South Africa - Personal

South Africa - Personal

Stewardship & ESG

ESG: No easy solutions

But open minds and ability to shift positions are key

- Asset owners are placing increased pressure on how ESG factors are considered in portfolios

- ESG analysis cannot be reduced to numeric factors or single-score rankings

- There are negative multipliers involved in a naive approach to ESG integration

- ESG investing requires deep analysis and consideration of consequences across the board

COVID-19 HAS UNDOUBTEDLY raised the profile and awareness of the importance of environmental, social and governance (ESG) factors in investing. The impact of a global pandemic on humanity has emphasised global challenges, such as pollution and climate change, and how they need to be dealt with by a global community. The impact of severe lockdowns and the divergent performance of companies and countries have also exacerbated inequality, underscoring many of the social challenges that the world is facing.

While only being part of the solution, it is expected that listed companies play their role in addressing these challenges. An assessment of how companies are applying ESG standards and changing their business models to deal with these challenges is an integral part of our analysis, understanding and valuation of a company. We are also seeing increased interest from the ultimate asset owners – the pension funds and unit trust investors – as to how their portfolios are being managed in line with ESG standards.

However, given how nascent the industry focus on ESG is, it remains fraught with risks, in particular, attempts to oversimplify what is a multi-faceted challenge and one that does not lend itself to quick fixes and short-term solutions.

The scale and scope of ESG analysis is sometimes so large that it is difficult to capture all the elements succinctly. It is important to understand the linkages between elements of ESG and that what might be positive for one element (e.g. reducing environmental impacts) might be negative for another element (e.g. the regional social impact of shutting down environmentally sensitive operations). Even within one element, you can end up with conflicts – for example, take the push by the UK and the EU to promote diesel vehicles because of their lower carbon dioxide emissions. In the UK, due to government incentives, the diesel market share went from 7.4% in 1994 to 39% in 2016. The flaw here is that by focusing primarily on carbon dioxide, they ignored the negative effect of diesel vehicles’ particulate and nitrous oxide emissions, which result in more immediate health impacts. The US, which took a more holistic approach to assessing tailpipe emissions, did not adopt diesel incentives due to the negative externalities*.

KEEPING SCORE CANNOT BE REDUCTIVE

The above example shows why it is so dangerous to attempt to ‘score’ companies or even portfolios with a simple metric. A single ESG score inevitably loses so much relevant information that it is at best worthless, or worse, results in negative outcomes. Members of the investment industry are typically numerate people, and we all have the desire to reduce complex problems to numbers, solvable in spreadsheets and quickly comparable in tables.

The reality is that ESG is not simply a numerical problem, but one that requires significant research, understanding and debate. The rise in passive funds has, unfortunately, placed further emphasis on the simple numerical solution, as passive managers by design do not have the backing of research teams that understand the nuances of every company that they own. It is preferable in their world to download a single-point score and rank the companies, as they are unable to differentiate on any other basis.

But how do you compare different ESG risks on a simple scorecard? Is a company that is reducing its emissions drastically, yet incurring a high number of workplace injuries and fatalities, better than a company that has a high regard for workplace safety but has been unable to reduce its emissions? How do you score lives versus emissions? Similarly, some of the most advanced technology companies in the world today, while delivering huge value and life-changing solutions, often have very poor human capital ratings (consider the so-called ‘Gig Economy’ workers) and typically have founders that are entrenched through high-voting share schemes. Given their high ranking in ESG tables and their prevalence in ESG funds, these are clearly issues that do not score badly on current ESG assessments, but is this correct?

THE NATURE OF POWER

There is no greater example of unintended consequences, in our opinion, than the current global stance on divesting from fossil fuel companies. While there are myriad issues facing the world under the banner of ESG, the easy win for investors to be seen to be doing something has been their stance on thermal coal companies. The policy of divestment has been used as a blunt tool to force investment funds out of companies that have operations providing thermal coal to the world’s power plants.

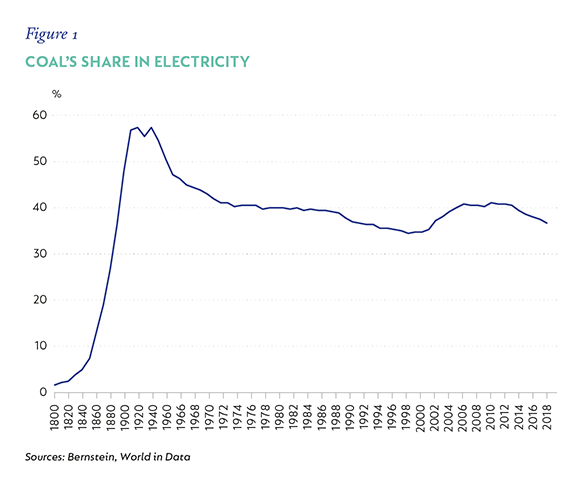

For perspective, it is important to understand that coal has been a prevalent fuel for the past century and a half, and was undoubtedly the driver that elevated the human race from an agrarian society to where we are today; principally, through the provision of electrical power.

While coal peaked in 1920 on the back of industrialisation, Figure 1 shows that, following a steady decline, coal’s share of power generation began to increase in 2000 as nuclear power fell out of favour (nuclear is greenhouse gas free but has other issues, such as safe waste disposal). This saw millions of Asians lifted out of poverty, as Asia (mainly China) industrialised. Consider that the World Bank states that China has lifted 800 million people out of extreme poverty since 1970 – truly a staggering achievement. Coal usage peaked in 2013 and has been on a steady decline since then.

THE SHADOW IMPACT

What this reality means is that there are still significant coal-fired generation facilities in existence and that there are still coal mines operating to supply their fuel source. Selling a coal mine from one’s portfolio doesn’t stop it from existing. All that this achieves is an equivalent to the tragedy of the commons, where what might be good for the individual is not good for the community. This divestment stance has seen many listed companies attempt to exit their coal mine holdings as fast as possible. The net result is that instead of sitting observable in a listed entity that is governed by global governance and environmental standards, they are leaking into separate listings, private investors and State-owned entities – none of which are better than the existing situation, and in many cases, are much worse.

Take the new listing of Thungela, where Anglo American, a large and well-resourced global miner, under pressure from investors, spun off its South African (SA) thermal coal assets into a separate vehicle. While part of a major miner with many revenue streams, these assets could have been run down in a responsible manner, under the watchful eye of society.

As a large mining group, there would have been the potential for employees to be moved to different operations as the mines ran down. The diversity of minerals would ensure that the company’s success or failure would not be linked to the performance of just one commodity. One cannot blame Anglo American’s management for doing this, as they were just responding to the incentive system that investors were imposing (i.e. sell your coal assets or else we won’t invest in you).

In 2019, Coronation specifically wrote letters to the boards of BHP Billiton and Anglo American asking them not to unbundle or sell their coal assets, but rather to hold them and run them down in a socially responsible manner. Unfortunately, we have lost this battle. Today, of all the thermal coal being mined in SA, only 41% is being done by publicly listed entities. When companies are unlisted, it becomes far more difficult to engage with these businesses and it is much more difficult to track key metrics such as:

- their emissions intensity;

- their rehabilitation funds – are they being provided, or are existing funds being stripped?;

- capital allocation into new mines or life extensions;

- mineworker safety; and

- investment in surrounding communities.

In analysing the voting on the unbundling of Thungela, it is apparent that the only major fund manager to vote against the unbundling was Coronation. Now listed on its own, Thungela is completely exposed to the risks associated with the movement of a single commodity price – that of thermal coal. Given the exact same pressures that Anglo American was under, a 100% thermal coal operation is unlikely to find a home in many portfolios, which means that capital markets are, for all intents and purposes, closed.

Banks are under pressure not to lend to coal mines, which means that Thungela will struggle to fund itself through a cyclical downturn, increasing its solvency risk. Reinsurers are under pressure not to underwrite coal assets, which means that they are unlikely to be able to insure themselves against catastrophic risks, exposing workers and nearby communities to the risk that they would not receive any compensation should one of these eventuate.

The CEO, who has now been put in charge of this new listed company and has a fiduciary responsibility to his employees and shareholders, has come out in support of his business and was quoted as follows, “Anglo was not going to invest in the future of these mines necessarily … We are now independent, where it makes sense we will absolutely invest in these mines”. So, in fact, the policy of divestment is now directly responsible for reinvestment in coal mines, which is the exact opposite of the intended end goal.

The same stance held towards coal companies is increasingly being applied to oil companies. The net result is that, because the continued demand and requirement for oil are likely to extend for many years as we transition responsibly to more sustainable power sources, the oil we need is increasingly going to be supplied by privately held companies and nation states. The downside here is that many of these entities do not comply with the most basic of environmental or governance standards.

SUBSTANCE OVER FORM

The above is an example of just some of the nuances of a particular industry dealing with a specific subset of the ESG continuum. A portfolio of shares operating across multiple industries will introduce tens and hundreds of further ESG-related issues, none of which can be reduced to simple numbers. They all require the application of thought and careful consideration with regard to what the intended outcomes are and the consequences of those decisions on all stakeholders.

Undoubtedly, mistakes will be made, but these need to be recognised and positions changed as evidence comes to the fore, showing that what was previously seen as the appropriate stance no longer applies. One needs to be open to new ideas and be prepared to stand for what is right rather than expedient. Already the industry abounds with claims of ‘greenwashing’, and it is incumbent on us as long-term managers to ensure that we can show a track record of having made meaningful change for the benefit of all, rather than just sweeping difficult problems out the door. +

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter