunities as the company expands its ecosystem and increases monetisation touchpoints. This is further supported by a current low paying ratio (c.8%) for its music streaming business, along with very low average revenue per user (just over $1), which should expand significantly over time as consumers derive value from its products.

The business has been investing aggressively into various products to improve and expand its offerings, and these investments should begin to be harvested this year. Current profitability (and FCF) is significantly depressed; in our view, and, using our estimates of 2022 FCF, the business trades on a 5% FCF yield, which we deem attractive considering the long duration growth the business should experience, coupled with its dominance in its respective markets.

AN AGILE POSITION

The markets remain volatile as the Covid-19 pandemic continues to cause disruption around the world, with various governments responding in different ways, which continues to create a disruptive operating environment for many businesses. However, with vaccines now being formally rolled out, there is light at the end of the tunnel. Exactly when enough people have been vaccinated, which should end the Covid-19 pandemic, is still uncertain, as there remain unknowns relating to various governments’ ability to first procure the vaccine, and then inoculate their populations.

As a result, the outlook for the future remains uncertain and hard to predict, but we take comfort in the fact that Optimum Growth holds a collection of businesses that we feel are attractively priced and can operate in what we deem to be a highly complex and fast-changing environment. Moreover, the fact that the Fund is a multi-asset flexible fund provides us with additional tools to protect (through the use of put options, for example) and grow capital.

We are now approaching the one-year anniversary of Covid-19, with reason to be somewhat optimistic that its devasting effects are closer to coming to an end compared with a few months ago. How consumer behaviour permanently changes, and what the world will look like in the next few years, remain unknowns. However, against this backdrop, we remain positive on the outlook for Optimum Growth, which has been built bottom up, with a collection of attractively priced assets that provide diversification to achieve the best risk-adjusted returns going forward.

GEM CONTRIBUTORS

In the quarter under review, the biggest contributor to outperformance in the GEM Fund was the HDFC, which returned 48%, contributing 83 basis points (bps) to alpha. Earlier in 2020, the HDFC had declined by 40% from pre-pandemic levels as India shut its economy down completely in one of the harshest lockdowns seen anywhere in the world. While most financial services companies could operate digitally during the lockdown, mortgages have a legal requirement to be signed in person on a physical piece of paper. With the HDFC being unable to open its offices during Q2-20, loan origination plummeted. The large decline in the share price didn’t make sense to us. Aside from being clearly driven by temporary factors, the mortgage business makes up less than half of the HDFC’s valuation, with the balance of its value being its stake in the country’s largest private sector bank (HDFC Bank), a life assurer and an asset manager (all listed). None of these were as badly impacted by the lockdown, implying that the market was writing down the mortgage business to a fraction of its former value. As the year wore on, volumes returned to normal and now, despite many localised restrictions, loan volumes are back to 90% of pre-pandemic levels. The worst fears of large-scale defaults and people taking advantage of moratoria mandated by the Reserve Bank of India have also proven to be overblown and, as a result, the HDFC’s share price has recovered strongly.

The next-largest contributor to performance was pan-Latin American ecommerce retailer Mercado Libre, up 54% for a 61bps contribution. We wrote extensively about Mercado Libre in our Q2-20 commentary, and how the reasons for the strong share price performance can be put down to operational results far in excess of our (already very positive) expectations. In the Q3-20 results released in November, Mercado Libre saw gross merchandise volume and items sold on its marketplace more than double year on year. Its payments business, Mercado Pago, also saw growth in excess of 100% - both on its network (people using the payments system to buy things on the business’s websites) and off its network (people using Mercado Pago at other retailers).

Other material positive contributors were Tencent (up ‘only’ 10%, so the zero weighting in the Fund contributed 56bps of alpha), Wuliangye Yibin (up 37% for 49bps alpha) and HDFC Bank, which makes up roughly 40% of the HDFC’s sum of the parts valuation (up 45% for a 45bps contribution).

GEM DETRACTORS

On the negative side, the largest three detractors were all due to underweights or zero weights. Although Samsung is now a 3.5% position in the Fund, we are underweight the benchmark, and Samsung’s 50% return in the quarter cost 47bps of alpha. We neither own Pinduoduo (a group buying-themed e-commerce retailer in China) nor NIO (best described as China’s Tesla), and both of these stocks more than doubled in Q4-20, costing the Fund 42bps and 40bps of alpha, respectively. Three other detractors of around 35bps each were Naspers, X5 and NetEase, all of which had positive returns in the quarter but lagged the 19.7% return of the index and therefore detracted from relative performance somewhat.

OTHER ACTIVITY

The biggest moves in position size for the quarter in existing holdings were in the two e-commerce players Alibaba (70bps decline in position size) and JD.com (93bps increase in position size). In the case of the former, the decline in the share price of 20% during Q4-20 was the primary driver of the reduced exposure. Alibaba suffered the fallout of the failed initial public offering of its financial services affiliate, Ant Financial, as well as increased regulatory scrutiny of its operational practices by the antitrust authorities. We added slightly to the position, since Ant Financial makes up less than one fifth of our look-through valuation, but this buying was not enough to offset the impact of the share price decline. In the case of JD.com, continued great operational results, coupled with the share lagging the market, resulted in us buying more to increase the position further.

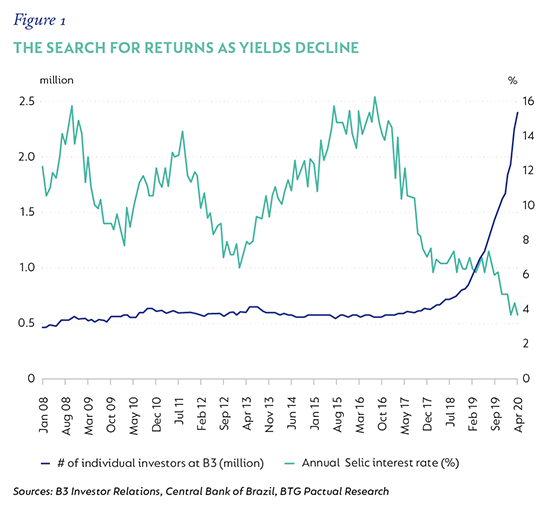

There were four new buys in the quarter, only one of which has been previously held in the Fund. Not coincidentally, this buy, the Brazilian stock and commodity exchange Brasil Bolsa Balcão (B3), was the largest of the buys and reached a 73bps position by year-end. We have covered B3 since 2008 (when it was known as Bovespa) and have owned it before. Over time, the company has evolved through mergers with complementary businesses that have established a ‘moat’ around its overall offering, which is now exceptionally difficult to overcome. In its current form, B3 comprises an exchange for the trading of equities, as well as fixed income, currency contracts, over-the-counter derivatives and a lien system that assists with credit provision and the registration of loans. Brazil historically ran very high nominal and real interest rates, a legacy of the country’s long fight against inflation, which culminated in the ‘real plan’ of 1994 that ended hyperinflation. The very high real interest rates made fixed income the investment of choice for domestic investors, to the extent that equity investment was not particularly attractive (why take equity risk when you can earn 5%-8% real returns at very low risk?). As Brazil’s economy has stagnated, and as central banks around the world slashed rates to boost economies in response to Covid-19, interest rates have declined to record lows in Brazil and investors have been drawn to equities in search of returns, as illustrated by Figure 1.

RISK ASSET APPEAL

We do not believe this is a once-off move, but rather a structural trend in the country as its financial system evolves toward what is found in other parts of the world. Equities comprise less than 10% of individuals’ investment portfolios in Brazil, which is only half the level of neighbouring Colombia, a country with a far less developed financial system.

In the US, for example, the figure is in the mid-30s. Brazilian mutual funds have, in aggregate, only 10% exposure to equities and, for pension funds, barely 20%. Volatility, of which there is plenty right now, benefits the derivatives business and lower interest rates benefit loan provision, which uses B3’s infrastructure services. All these suggest many years of strong revenue growth and, with a large portion of B3’s costs being fixed in nature, profits are likely to grow far in excess of turnover. In the results published after the end of Q3-20, for example, operating profits grew by 79% for the first nine months of 2020 on the back of a 41% increase in revenue over the same period. Our assessment of fair value for B3 has increased materially as the business and market have evolved and this, coupled with a 20% fall in the share price after a July peak, prompted us to start buying in November.

The next largest new buy was Youdao (54bps position at year-end). Youdao is majority owned by NetEase (3.0% of the Fund) and offers a variety of online education services catering to both adults (foreign languages, professional certification), and primary and secondary school students (K12). Its key selling point is personalised learning, with courses adapting to the progress, and strengths and weaknesses of students. The business has also launched some innovative hardware solutions such as a dictionary pen that simultaneously translates text as the user scans over it. Youdao aims to offer many of the benefits of offline/in-class tutoring online by combining good teachers with its technology.

Already there are over 100 million monthly active users of Youdao’s various services and it is spending heavily to convert these into students of its online courses. The association with NetEase provides a structural advantage in customer acquisition and the company’s hardware sales should convert into more students over time, in our view. Profits are therefore depressed in the short term, but as spending declines and revenue grows strongly, Youdao is likely to be very profitable and highly cash generative, in our view.

The Fund also purchased a 50bps position in Walmart de México y Centroamérica (Walmex), a majority owned but separately listed subsidiary of the Walmart Group that operates across Mexico and Central America. We started researching and following Walmex in detail back in 2010 and have met the company many times over the years, and have always been impressed by the business. However, this is the first time it has been bought into the Fund, as valuation has never been on our side. Its various formats, ranging from bodegas to Sam’s Club (a members-only bulk-buying club), plus its status as an e-commerce operator in Mexico to rival Amazon and Mercado Libre, make it a very attractive business with a presence in all aspects of retail in the region. Walmex’s share price has barely moved in dollars over the last 10 years, even though its intrinsic value has consistently increased, and this combination brought it into buying range for us for the first time.

Our last new buy (40bps) was Taiwanese e-commerce operator Momo.com, which focuses on the business-to-consumer sector. Despite having many of the same drivers of e-commerce that South Korea has (high per-capita income, densely populated urban areas, and high internet and smartphone penetration), e-commerce penetration in Taiwan is only 12% versus 31% in South Korea. Mainland China has 32% e-commerce penetration, partly driven by the very poor infrastructure for physical retail. We believe Momo.com will benefit disproportionately from rising e-commerce penetration, thanks to its heavy investment in warehousing and logistics – Momo.com has outspent its main competitor PCHome by almost three times on a like-for-like basis, and now has an automated distribution centre near the capital Taipei and 13 satellite warehouses across the island. On delivery, although e-commerce operators in Taiwan outsource to third parties, Momo.com is investing in its own dedicated delivery infrastructure to gradually increase this over time from the 10% of orders being fulfilled directly right now to 20%-30% within the next few years. It also aims to get delivery times down to three hours for the capital, which will be far superior to any competitor offering.

Finally, we sold our last remaining exposures in Chinese spirits firm Jiangsu Yanghe (43bps position) and Indonesian broadcaster Media Nusantara (17bps position) to make way for the buys above and, in the case of Jiangsu Yanghe, a very strong run in the share price to in excess of fair value.

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter