South Africa - Personal

South Africa - Personal

Investment views

Separating the wheat from the chaff

The case for (only the best) long duration technology businesses.

The Quick Take

- During the pandemic, when attractive returns were scarce elsewhere, many investors allocated capital to riskier assets.

- Lossmaking long duration technology businesses benefited from this trend.

- However, recently rising interest rates have caused these stocks to fall out of favour.

- The sell-off has been indiscriminate, presenting us with attractive stock picking opportunities.

“We always overestimate the change that will occur in the next two years and underestimate the change that will occur in the next ten.” – Bill Gates

As the world shut down in March 2020, it resulted in an unprecedented level of forced consumer experiments being undertaken out of necessity, which boosted the fortunes of some businesses and destroyed others. Long duration technology businesses were among those that benefited by capitalising on these forced experiments.

The conundrum now is discerning between those experiments that have become habits and those that were just stop gap measures. This is an important distinction in trying to understand which businesses benefited cyclically and which benefited structurally.

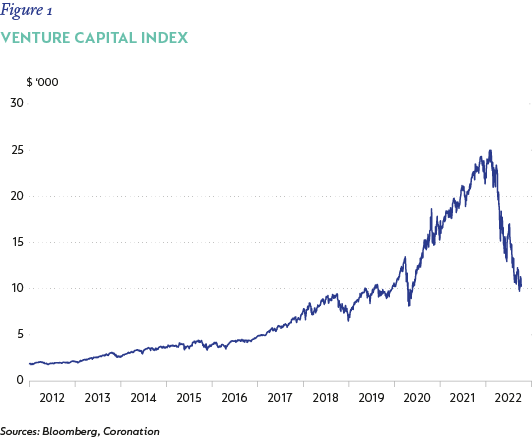

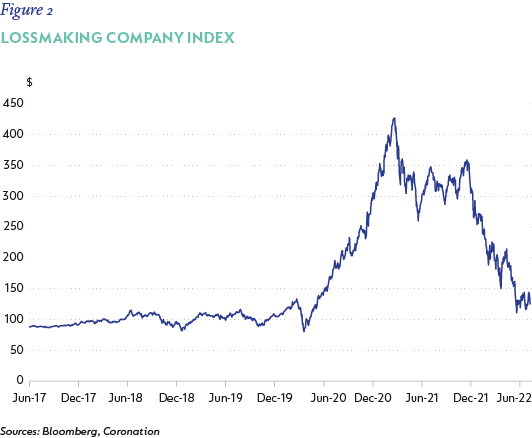

Both public and private markets have been fairly indiscriminate in concluding that many of these forced experiments would not stick and that the tailwind they provided to long duration growth businesses is not sustainable or enduring. The venture capital and lossmaking company indices (figures 1 and 2) are basically back to levels last seen in March 2020.

Whilst there are most definitely companies which got a cyclical boost as opposed to a structural one, we do not believe this is true for all businesses, and thus this synchronised selling is presenting us with incredibly attractive stock picking opportunities. The role of an active investor is to seek out these opportunities, and this is something we are incredibly excited about.

HOW WE GOT HERE

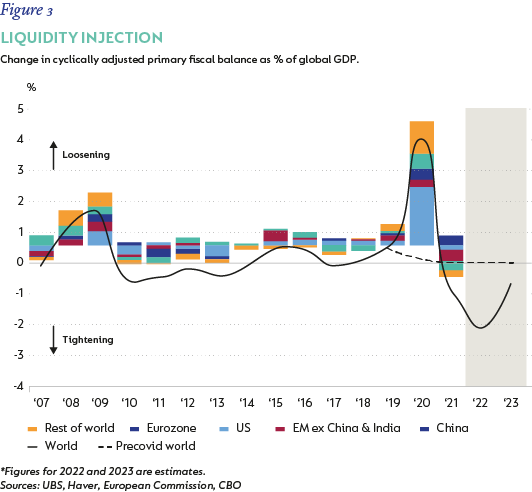

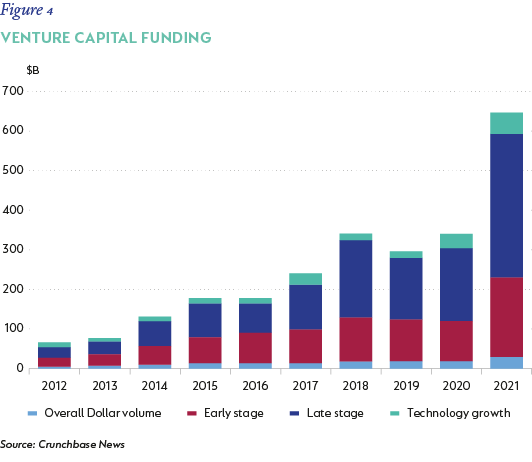

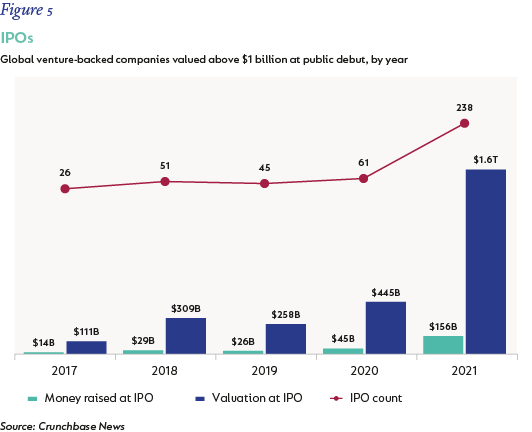

The liquidity injected into the system (Figure 3) in the depths of the pandemic allowed many of these forced experiments to be funded at levels not seen before. Long duration technology companies were either created or their development materially accelerated by this bountiful liquidity. Venture capital funding (Figure 4) reached levels in 2021 that dwarfed all previous periods, further supported by a very accommodative IPO environment (Figure 5), creating a funding cycle that arguably drove reckless financial behaviour due to the cost of capital being close to zero.

In an environment of zero or negative interest rates a common phrase was thrown around – TINA (there is no alternative), which most likely drove increased risk taking. With zero or negative interest rates many investors were forced to move up the risk curve to generate acceptable absolute returns, which created a material tailwind for “riskier” assets – lossmaking long duration businesses falling into this category.

This laissez faire environment has clearly changed, as interest rates have risen across the world and the sentiment towards lossmaking companies has become extremely negative after a period of extreme euphoria. We have gone from a period where companies with long duration growth stories were idolised to one where near-term profits and cash flow are what matters. As is often the case in financial markets, the pendulum has swung (from bulls to bears), but in an indiscriminate way that provides the stock picker with an opportunity.

Furthermore, while there are some similarities with the dotcom crash in 2000, there are also material differences. Most notably, the proliferation of technology today is at exponentially higher levels than in 2000. In 2000, only 7% of the world was using the internet. Today, this figure stands at 50%. The utility provided by many internet businesses is also significantly higher than in 2000. In 2000, the viability of many internet-based businesses was questionable, whereas today, almost every business is becoming technology enabled in some shape or form. Just consider for a moment what would have transpired if Covid-19 lockdowns were enforced in 2000. The ability of the world to continue to operate would have been materially impaired compared to what was experienced in 2020 and 2021. Whilst lockdowns were undoubtedly difficult for many people, it could have been much worse without the aid of technology and internet-enabled businesses. In the height of the euphoria, the valuations of many of these businesses resembled those in the 2000s but the subsequent correction has been indiscriminate, providing us with some very attractive investment opportunities.

HOW WE FIND OPPORTUNITIES

When trying to understand if a long duration growth business is structurally stronger today than before the Covid-19 pandemic, it is important to identify the problem the business is trying to solve. We ask ourselves if this problem has sustainable consumer demand and if it can be solved in an economically profitable way. If the answers to both questions are yes, we set out to determine if we are buying this business at a reasonable or cheap price relative to its intrinsic value.

In our view, many market participants don’t effectively differentiate between businesses, and they are selling long duration growth businesses in an indiscriminate and synchronised manner. This generally provides for an opportunity to acquire assets at cheap prices. However, this is often easier said than done, as in times of market stress, fear becomes the overarching emotion. Declining stock prices perpetuate this negative cycle, thereby shifting the focus away from underlying company fundamentals at the exact wrong time.

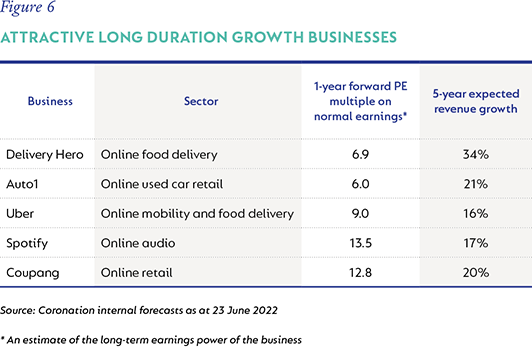

In order to avoid this trap, the focus has to remain on doing diligent and detailed work on the underlying business. This is our core focus at Coronation, and our research leads us to believe there are incredibly attractive long duration growth businesses trading at prices materially below their intrinsic value when considering the “normal” earnings power of these businesses (Figure 6).

The key focus is getting these normal earnings directionally correct and trying to invest in businesses that have a narrower range of future outcomes as the future is naturally hard to predict. Again, an important consideration in this process is understanding the problem the business is solving and if they are solving this problem better and more efficiently than their competitors.

Another factor to consider is if the growth that the above businesses offer is driven by structural growth drivers, making them less reliant on a buoyant macro environment. Counter-intuitively, the tougher funding environment can be supportive of overall business economics as competition becomes more rational. Furthermore, companies that are well capitalised are further advantaged as competitors face a world with less free flowing liquidity.

VALUATIONS ARE OUR GUIDING LIGHT

In the current environment, more weight is placed on the most recent information and any uncertainty is shunned, with many market participants waiting for more predictability and less volatility. The problem with this approach is it is often not obvious when the tide will turn, and the tide often turns at unexpected times and for different reasons than most people expect. Therefore, our guiding light remains being valuation focused and taking a longer-term view when assessing the prospects of a business. Whilst this might seem obvious, in stressed market environments the time horizon of many market participants dramatically shortens, and the potential of businesses with longer-dated payoff profiles is overlooked, which, in our view, provides patient long-term investors with exceptional opportunities.

While market corrections are often painful, the flip side is that it may allow for outsized alpha opportunities to be realized. It remains absolutely critical not to become emotional, as hard as this may be, and focus on what ultimately matters, which is buying businesses at prices below their intrinsic value. +

Disclaimer

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter