South Africa - Personal

South Africa - Personal

Investment views

Finding opportunity amid turmoil

‘In the midst of every crisis, lies great opportunity.’ - Albert Einstein

The Quick Take

- A concentrated volley of crises has made the world an uncertain place; but opportunities exist for those who seek them

- No matter the quality of an asset, an investment is only good if the price paid is right

- Richemont’s rich heritage and enviable portfolio of luxury brands place it in a class of its own. We strongly believe that buying Richemont at its current price is an attractive proposition and will benefit our clients’ portfolios in the future

IT HAS BEEN a dramatic and disconcerting start to the year. We appear to lurch from one crisis to the next. The world had barely recovered from the Global Financial Crisis before we were hit by the Covid-19 pandemic and, just as life was starting to return to normal, we are now faced with the material implications caused by the Russian invasion of Ukraine.

This has coincided with a time of high inflation and rising interest rates (first time since 2018) as central banks start to unwind monetary support. In times of crisis and ensuing economic uncertainty, it is tempting to give into one’s emotions by fleeing to cash to preserve capital as the price of risk assets fall. However, we believe that to do so would be a mistake. Investing is a constant exercise in conquering one’s emotions and remaining focused on the long-term assessment of risk and value. It requires looking through the noise caused by short-term volatility. History has shown that those investors who are able to do just that, achieve outsized returns.

The cornerstone of Coronation’s investment philosophy is our long-time horizon. Every crisis we have lived through has presented a great opportunity for investors who are prepared to take a long-term view. We believe that the current turmoil is providing us with an opportunity to buy many high quality stocks at very attractive prices. Through our detailed work, we are confident that these stocks offer investors attractive risk-adjusted returns even if the economic environment deteriorates further. One such company is Compagnie Financière Richemont SA (Richemont).

A HIGH-QUALITY BUSINESS AT AN ATTRACTIVE RATING

‘As long as people want to say I love you, or I’m sorry, or I want to go to bed with you, then we have a business.’ - Johann Rupert; Richemont Chairman

Richemont is a high quality, globally diversified hard luxury business that owns some of the world’s most desirable and enduring heritage brands. These brands have legacies that span centuries and cannot be easily replicated, which raises the barriers to entry for competitors and provides a significant level of protection from technological disruption. The aspirational nature of its enviable brand portfolio affords Richemont significant pricing power and allows it to enjoy healthy margins over time. Richemont’s earnings are extremely high quality, denominated mainly in developed market currencies (largely euros and US dollars) and is supported by cash (10-year free cash flow conversion of approximately 90%). It boasts a fortress balance sheet (approximately 8% of market capitalisation comprises net cash) and a stable ownership structure that ensures that the business is managed for the long term.

UNRIVALED HERITAGE

The global jewellery market is highly fragmented, with the market share of branded jewellery estimated to be around 25%. Branded jewellery is expected to continue to gain share as considerations such as authenticity, sustainability, store of value and display of status become increasingly important for consumers.

Richemont is extremely well-positioned to benefit from these structural tailwinds by being the largest player and owning the best branded jewellery portfolio, which includes key brands such as Cartier and Van Cleef & Arpels. These brands have unrivaled heritage and are highly desired by consumers, boasting the top three most sold jewellery lines in the world, namely Love and Trinity by Cartier and Alhambra by Van Cleef & Arpels. This lays the foundation for multi-year earnings growth.

Richemont has a healthy exposure to emerging markets (approximately 58% of group revenue) with aspirational consumers that have a high affinity for luxury goods. It offers investors good exposure to the Chinese consumer with approximately 40% of sales generated from Chinese consumers, either in Mainland China or from Chinese tourists travelling abroad. Sales to Chinese consumers are expected to grow given the region’s cultural affinity for branded luxury products, and as wealth levels continue to improve as the Chinese economy transitions from being infrastructure-led to one driven by services and consumption.

BRAND EQUITY IS SERIOUS BUSINESS

The luxury watch market is very consolidated (the top three players have a revenue market share of approximately 70%), a lot more competitive and does not have the same structural tailwinds of the global jewellery market. It has proven to be more cyclical over time. The luxury watch market experienced a ‘super cycle’ between 2004 and 2014 driven by Chinese corporate gifting which benefited all luxury goods players, including Richemont, with nearly five out of every 10 luxury watches sold to Chinese consumers. This artificial demand inflated luxury watch sales by roughly 20%. When Xi Jinping became president in late 2013, he implemented a clampdown on corruption. This saw a sharp fall-off in the demand for gifting beneficiaries such as watches and expensive spirits like cognac.

The result was a painful reset for the earnings of Richemont’s Specialist Watchmakers division. Richemont has been proactive by buying back excess stock from the wholesale channel to prevent discounting, thereby protecting brand equity. Supply chain disruptions at competitors, coupled with strong consumer demand and tight cost control, has resulted in recent reported earnings recovering to above pre-pandemic levels and operating margins approaching previous peaks.

Offsetting the positives of the investment case is the uncertainty around the turnaround of Richemont’s fashion and accessories business as well as its omni-channel strategy, which comprises its investment in Yoox Net-A-Porter (YNAP) and the partnerships with Alibaba and Farfetch. Both have been loss-making and remain a drag on group earnings. Richemont has recognised the importance of online retail well ahead of its peers and discussions with Farfetch are well-advanced to create a neutral online platform for luxury groups to expand their reach beyond that of physical stores. If concluded successfully, this will eliminate losses.

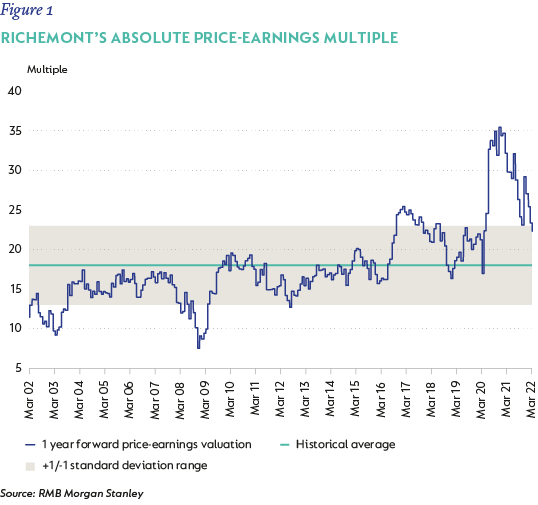

The positive attributes of the Richemont investment case are well-known and the market rewarded the company, and other listed luxury peers such as LVMH (Moët Hennessy Louis Vuitton SE), Kering and Hermès, by ascribing a high price-earnings multiple in valuing it. Richemont was a company we always wanted to own on behalf of our clients, but at the right price. After all, the best company can be a poor investment if one overpays. While the strong earnings prospects of Richemont remain unchanged given the structural tailwinds benefiting the company, it has de-rated significantly in recent years. This is on the back of several concerns, including the adverse impact of the ongoing hard lockdown in China, current geopolitical tensions and the impact on consumers’ propensity to spend on luxury goods (i.e. loss of the ‘feel-good’ factor), and rising interest rates - given the high price-earnings multiples of luxury goods companies. This de-rating is shown in Figure 1.

LOOKING AHEAD

Richemont now trades on a one-year price-earnings multiple, stripping out the net cash and excluding YNAP losses, of just under 17 times. This is extremely attractive for a global business of high quality and where we expect earnings to grow strongly for many years.

Markets remain volatile and unusual events will unfold time and time again, often in an unpredictable fashion. It is human nature to be swept up in the news flow and make knee-jerk decisions based on emotion. At Coronation, our key strength is to understand and unpack events unfolding, focus on risk and valuations when assessed over the long-term, and aim to make rational decisions that will benefit our clients. Buying Richemont today when sentiment is heavily against it, is one of those decisions.

Disclaimer

SA retail readers

SA institutional readers

Global (ex-US) readers

US readers

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter